Valued Insights: Asia Pacific Logistics

As more investors seek to access this increasingly attractive sector, our latest Valued Insights article examines the latest trends in the APAC logistics market.

20 Apr 2022

Investors flock to logistics real estate

Asia Pacific logistics real estate has performed strongly since the onset of the COVID-19 pandemic on the back of accelerating e-commerce penetration, the development of omnichannel retail and a drive towards augmenting supply chain resilience – all of which have translated to substantial leasing demand.

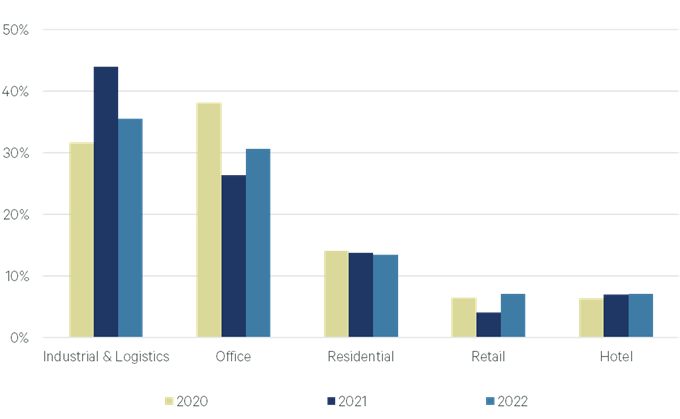

The buoyant occupier market has piqued investor interest in logistics assets, with respondents to CBRE’s 2022 Asia Pacific Investor Intentions survey naming logistics as the most popular sector for a second consecutive year.

Figure 1: Preferred sector for investment

Source: 2022 Asia Pacific Investor Intentions Survey, CBRE Research, January 2022

This interest has been converted into strong purchasing activity, with 2021 investment volume in Asia Pacific industrial and logistics real estate increasing by 58% y-o-y to US$33 billion, surpassing the previous year’s investment volume of US$21 billion by a substantial margin. The steady inflow of capital to the sector resulted in further yield compression over the course of the year.

As more investors seek to access this increasingly attractive sector, this latest article in CBRE’s Valued Insights series examines the latest trends in the Asia Pacific logistics market and considers the implications from a valuation perspective.

Broad shift to larger logistics trades

Across the region CBRE is observing a trend towards larger logistics trades, with portfolio deals trading at premiums to collective value of individual assets. In many respects, logistics is emerging as an operational trading platform versus a collection of individual properties.

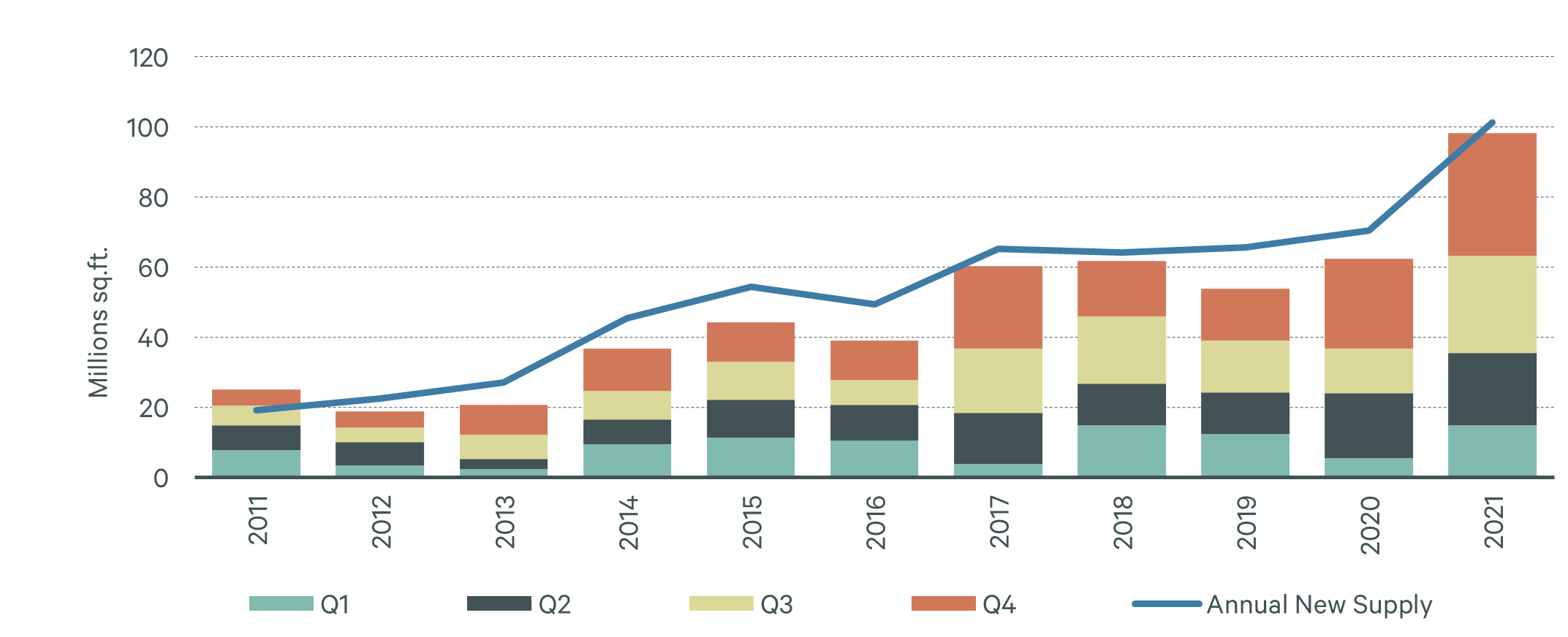

Leading Asian markets registered net absorption of 35.0 million sq. ft. in Q4 2021, the highest quarterly level on record, underpinned by robust leasing activity in Greater China, India and Japan. Full-year net absorption reached 98.3 million sq. ft., an increase of 57.3% y-o-y.

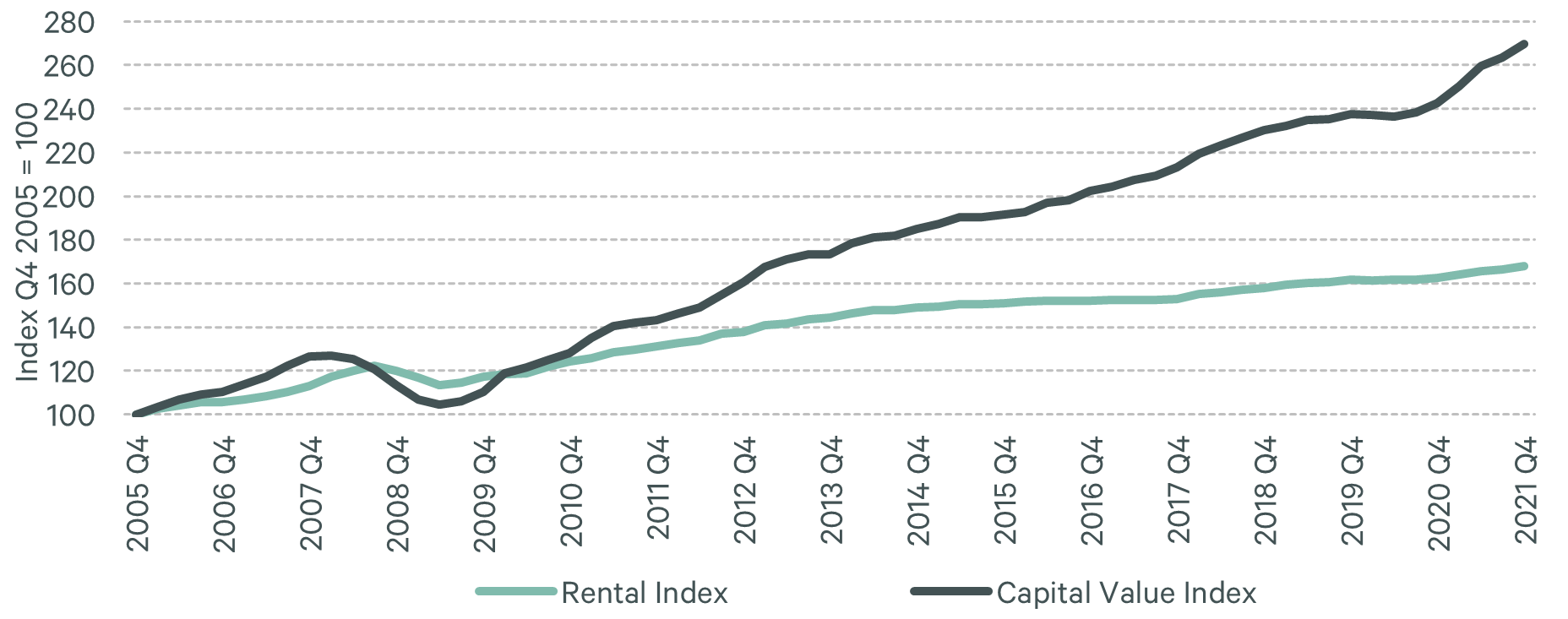

Figure 2: Asia Pacific Logistics Capital Value and Rental Index

Source: CBRE Research, March 2021

Figure 3: Asia Pacific Logistics Net Absorption and New Completions (millions sq. ft.)

Source: CBRE Research, March 2022

Greater China: Mainland sees continued strong demand for platform deals

With limited availability of stabilised or income generating assets available for sale, mainland China saw a wave of platform level investment over the course of 2021. Many institutional buyers are eyeing opportunities in development platforms, which offer higher returns than stabilised platforms. Yields for stabilised platforms are now close to those for core retail and have narrowed further with those for core office properties. Property funds have also been a major source of investment, with around half of all fund-raising concluded in 2021 raised by logistics-focused funds.

Elsewhere in Greater China, logistics deals accounted for just under 40% of investment volume in Hong Kong SAR in 2021. Most transactions have involved redevelopment and conversion projects, particularly in the data centre, self-storage, and cold storage sub-segments, with the lack of stock for sale continuing to impede any platform deals.

With so much capital deployed into the sector, yields have been driven down significantly in recent years and are now converging with those for the office and retail sectors. While the market has already been in the upcycle for close to a decade and rental growth is plateauing, some owners still anticipate short- to medium-term yield compression.

Japan: New players enter development market

Transaction volume in Japan’s logistics sector increased by 78% y-o-y to JPY 428.0 billion in Q4 2021, the largest figure for the October-December quarter since surveys began in 2005, making it the second largest sector in terms of investment behind offices. While purchasing in recent quarters has been dominated by J-REITs, new players including overseas investors have been entering the market in greater numbers.

Major developers have historically dominated logistics development in Japan, with their strategy being to construct warehouses and then transfer them to J-REITs, meaning that deals between third parties have been few and far between.

More recently, investors and developers have begun to pursue logistics development. As it remains challenging to obtain land for development, any plots or properties that are transacted between third parties typically fetch high prices.

Australia: Investors eye brownfield sites

While pandemic-related disruption continues to weigh heavily on many segments of the Australian economy, it has driven a sharp increase in e-commerce penetration, leading to strong requirements for high quality warehouse space. This has seen many investors look to reweight their portfolios to capture this demand.

The regional trend for portfolio building has also been witnessed in this market, with investors buying individual assets, bundling them up and obtaining considerable portfolio premiums.

Within Australia there is a large focus on brownfield areas and development land, with most major investors looking at purchasing older brownfield industrial stock and repositioning or redeveloping to modern logistics facilities. These urban / last mile locations are expected to capitalise on higher-than-average market rent growth.

India: The sunrise sector

Tighter regional logistics yield has prompted many investors to seek greenfield development in India during 2021, with many big names chasing opportunities in the warehouse sector, which continues to suffer from a lack of quality assets.

Among the pull factors include the pandemic-led shift from just-in-time delivery to higher levels of inventory holding, which has led to stronger take-up both now and in projections for the next 24 months. The introduction of a unified Goods and Services tax (GST) has also facilitated investment in Indian logistics property.

Additionally, with fast delivery a crucial requirement for e-commerce players’ seeking to achieve seamless omnichannel operations, there is strong demand to acquire warehouses in urban areas for last-mile delivery and also in tier II cities.

Gradual movement towards ESG adoption

As occupiers and investors look to strengthen their Environmental, Social and Governance (ESG) performance, sustainability criteria are gradually being incorporated into logistics facilities and wider operations.

Adoption generally remains confined to leading international logistics platforms and operators, with take-up limited so far in individual markets. CBRE’s 2021 Asia Pacific Logistics Occupier Survey found that focus areas include green certification, energy saving and green operations.

Figure 4: Sustainability initiatives among major logistics occupiers and investors

|

Type of Initiative |

Company |

Initiatives |

|

Green Certificates |

Prologis |

|

|

ESR |

|

|

|

Renewable Energy |

Goodman |

|

|

MapleTree Logistics |

|

|

|

Green Operations |

Cainiao |

|

|

DHL |

|

Source: Various corporate sustainability and ESG Reports, 2021

Note: This is only a small sample of companies actively pursuing ESG objectives. Other firms are adopting similar initiatives.

Given the infancy nature of ESG within the sector and lack of any evidence trends, it is currently challenging for valuers to calculate yield premiums (if any) for ESG compliant assets, with most markets possessing little or no benchmarks. In Japan, while CBRE has not yet seen any cases of rent growth or cap rate compression due to ESG, it will likely become a key area of focus for investors in future.

Elsewhere, Melbourne has seen no movement in rents or cap rates due to ESG performance. While many industrial users show little interest in ESG criteria, adoption among larger corporate occupiers is gaining meaningful traction, which will continue to exert pressure on logistics investors to ensure their properties are ESG compliant.

Other key trends include the growing adoption of smart warehouse technologies, which have played a key role in helping e-commerce platforms improve efficiency, augment order handing capacity, and resolve labour shortages. Owners and investors are advised to respond by offering lease tenures that can encourage technology adoption, facilitate the installation of sensor systems, and provide additional electricity capacity.

Conclusion

Robust investment in logistics property globally has valuers looking for ways to support underlying asset pricing. Most markets have seen yields reduce substantially over the past three to four years, some by as much as 300bps.

In many markets, valuers have seen lower total return hurdles driving pricing, with transactions being underwritten by strong rent growth, particularly in the short term. While this has firmed capitalisation rates, this is with the expectation of cash yields improving strongly in the near term.

The valuer is interpreting market transactions that indicate a structural change in the logistics sector and expectations of rent growth. In-house logistics operations are becoming more complex and driving growth of third-party logistics, necessitating the need for efficient logistics solutions.

This is increasing complexities within the supply chain, from transporting materials to factories and finished goods to retailers and distributors. Together with the advent of the omnichannel approach, this is anticipated to drive demand for fourth party logistics firms capable of handling complex supply chain operations.

CBRE expects that these new business models will support stronger profits in both 3PL and 4PL operations and underpin rent growth fundamentals, supporting structural changes to the logistics market and spurring investor demand.

Disclaimer:

The views and opinions in these articles belong to the author and do not necessarily represent the views and opinions of CBRE. Our employees are obliged not to make any defamatory clauses, infringe or authorize infringement of any legal rights. Therefore, the company will not be responsible for or be liable for any damages or other liabilities arising from such statements included in the articles.