Singapore

CBRE's commentary for URA Q2 2023 stats

July 28, 2023

Associated Contact

Head of Marketing & Communications, Singapore

Office

• Tight market conditions continued to hold up the office market. Based on URA statistics, office rents in the Central Region increased for the seventh consecutive quarter since Q3 2021. The URA office rental index increased by 2.3% q-o-q in Q2 2023, though there was some moderation in the pace of rental growth, from the increase of 5.1% q-o-q registered in the previous quarter.

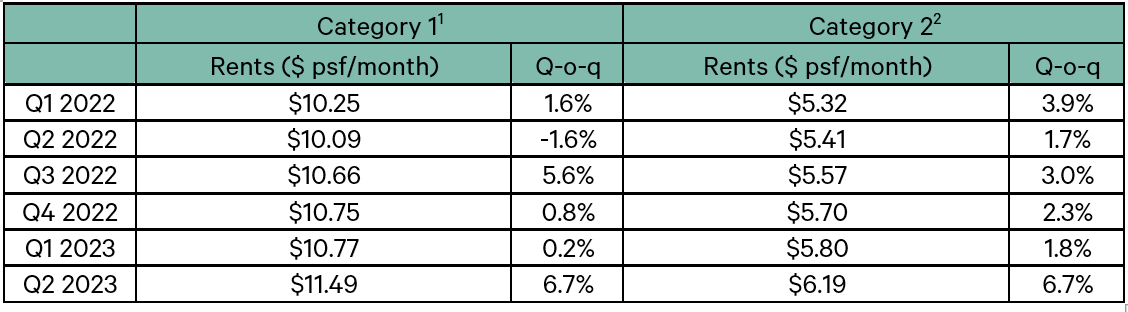

• CBRE Research notes that the pace of rental increase for prime buildings in Downtown Core and Orchard planning areas has surpassed expectations, based on median contracts signed. Median rental (by contract date) in Category 1 (a proxy for prime CBD) office space accelerated by 6.7% q-o-q in Q2 2023, from 0.2% q-o-q in Q1 2023.

• This can be attributed to the prevailing tight vacancy levels in prime office buildings, with vacancy rates for Category 1 buildings declining to 9.2% in Q2 2023 and matching vacancy levels back in Q2 2020 when the pandemic just commenced. CBRE Research also observed that selected occupiers were in favour of renewing their leases with higher rental rates rather than pursue relocation alternatives, as the current challenging market conditions were exacerbated by high fit-out and funding costs. In addition, more occupiers are now focusing on space optimisation and some are rightsizing to a more efficient footprint. These reasons may have collectively led to a higher $psf/month rent in Q2 2023.

• Although prevailing vacancies have been low, CBRE Research notes that total amount of shadow space in the office sector remains quite high among prime office buildings in Downtown Core. These shadow space may eventually materialise into higher vacancy rate in the future. Going forward global macroeconomic headwinds and corporates’ cost-cutting exercises could aggravate the situation in H2 2023.

Table 1: Median rentals based on contract date

2 Refers to the remaining office space in Singapore which are not included in “Category 1”

Source: URA

• According to data tracked by CBRE Research, Core CBD (Grade A) rents increased by 0.9% in H1 2023, largely supported by tight vacancies.

• Going forward, rents and occupancies could come under pressure amid a more cautious environment, as high interest rates and weaker economic growth persist for the rest of the year. Continued corporates’ cost cutting exercises could result in shadow space potentially increasing, which could compete with new office supply which is still largely un-committed.

• Under the confluence of rising risks and flight-to-quality trends, CBRE Research expects Core CBD (Grade A) rents to stabilise into H2 2023, while rents of older offices may see downward pressure.

Retail

• Retail indicators such as the retail sales index remained positive, a testament to consumers’ spending power and tourism recovery despite the weak global economic backdrop. As a result, URA’s Q2 2023 data showed that rents of retail space in the Central Region rose by 0.3% q-o-q, reversing five consecutive quarters of decline. Similarly, CBRE Research notes that prime retail spaces performed well in the quarter, rising by 0.8% q-o-q as demand remained strong for such locations.

• According to URA data, the islandwide private retail market saw higher leasing activity in Q2 2023, and hence positive net absorption of 25,000 sq. m. (about 269,000 sq. ft.), compared to the lower take-up of space in Q1 2023 which saw negative net absorption of 13,000 sq. m. (about 140,000 sq. ft.).

‒

• Islandwide private retail vacancy rates thus fell from 8.5% in Q1 2023 to 8.3% in Q2 2023, contributed mainly by strong take-up of space in the Fringe submarket, which continued to outperform in Q2 2023. This was accentuated by the opening of The Woodleigh Mall, following the debut of Shaw Plaza Balestier in the previous quarter. The submarket’s retail vacancy rates thus fell from 8.0% in Q1 2023 to 7.5%, the lowest since Q2 2014’s 7.4%. In H2 2023, a few significant projects in the Fringe area, such as One Holland Village, are due to be completed, which could continue to support take-up in the submarket.

• CBRE Research believes that rents have bottomed and are seeing a nascent recovery alongside an improvement in vacancy rates in Q2 2023. Anecdotally, CBRE Research notes that demand continued to be primarily driven by F&B operators, especially cafes. Fashion and beauty & health stores including Massimo Dutti, Sift & Pick and Rituals also increased their presence in the quarter.

Outlook for Retail

• Retailers remain optimistic about tourism recovery and consumer spending. However, in the near term, they may continue to face challenges such as manpower shortage, higher operating costs, and another GST hike. Nonetheless, with improved mobility, tourism recovery and a below-historical-average new retail supply in the next few years, CBRE Research expects overall retail rents to see a sustained recovery in 2023, led by prime Orchard Road and City Hall/ Marina Centre retail space.

Residential

Overall private housing prices declined in Q2 2023 for the first time in three years. URA’s All Private Residential Price Index registered a 0.2% q-o-q increase in Q2 2023, reversing from its 3.3% q-o-q growth in Q1 2023. The price decline was led by a 2.5% q-o-q price decline in non-landed RCR properties.

• Private home prices declined 0.2% q-o-q in Q2 2023, the first decline after 12 consecutive quarterly increases and reversing from 3.3% q-o-q growth in Q1 2023. With this, private home prices have risen 3.1% in H1 2023, and 27.8% since bottoming in Q1 2020 at the onset of COVID-19. Prices of non-landed properties fell 0.6% q-o-q after a 2.6% rise in Q1 2023 while prices of landed properties rose 1.1% q-o-q, a significant moderation from the 5.9% increase in Q1 2023.

• The decline in prices of non-landed properties was mainly driven by properties in the Rest of Central Region (RCR) where prices fell 2.5% in Q2 2023. This could be attributed to new projects such as Riviere, Piccadilly Grand and Amber Park clearing their last few units in the quarter, resulting in lower median prices. In addition, new RCR projects launched during the quarter such as Tembusu Grand, Reserve Residences and Blossom by the Park sold well at attractive prices, and in turn could have competed with older stock and tempered price expectations in the secondary market.

• Non-landed CCR prices also saw a 0.1% q-o-q decrease in Q2 2023 compared to a 0.8% increase in the previous quarter as some projects in the CCR such as The Atelier, which are nearing completion, continued to move units on the back of developers offering discounts and marketing campaigns. In contrast, OCR prices saw a 1.2% price increase q-o-q in Q2 2023, moderating from the 1.9% rise in Q1 2023 on low transaction volumes.

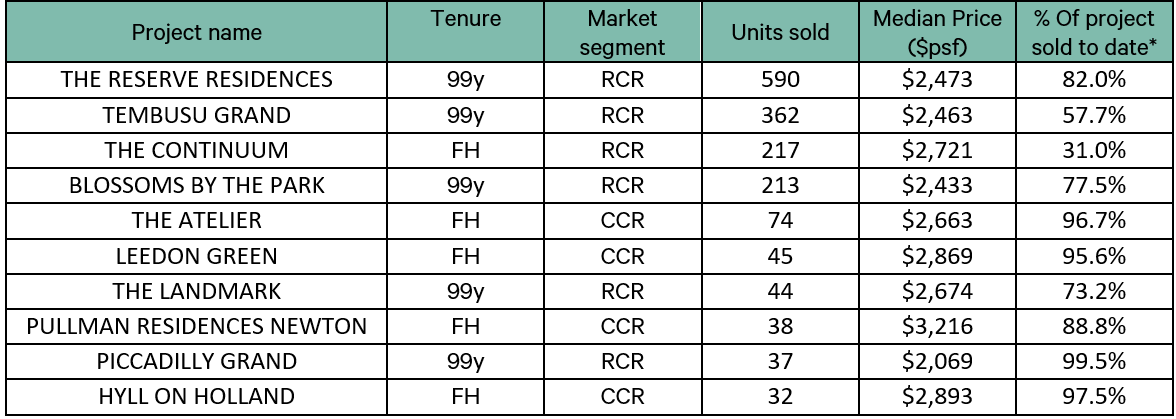

Table 2: Top 10 best-selling new developer sales projects (excluding ECs) for Q2 2023 (ranked in descending order by number of units sold in the quarter)

*Sales status based on caveats from Realis as of 28 Jul 2023.

• New home sales picked up q-o-q on the back of attractive new city fringe launches. 2,127 new homes were sold in Q2 2023, a 69.3% q-o-q increase from 1,256 units in Q1 2023. Sales were largely supported by robust take-up at new RCR launches, Blossoms by the Park (275 units), Tembusu Grand (638 units) and The Reserve Residences (732 units). Sales volumes, however, were still lower y-o-y compared to Q2 2022’s 2,397 units amid high interest rates, tighter financing conditions, and a slowing economy.

• Stable activity was observed in the resale market. 2,976 resale units were transacted in Q2 2023, a 13.5% pickup from Q1 2023’s 2,622 units. Resale transactions made up 55.2% of total transactions in Q2 2023, a lower proportion compared to 63.6% in the previous quarter due to higher new sales as homebuyers gravitated to attractive new launches in the quarter.

• Unsold inventory of uncompleted private residential units (excluding ECs) rose in Q2 2023 to 17,484 units from 16,252 units in Q1 2023. Including completed units, unsold inventory has likewise risen 8.9% from 16,464 units in Q1 2023 to 17,924 units in Q2 2023. Recent GLS tenders at Marina Gardens Lane, Tampines Avenue 11 and Jalan Tembusu have indicated signs of heightened developer caution amid elevated interest rates and economic uncertainties, with said sites fetching fewer-than-expected bids and top bid prices at the lower end of market expectations.

‒

• While unsold inventory is still significantly lower than the last peak of 37,799 units recorded in Q1 2019, the Government has ramped up GLS confirmed list supply under the H2 2023 GLS Program further to bring 2023’s full year supply to 9,250 units, the highest in a decade. Supply is now more in line with the 10-year average developer sales (2013 – 2022) of 9,706 units. Upcoming tenders of GLS sites could continue to see interest but developers are likely to remain highly cautious and selective until there is more clarity on an economic recovery and interest rate stabilisation.

• Rentals of private residential properties continued rising in Q2 2023, but momentum eased. Based on the URA Rental Index for all private residential properties, rents rose 2.8% q-o-q in Q2 2023, slowing from the 7.2% q-o-q rise recorded in Q1 2023. With completions continuing to outstrip demand, vacancy rates increased to 6.3% in Q2 2023 from 6.0% in Q1 2023. Rents are anticipated to ease further moving forward alongside abundant new supply in the coming quarters. Expatriate demand could moderate as companies restructure and cut back on hiring amid challenging economic conditions.

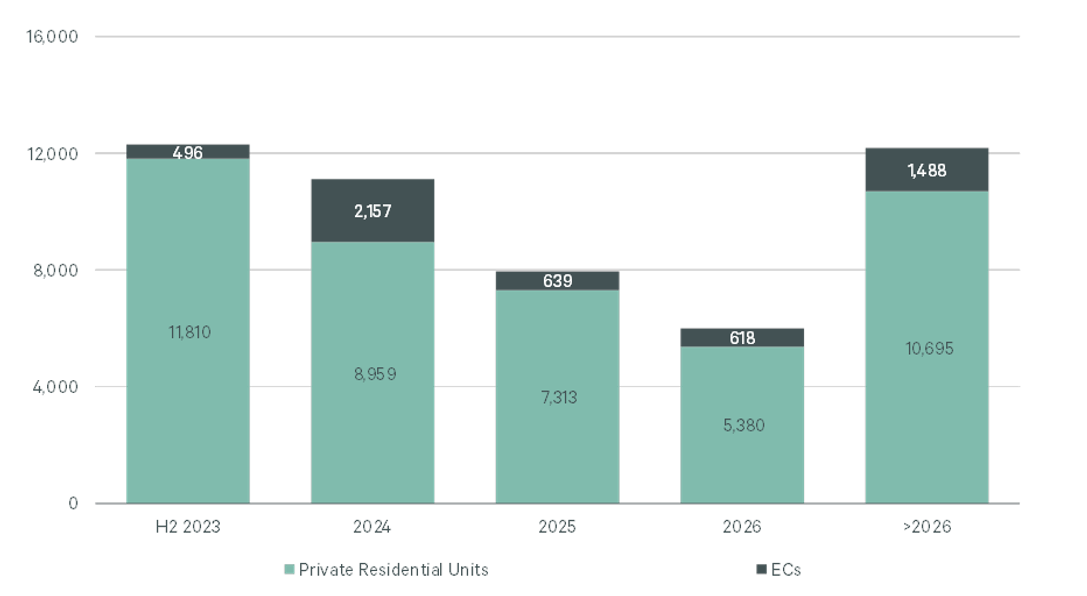

Chart 1: Projected Completions by Year*

Source: URA, CBRE Research. Note: 4,401 private residential units were completed in Q2 2023.

*For private residential units and ECs with planning approvals

Outlook for Private Residential

• H1 2023 new home sales currently stand at 3,383 units, a 19.9% y-o-y fall from 4,222 units sold in H1 2022. However, home sales could catch up with 2022’s home sales in H2 2023 due to a greater number of launches available, offering more choices for buyers. July is set to be a blockbuster month, with at least 1,108 units already sold across four new launches opening in the weekends of 8-9 and 15-16 July. It was reported that The Myst sold 27% (110 units) of its total 408 units at an average price of $2,057 psf, Lentor Hills Residences sold 50% (298 units) of its total 598 units at an average price of $2,080 psf, Pinetree Hill sold 150 units or 29% of total 520 units at an average price of $2,460psf, and Grand Dunman moved 55% (550 units) at an average price of $2,500 psf over their respective launch weekends.

• Despite higher prices, there is still liquidity and strong demand for realistically-priced new projects with attractive locational attributes. Nonetheless, the weaker average take-up rate at 2023 new launches relative to 2022 reflects buyers’ selectiveness and growing resistance to the high prices, and developers should be prepared to take a longer time to clear each project. Launches that could be coming in the next few quarters include The LakeGarden Residences at Yuan Ching Road, TMW Maxwell, Altura EC and Newport Residences. Overall, CBRE Research expects 6,500 – 7,500 new private homes to be sold in 2023, consistent with the 7,099 units in 2022, which was a 14-year low since 2008’s 4,264 units. Stabilisation of interest rates should provide a clearer outlook in H2 2023 and bring back buyer confidence, especially owner-occupier demand.

• In the rental market, overall private residential rents have risen 10.2% in H1 2023 so far and are up 57.2% since bottoming in Q3 2020. Moving forward, the 11,810 private residential units (excl. ECs) expected to be completed in H2 2023 would inject a significant amount of stock into the market and alleviate the tight supply situation. In addition, we note expatriate demand has slowed with the economic slowdown and as temporarily-displaced owners move into their newly completed homes. Thus, we expect rents to start easing. Based on rental data collected in mid-July, we note median rents peaked in April 2023 and started to soften with June 2023 median rents softening by 3.9% compared to April’s, led by the CCR.

• However, rents are unlikely to fall back to pre-2022 levels, due to increased property taxes, higher prices (requiring higher returns), higher mortgage payments from higher interest rates, and higher rental demand from the newly imposed 15-month wait-out period for downgraders (buying resale HDB) under Sep 2022’s round of cooling measures. CBRE Research expects islandwide private property rents to decline 5% in H2 2023 for a full year increase of 5%.

• In view of the cooling measures effective 27 April 2023, CBRE Research believes home prices which have risen 3.1% in H1 2023 have peaked and are likely to flatten out in the next few quarters. Barring widespread retrenchments and a sustained recession, a significant price correction is not expected given low unsold inventory and generally healthy household balance sheets. As such, CBRE Research maintains its full year 2023 forecast for private home price growth of 3%, slower than the 8.6% seen in 2022 due mainly to a weaker economic outlook -- MTI forecasts 0.5 – 2.5% GDP growth for 2023, vs 3.6% for 2022.

URA Press Release:

https://www.ura.gov.sg/Corporate/Media-Room/Media-Releases/pr23-28

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.