Valued Insights: Multifamily

Rapid urbanisation, escalating housing prices and impactful regulatory changes are spurring the development of multifamily real estate in Asia Pacific.

20 Sep 2021

Rising Investor Interest in Asia Pacific Multifamily

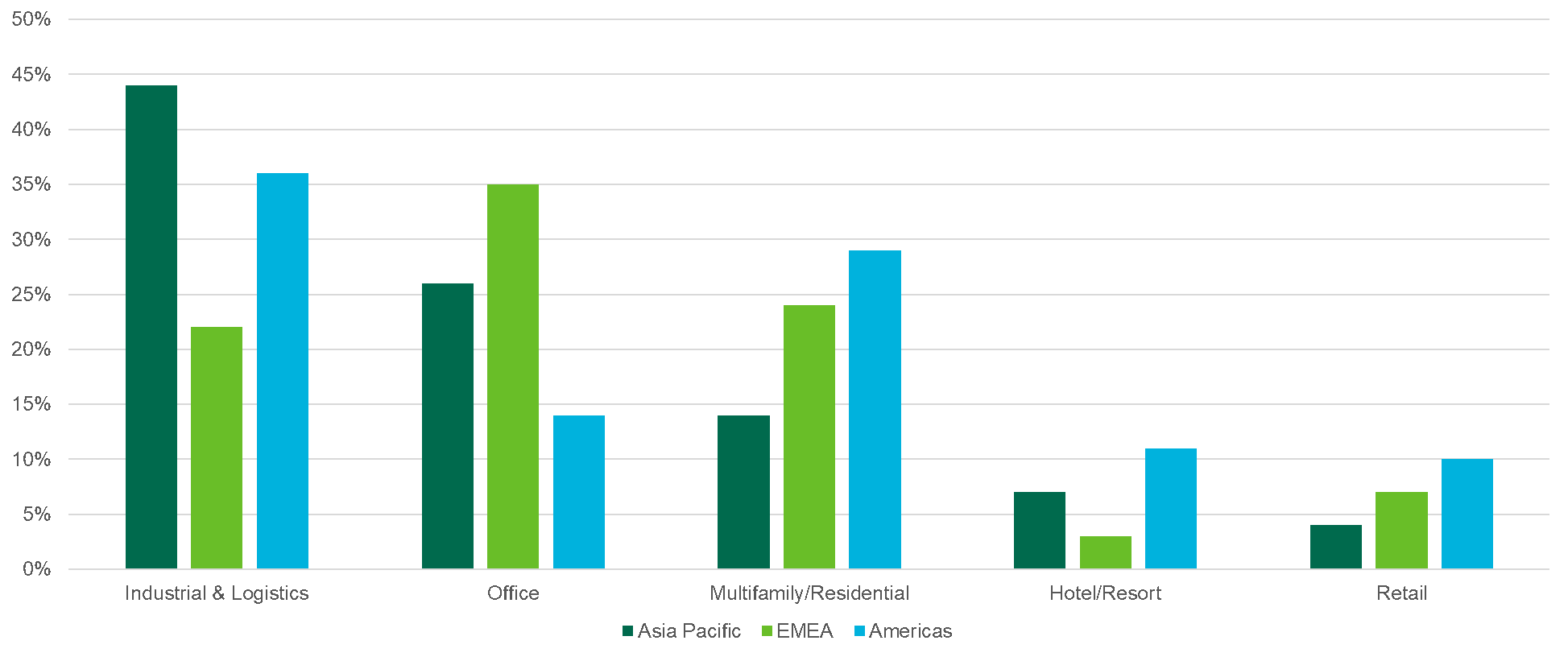

Rapid urbanisation, escalating housing prices and impactful regulatory changes are spurring the development of multifamily real estate in Asia Pacific, driving strong end-user demand and drawing an increasing volume of institutional capital to the sector.Multifamily ranked as the third most popular sector for investment in CBRE’s 2021 Asia Pacific Investor Intentions Survey, despite the economic impact of measures to contain the COVID-19 pandemic and fierce competition from other asset classes.

Figure 1: Preferred Sector for Investment in 2021

Source: Global Investor Intentions Survey, CBRE Research, February 2021

Source: Global Investor Intentions Survey, CBRE Research, February 2021

Regional investment turnover still trails far behind that in the west, however, with Japan, the region’s most developed multifamily market, registering US$ 6.8 billion worth of transactions in 2020, compared to Europe’s US$ 75 billion and the U.S.’s US$ 142 billion, according to RCA and CBRE Research data.

This latest article in CBRE’s Valued Insights series provides an overview of the Asia Pacific multifamily sector and discusses the latest developments, trends, and opportunities from the perspective of CBRE’s valuation experts.

What’s Driving Multifamily Demand?

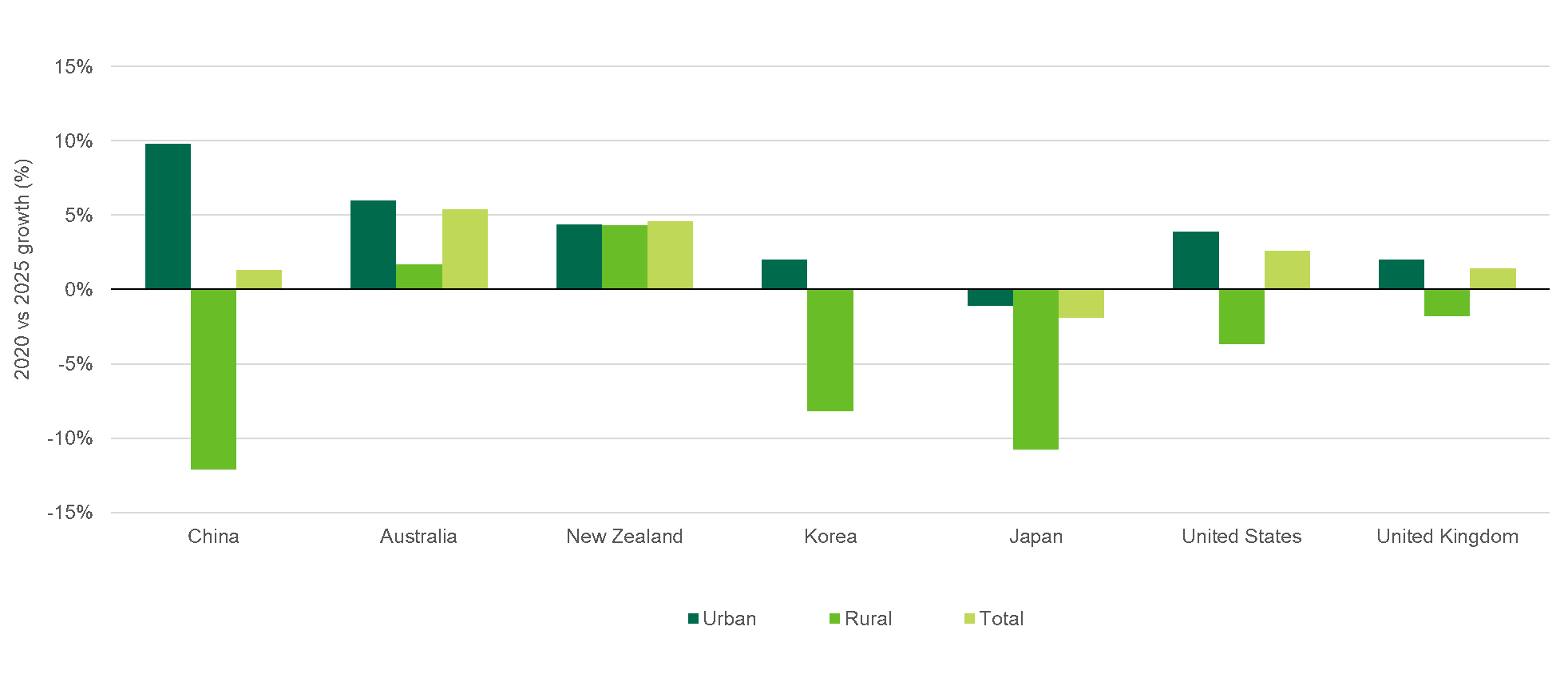

Around 2.3 billion people resided in Asia Pacific’s cities in 2019, marking the first time the region has been predominantly urban.[1] As large numbers of people relocate to cities to secure employment and improve social mobility, demand for rental housing is rising, particularly in major markets such as mainland China and Australia.Figure 2: Forecasted Urban and Rural Population Growth by Country (2020 vs 2025)

Source: Oxford Economics, June 2021

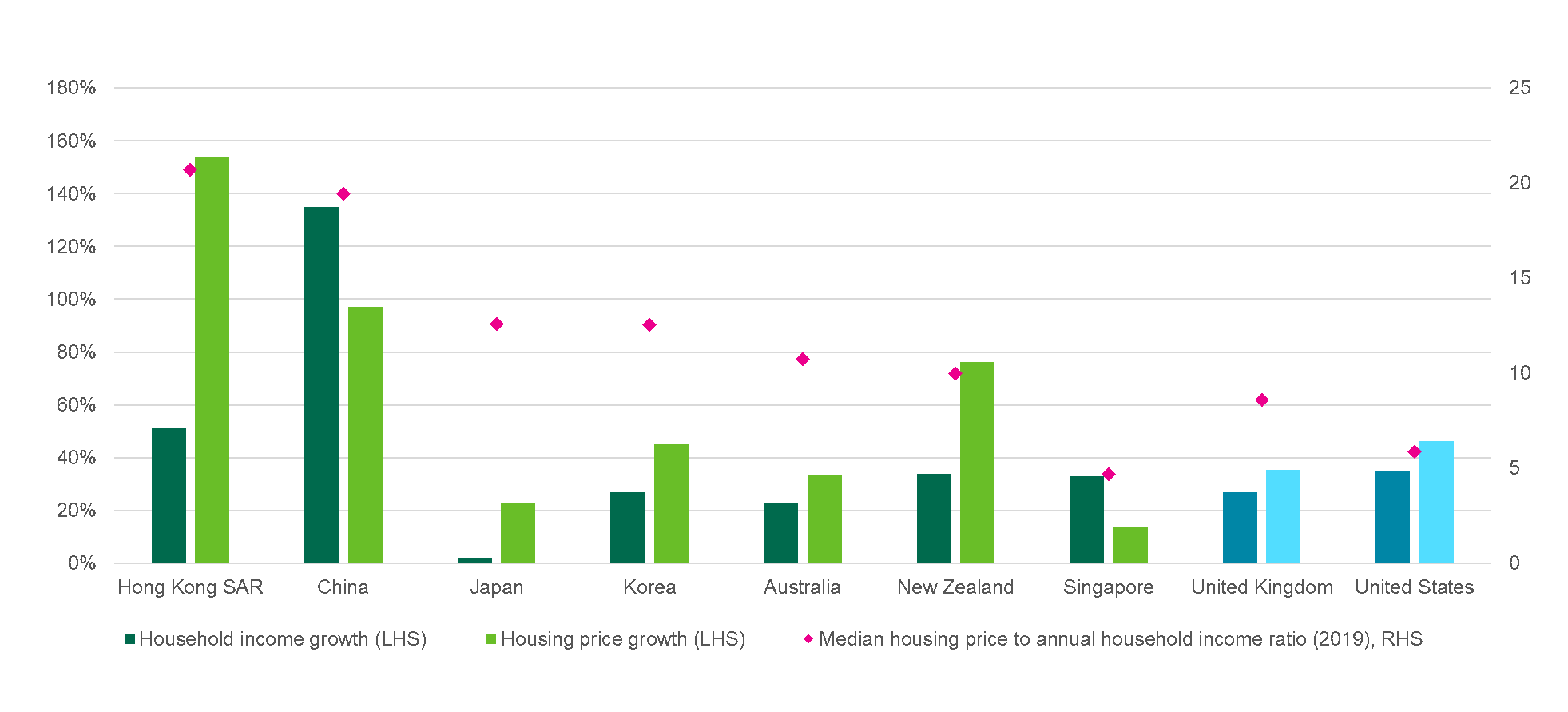

Housing affordability in Asia Pacific is declining as residential price growth outstrips rises in incomes, with the average cost of a home in a mainland China tier 1 city now equivalent to 13 years’ average salary. This has prompted authorities in several markets to introduce polices supporting build-to-rent residential development projects, spurring expansion of the sector.

Figure 3: Housing Price Growth vs Household Income Growth (2010 vs 2019) and Median Housing Price to Annual Household Income ratio (2019)

Note: The median housing price to annual household income ratio for China is the average of four tier-1 cities, Korea is Seoul, Australia is the average of Sydney and Melbourne, New Zealand is Auckland only. United Kingdom covers London only while the U.S. covers New York only.

Source: Oxford Economics, CEIC, Demographia, E-house, May 2021

Foreign Investment Boosts Japan Multifamily

Rising population densities in core areas, a growing number of smaller households and a cultural preference to rent apartments before making a once in a lifetime home purchase are driving demand for rental housing in Japan’s major cities.

The typical Japan multifamily asset is a six to 10-storey building located near a train station with two or three units of around 20 sq. m. on each floor. Selected other properties provide larger unit sizes of up to 100 sq. m. Recent years have seen younger renters request added value features such as Wi-Fi.

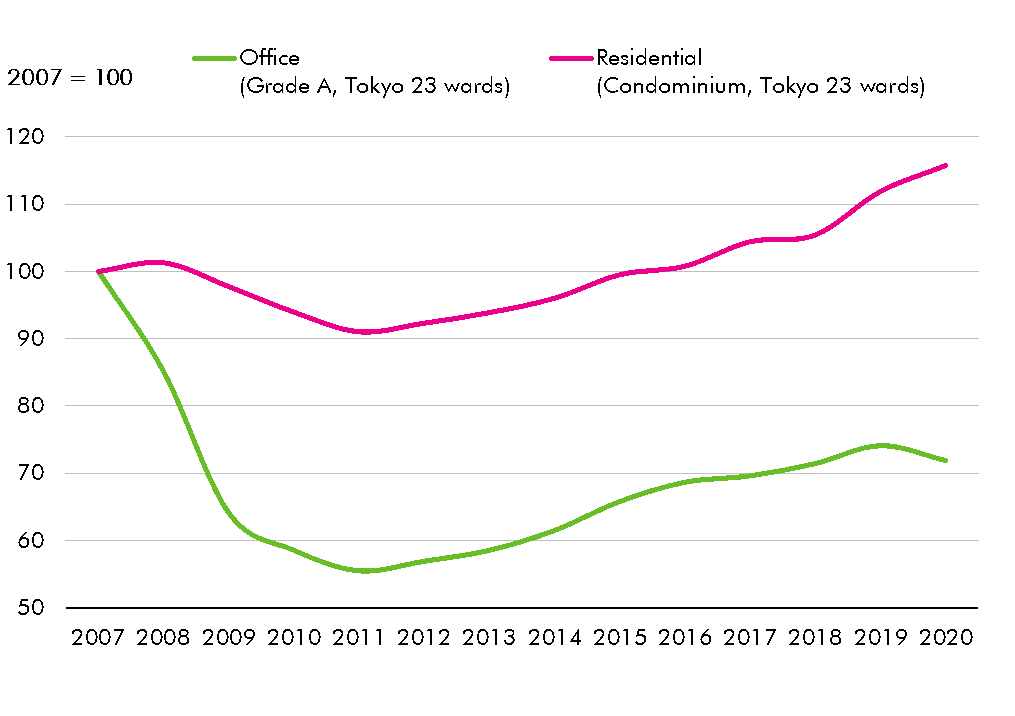

Multifamily has been among Japan’s most resilient property sectors over the past decade, with robust demand and a steady, albeit manageable, flow of new supply translating to strong rental performance. Since 2007, condominium rents in the Tokyo 23 Wards have comfortably outperformed those for Grade A offices in the same district (Figure 6).

Figure 4: Tokyo Prime rents by Sector

Source: Tokyo Kantei (NLA is less than 30㎡), CBRE Research, February 2021

Japan’s multifamily sector was traditionally confined to domestic owner-operators, who would develop buildings and then operate them. As investment capital flowed into Japan’s commercial real estate investment market, investors seeking stable income streams began to consider multifamily as a viable investible asset class. This led to investors such as J-REITs buying entire portfolios comprising 10 or more multifamily buildings while retaining the previous owner-occupiers as managers. Foreign buyers subsequently began expressing an interest in the sector, with overseas capital rising steadily in recent years, reaching US$4.9 billion, or 72% of investment volume, in 2020.

With multifamily yield having tightened in Tokyo, investors are now considering regional cities offering higher returns, such as Osaka and Fukuoka. Despite Japan’s population continuing on an overall downward trend, net population inflows in in the Tokyo 23 Wards and satellite cities adjacent to Tokyo including Kawasaki and Saitama continue to provide attractive opportunities for investors.

Growing Interest in Build-to-Rent in Australia

Multifamily as an asset class is gaining ground in Australia, predominantly in Melbourne and Sydney. The typical format is for around 400 dwellings per development, ranging from mid- to high-rise. While most properties are located in the city or city fringes areas or high-density satellite locations, future developments will be announced, and opportunities will arise in middle ring suburbs.

Growth is being driven by the weight of institutional capital seeking low risk stable returns coupled with the country’s expanding population of renters, lifestyle changes, constrained dwelling supply, a decline in housing affordability and existing mediocre quality rental accommodation.

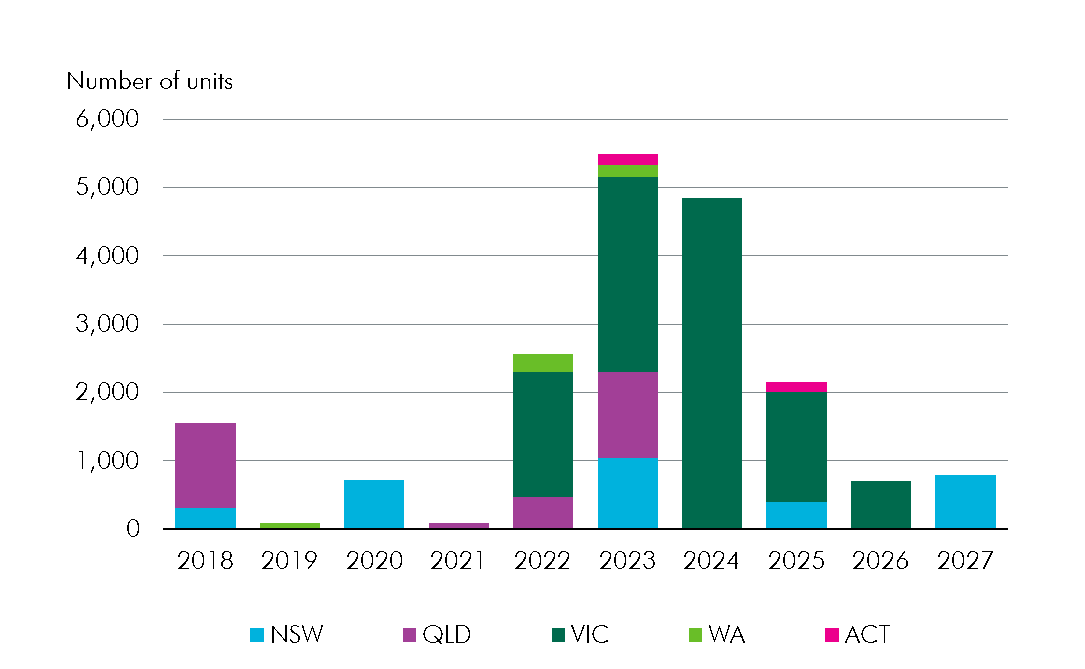

Initial interest in Melbourne and Sydney resulted in a significant pipeline in the former owing to its relatively high availability of suitable land and lower land costs compared to the latter. Victoria will account for the bulk of new build-to-rent residential supply over the next five years, with New South Wales and Queensland the other main sources of new stock.

Figure 5: New Supply of Build-to-Rent Projects by State

Source: CBRE Valuations & Research, June 2021

Although there has been positive activity in Australia’s build-to-rent sector, challenges remain around taxes on land value, Goods and Services Tax (GST), Managed Investment Trust (MIT) withholding tax and foreign ownership surcharges. These factors weaken returns and erode profit margins, resulting in some build-to-rent projects failing to hit investors’ return targets.

However, recent moves by New South Wales to reduce land tax by 50%, subject to several conditions, and proposals by Victoria for a similar initiative, will provide savings. A potential change for multifamily assets to a Commercial Residential Premises classification—similar to serviced apartments, purpose-built student housing and hotels—could allow for a more favourable and level playing field for treatment of GST for developers and Managed Investment Trust (MIT) withholding tax for foreign investors.

Foreign investors have been active in providing project financing for or taking equity stakes in multifamily developments, particularly those with international exposure and experience. CBRE expects credit to emerge as a viable investment channel for foreign investors initially, as by pursuing this route they will not be subject to the MIT.

Mainland China Offers Potential

Mainland China’s multifamily sector remains small as developers overwhelming prefer the build-to-sell model. However, its population of 1.4 billion, accelerating rate of urbanisation, and rapidly falling housing affordability have placed it on domestic and overseas multifamily investors’ radar.

Being the locations for the strongest population growth and lowest housing affordability, the four Tier 1 cities of Beijing, Shanghai, Guangzhou, and Shenzhen are the main focus for investors. Selected Tier 2 cities are also attracting interest. These include Hangzhou, which is home to a large number of technology and financial companies, and Nanjing, which has a large university population.

Renters in the 21-30 population cohort, which accounted for over 60% of rental housing demand in the country in 2019, are displaying strong demand for centralised rental apartments featuring high quality facilities, cleaning services and a safe and convenient environment. With individual landlords typically unable to provide such an offering, there is a niche for institutionally owned and managed residential accommodation.

Figure 6: Floating population and housing affordability in major cities in 2019

Source: E-house China, Demographia, CBRE Research, 2020

The major rental apartment players in mainland China are developers, operators, and hotel operators. Developers typically build rental apartments into existing projects, while operators mostly adopt an asset light approach featuring a sublease model. There is also increasing participation by hotel operators leveraging their existing hotel properties.

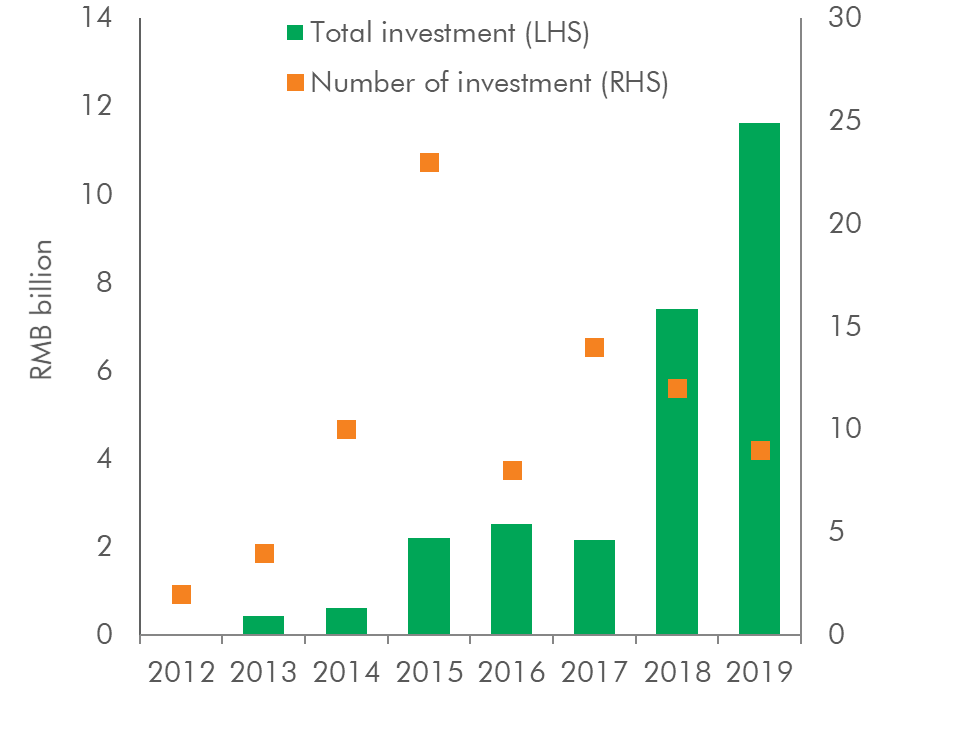

Recent years have seen rapid growth in private equity and venture capital investment into mainland China’s long-term rental apartment sector, with RMB 11.2 billion worth of deals completed in 2019, more than five times that in 2017.

Figure 7: Private Equity/Venture Capital Investment in Long-Term Rental Apartments 2012-2019

Source: Beike, Danke, Public Information, CBRE Research, June 2020

While the cost of land remains a major obstacle and can pose a challenge for developers seeking to create long-term rental apartment projects that can generate an attractive yield, authorities are now increasing land supply for subsidised rental properties and providing credit lines for construction.

In addition to development, investors can access mainland China’s long-term rental apartment sector through investing in equity platforms, while other options include converting underperforming lower star hotels into rental accommodation.

Conclusion: Can Multifamily Become a Core Asset in Australia and Mainland China?

Multifamily is a traditional asset class in the U.S. and Europe, where CBRE values millions of dollars of real estate for investors and financiers annually. In Asia Pacific, investors now clearly view multifamily and its ongoing resilience as a very attractive sector, with CBRE’s Japan team valuing a large proportion of the US$ 7 billion of investments made in this market in 2020.

Ongoing demand for core assets has developers, operators, and investors looking at alternates and new market opportunities. For these new opportunities to be fruitful, there must be occupier demand. As well as the established market of Japan, this occupier demand and growth appear to be front and centre in Australian and mainland China.

Both Australia and mainland China appeal to operators and investors in different ways. Provided the legal, operating, investment and tax structure frameworks are well considered and implemented, these markets are set to experience strong and rapid growth.

Amid falling returns for commercial real estate, growing appetite for alternative asset property classes, eagerness for diversification, and rising end-user demand, CBRE expects multifamily investment volumes to pick up further in the coming years. Investors keen to enter this sector should engage specialised and experienced valuation advisors to maximise their chances of success in this growing asset class.

[1] https://sdg.iisd.org/news/escap-un-habitat-publish-guidebook-for-future-urbanization-in-asia-pacific/

Disclaimer:

The views and opinions in these articles belong to the author and do not necessarily represent the views and opinions of CBRE. Our employees are obliged not to make any defamatory clauses, infringe or authorize infringement of any legal rights. Therefore, the company will not be responsible for or be liable for any damages or other liabilities arising from such statements included in the articles.