A Guide to Asia Pacific’s Data Centre Industry for Investors and Enterprises

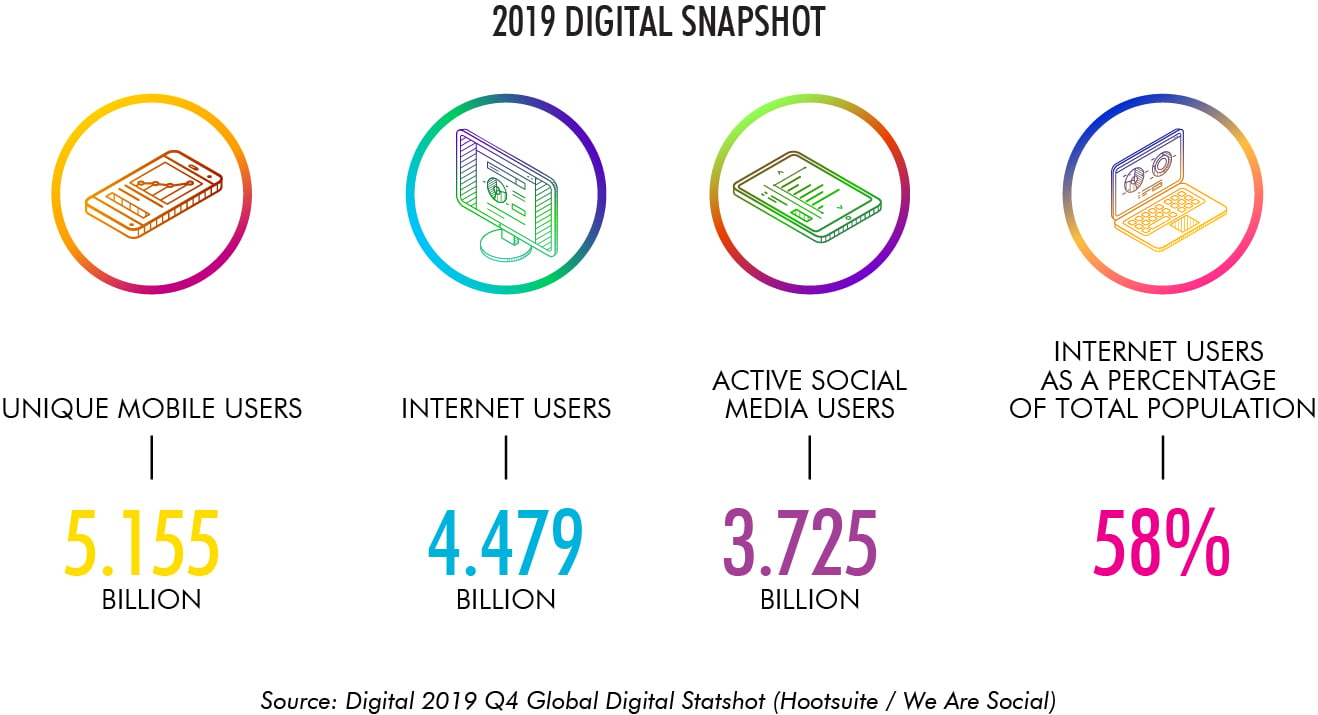

Our world is consuming data at an exponential rate. In 2019, there were over 4.4 billion active internet users, representing a 10% increase from the previous year (Hootsuite/We Are Social Global Digital Report 2019).

07 Apr 2020

Our world is consuming data at an exponential rate. In 2019, there were over 4.4 billion active internet users, representing a 10% increase from the previous year (Hootsuite/We Are Social Global Digital Report 2019). This consumption is fuelled by the rapid growth of the Internet of Things, 5G, and the early stages of Industry 4.0. As machine-to-machine communication and learning accelerates, this will only serve to push data usage to new heights.

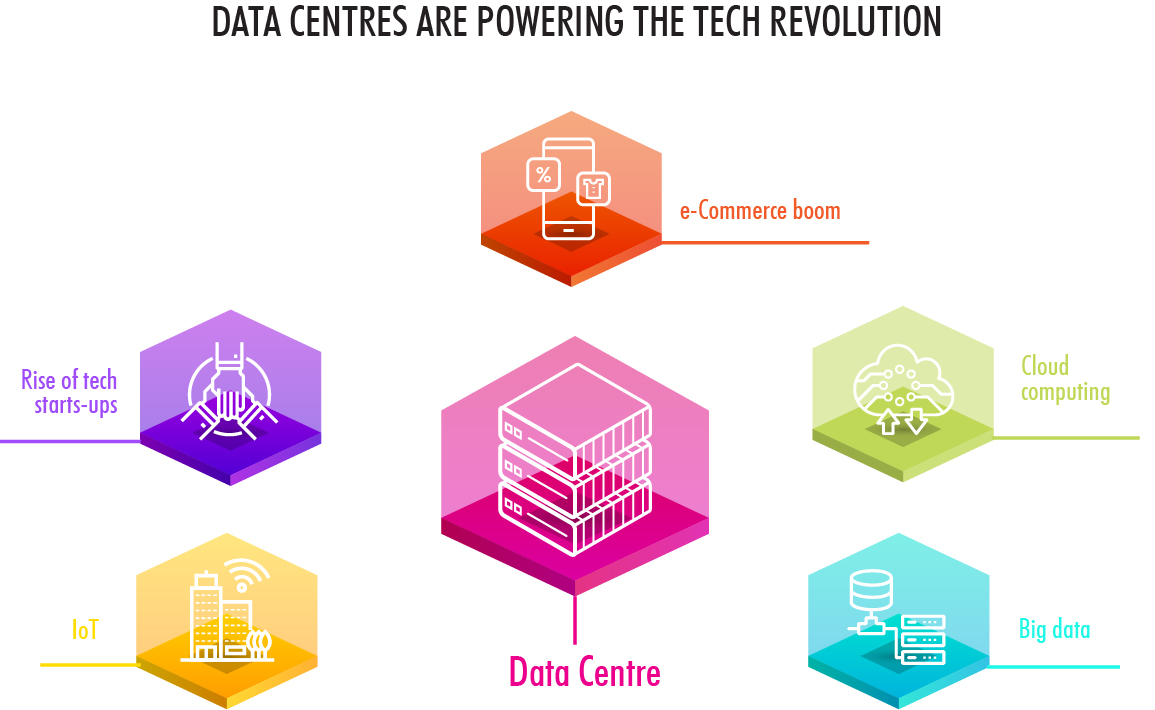

Data centres form the backbone of our technology-driven societies, which explains why this sector is sparking strong investor interest across the globe. With latency bandwidth restrictions and data sovereignty laws often requiring data to be processed geographically close to where it is consumed, demand for data centre facilities in urban areas is at an all-time high. This is turn has led to global pressure for supply to keep up with demand. According to CBRE, 2018 was a record year for data centre colocation uptake, with 2019 predicted to be even larger.

Asia Pacific is currently experiencing unprecedented levels of population growth, urbanisation and smartphone access – and these trends have generated a strong surge in data centre demand across the region. Internet penetration in US and Europe stands at 90%, while in Asia Pacific it’s between 50 to 60%. This represents a wealth of untapped opportunity for investors, since increasing digitisation will only fuel greater demand for data centres. As a result, the time to gain a better understanding of this dynamic sector is now – whether as an investor or as an end user.

The Investor Perspective

This fundamental reliance from both corporates and individuals, coupled with steadily increasing demand, means that many investors are increasingly looking to deploy capital into the data centre sector. However, given the complex nature of this particular market, investing in data centres presents its own unique set of challenges. Misconceptions abound; for instance, very few investors realise that a data centre is a service, not a real estate asset. Or that mechanical and electrical infrastructure represents a majority of the overall investment cost – between 65 and 75 per cent.

Since end users are generally averse to inexperienced investors, establishing credibility in the data centre sector through a solid track record is essential. This track record should not solely revolve around investment, but other areas of the asset class as well, such as operations.

Another important consideration is the scarcity of high-quality assets in the Asia Pacific market. Legacy data centres can prove to be challenging, since the buildings may not be designed to meet hyperscale cloud requirements fuelled by companies like Alibaba, Amazon Web Services (AWS) or Microsoft. As a result, the assets that do come to market are keenly contested; for instance, 20 times EBITDA+ is not uncommon on recently traded global platforms. Taking all these challenges into account, it’s safe to say that the barriers to entry can be quite high for new investors.

One final hurdle from an investment perspective is the fast-paced nature of the market, which is currently dominated by hyperscale cloud demand. Given the fact that it’s extremely difficult to predict hyperscale requirements beyond 6 to 9 months, there is a corresponding imperative for supply to be flexible and scalable. However, flexibility can prove to be a tricky proposition in Asia Pacific, where the time required to secure power from the grid can stretch up to 3 years in certain markets like Tokyo.

Challenges notwithstanding, we have seen investors in Asia Pacific benefit from being able to bridge issues associated with building or leasing capacity. For instance, more traditional real estate developer/investors who have a track record of delivering in heterogeneous markets can partner with hyperscale customers seeking large, dedicated facilities, or with specialist colocation providers who have developed modern facilities at competitive price points to allow organisations to enter into markets quickly. In this challenging landscape, investors and operators who ensure the quickest timescales can carve out a significant advantage in the data centre sector.

The Enterprise Perspective

From an enterprise perspective, figuring out the right data centre strategy for your business is critical to the success of your overall IT strategy. This of course is easier said than done. Many companies are re-assessing their IT strategies to adapt to the challenge of constantly evolving technologies – but the reality is that there is no one-size-fits-all solution.

A common issue that businesses grapple with is uncoordinated procurement due to regional growth and M&A. There may also be significant pressure from the CIO/CFO function to ensure that IT equipment is fit for purpose and being procured at best value via an auditable process. This is why it’s vital to have a good understanding of what the right data centre option for your business looks like.

Currently, the majority of enterprises still store data and run their servers on their own premises (on-prem). This requires significant capital investment – bearing in mind that the M&E replacement cycle is 10 to 15 years, while the lifespan for servers is usually 2 to 3 years. Another potential issue is the risk of redundancy, and whether businesses can invest the necessary capital expenditure to keep pace with changing technology. Enterprises should also consider the fact that it may not be commercially viable for them to build their own facility, especially when there are other options available in the market.

As a result, companies are increasingly turning to outsourcing as a more cost-effective option. There are two main outsourcing models to choose from; the first is colocation, which involves housing your IT equipment in data centre facilities managed by third party specialist operators. Colocation offers a few key benefits, such as the flexibility to increase or decrease capacity according to the company’s real estate strategy. Another advantage of outsourcing to a dedicated facility is that it guarantees that the necessary operational, technical and security standards will be met.

The second outsourcing model relies on cloud hosting services. So how do you decide which option is right for your business? While cloud computing has emerged as a major trend in the data centre industry, that doesn’t automatically make it the best solution for your company. For instance, cloud services might bring greater flexibility and cost savings, but issues of data security and sovereignty should also be factored in.

It’s essential for companies to understand the data sovereignty regulations in their particular market, since this will necessarily inform their wider data centre strategy. For instance, Indonesia’s law on data localisation, GR82, requires electronic system providers that provide public services to have data centres and disaster recovery centres based in Indonesia as part of their business continuity plan.

When it comes to data management, there is no magic bullet. This is why more enterprises are adopting hybrid IT solutions that strike a balance between cost and security. For example, a company could choose to still house highly sensitive applications on-prem or using a reliable colocation provider, while opting for a public cloud solution for the storage demands of day-to-day business. In a nutshell, embedding flexibility into your data centre strategy is essential to ensuring the scalability and cost-effectiveness of your broader IT strategy.

Flexibility is the Key

Whether you are an investor or an end user, flexibility should be at the heart of your data centre strategy. In a world shaped by constantly evolving technologies and accelerating data consumption, those who are willing to adapt and keep pace with change are the most likely to see their strategies pay off.

So what is on the horizon for the data centre industry in 2020? Across the region, we can expect to see more and more businesses opting for greater flexibility by pivoting from on-premise to colocation and cloud-based IT hosting solutions. As cloud computing continues to gain prominence, hyperscale providers will be looking to aggressively expand into Tier 1 and 2 markets to capture market share. Lastly, investor interest in this sector will only keep growing, which will lead to a very competitive environment.

As we’ve seen, the data centre sector can prove to be challenging from both an investor and an enterprise perspective. Given the high level of complexity and the fast-paced nature of the industry, it’s worth taking the time to understand the intricacies of the industry before taking the plunge. Only then can you avail of the wide range of opportunities arising in the sector, especially in the Asia Pacific region.

This article first appeared in the Q2 2020 issue of the SID Directors Bulletin published by the Singapore Institute of Directors.

Disclaimer:

The views and opinions in these articles belong to the author and do not necessarily represent the views and opinions of CBRE. Our employees are obliged not to make any defamatory clauses, infringe or authorize infringement of any legal rights. Therefore, the company will not be responsible for or be liable for any damages or other liabilities arising from such statements included in the articles.