Singapore

Commentary on Monthly New Home Sales for April 2025

May 15, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Developer sales in Apr 2025 eased for a second consecutive month on more lukewarm performance at new launches. 663 new private homes were sold in the month, down 9.1% m-o-m from 729 units in Mar 2025 but more than double the 301 units sold in Apr 2024 last year.

April’s sales take the tally of new homes sold in 2025 so far to 4,038 units. Buying sentiment has turned cautious against the backdrop of ongoing global trade frictions and geopolitical tensions which have dampened Singapore’s economic outlook.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

384 |

$2,948 |

41.0% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

107 |

$2,454 |

29.9% |

|

AURELLE OF TAMPINES (EC) |

TAMPINES STREET 62 |

99 yrs |

OCR |

54 |

$1,764 |

98.0% |

|

LUMINA GRAND (EC) |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

19 |

$1,509 |

97.1% |

|

PARKTOWN RESIDENCE |

TAMPINES STREET 62 |

99 yrs |

OCR |

17 |

$2,368 |

89.6% |

|

NOVO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

16 |

$1,609 |

96.8% |

|

GRAND DUNMAN |

DUNMAN ROAD |

99 yrs |

RCR |

14 |

$2,599 |

76.3% |

|

LENTOR MANSION |

LENTOR GARDENS |

99 yrs |

OCR |

12 |

$2,183 |

96.8% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

Freehold |

RCR |

11 |

$2,900 |

71.6% |

|

LENTOR CENTRAL RESIDENCES |

LENTOR CENTRAL |

99 yrs |

OCR |

11 |

$2,384 |

97.7% |

New launches in April 2025

|

Project Name |

Street Name |

Tenure |

Locality |

Total # of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

Units sold as % of total |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

937 |

937 |

384 |

$2,948 |

41% |

41% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

358 |

358 |

107 |

$2,454 |

30% |

30% |

|

21 ANDERSON |

ANDERSON ROAD |

Freehold |

CCR |

19 |

18 |

3 |

$4,811 |

17% |

16% |

Apr 2025 saw 3 new launches – 2 in the RCR and 1 in the CCR. City fringe launches included One Marina Gardens (937 units) and Bloomsbury Residences (358 units) while the prime launch was of ultra-luxury project 21 Anderson (19 units).

The top performing project was new launch One Marina Gardens (937 units) developed by Kingsford Group and located in the Marina South precinct at the fringe of the CBD. Despite its relatively attractive price point compared to other existing launches in the Downtown Core and high-floor units offering views of Gardens by the Bay, the project was met with a lukewarm response, moving 384 units (41% of total units) in Apr 2025 at a median price of $2,948 psf. Comparatively, major prior launches in Q1 2025 have recorded an average sell-through rate of 68% over their launch weekends.

The second best-selling private project was new launch Bloomsbury Residences (358 units) at Media Circle in the one-north precinct which was met with a subdued response, moving 107 units at a median price of $2,454 psf in April (30% of total units). This was followed by existing EC project Aurelle of Tampines (760 units) which was just launched in March. The project sold another 54 units at a median price of $1,764 psf.

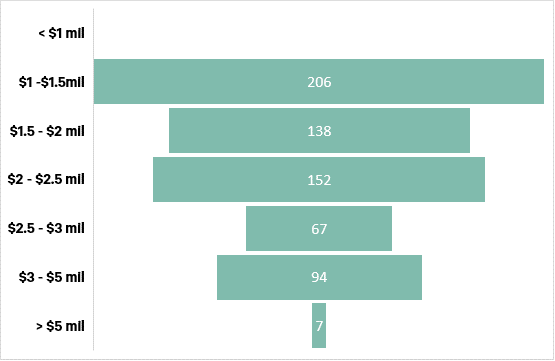

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 May 2025.

The Outside Central Region (OCR) was next, moving 95 units or 14.3% of total April new home sales, down from 596 units (81.8%) in Mar 2025.

Lastly, the Core Central Region (CCR) continued to underperform, 17 units were sold (2.6% of April sales), down from 46 units (6.3%) in Mar 2025 which saw the new launch of Aurea.

Outlook and forecasts

April’s sales take the tally of new homes sold in 2025 so far to 4,038 units. Q1 2025 saw new sales hold firm at 3,375 units, down only marginally by 1.3% q-o-q from the high base of 3,420 units in Q4 2024. However, buying sentiment has turned cautious against the backdrop of ongoing global trade frictions and geopolitical tensions which have dampened Singapore’s economic outlook, with the MTI cutting Singapore’s 2025 GDP growth forecast to 0 – 2% (from an initial 1 – 3%) as of 14 April.Looking ahead, most new launches for the rest of 2025 will be from the CCR and RCR, which have higher price points and may not generate the same kind of volumes as the attractively priced and voluminous OCR projects seen in Q1 2025. Developers might also choose to wait out the current period of heightened economic uncertainty and delay their launches until there is more clarity on the global trade and economic situation. CBRE Research thus maintains our full year new home sales to be 7,000 – 8,000 units, signalling a slowdown in new home sales in the next few quarters. There is downside risk to this projection should economic conditions worsen significantly.

Correspondingly, private home prices rose 0.8% q-o-q in Q1 2025, moderating from the 2.3% q-o-q increase in Q4 2024. We maintain a full-year 2025 private home price increase of 3 – 4% for now, on still-low unsold inventory and strong household balance sheets. Growth momentum could plateau in the next few quarters on a weaker economic outlook – MTI has cut Singapore’s 2025 GDP growth forecast to 0 – 2% (from an initial 1 – 3%) as of 14 Apr 2025.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.