Singapore

CBRE Commentary on Monthly New Home Sales for August 2023

September 15, 2023

Associated Contact

Head of Marketing & Communications, Singapore

New private home sales plunged 72.1% m-o-m from a 20-month high of 1,412 units in July to 394 units in Aug 2023, on fewer new launches and softening demand. Based on caveats downloaded from URA realis on 15 Sep, 68% of the new private homes sold in August were sold in the first half of August, before 16 Aug, as developers refrained from launching new projects after the start of the lunar seventh month on 16 Aug. Developers launched 590 units in Aug, 73% fewer than the 2,156 units in Jul 2023.

On a y-o-y basis, new home sales still declined 10% even as last year’s lunar seventh month fell between 29 Jul-26 Aug and there were no new condo launches in Aug 2022. Sentiment this year has clearly deteriorated with higher interest rates, softer economic prospects and two more rounds of cooling measures since.

This was also the third lowest monthly private home sales in 2023-to-date (after Jun’s 298 units and Jan’s 393 units), and brings cumulative new home sales in 2023 to 5,189, -5.6% from the 5,496 units sold over the corresponding period in 2022.

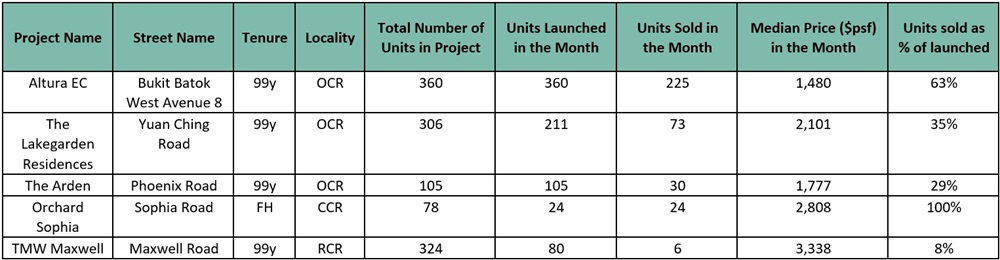

New launches in Aug 2023

Source: CBRE Research, URA

Aug 2023 saw 4 new private launches, 2 in the OCR - The Lakegarden Residences and The Arden, 1 in the RCR – TMW Maxwell, and 1 in the CCR - Orchard Sophia. These 4 new private launches sold 133 units in Aug, paled in comparison to the 1,159 units sold for the 4 new launches in July. Performance varied with the OCR projects doing better based on absolute volumes but all managed to sell 31% and below in terms of percentage of their total units available, compared to 29-56% for the new launches in July. ECs still outperformed private new launches with Altura EC (360 units) in Bukit Batok debuting and selling 63% (225 units) in its first month.

The Arden in the OCR sold 30 units or 29% of total 105 units at a median price of S$1,777 psf. The only CCR and freehold new launch in Aug -- Orchard Sophia sold 24 units or 31% of its 78 units at a median price of $2,808 psf, while TMW Maxwell, in RCR but is located within close proximity to the CBD, sold 6 or 2% of its 324 units at a median price of $3,338 psf.

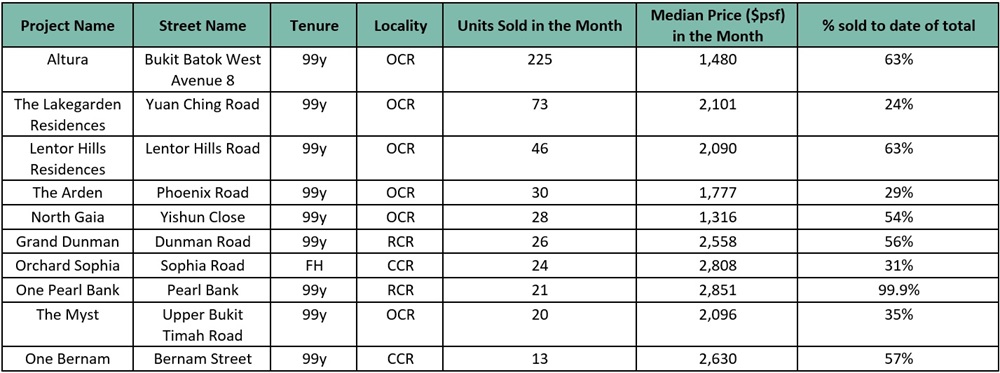

Top 10 Selling Projects in Aug 2023 (including ECs and landed)

Source: CBRE Research, URA

The top performing project in the month was Altura EC which sold 225 units at a median price of S$1,480psf. A distant second is The Lakegarden Residences which sold 73 (24%) units at a median price of S$2,101 psf. The third best-selling project in August was Lentor Hills Residences, launched in July, which sold another 46 units in August to bring cumulative sales to 63%.

Outlook

Year-to-Aug 2023 new home sales currently stand at 5,189 units, a 5.6% y-o-y fall from 5,496 units sold over the correspondingly period in 2022. We are of the view that the souring macro backdrop, elevated interest rate hikes and cooling measures have slowed demand, though this has become more prominent with the abundant new launches that have come through over Jul-Aug.

Slowdown in new launch take-up

In 2022, developers launched 15 new private residential projects with 4,528 units (excluding ECs) for sale. While this year to date, CBRE Research estimates that developers have already launched 17 private non-landed residential projects with a total of 6,773 units. We believe the pent-up demand has been mostly absorbed and genuine buyers are now spoilt for choice. In addition, prices have already moved up significantly and investors could feel that there is limited room for upside. Some of the projects which are targeted at investors or typically have higher foreigner buyers will face some resistance given the recent cooling measures doubling foreigners’ ABSD to 60% as well as a further increase in ABSD rate for investors. These investors will reassess their options and take a longer time to shop around.

Recent land sales have shown increased caution among developers

On 12 Sep, two suburban land tenders at Woodlands South and Lentor Central closed amid lukewarm response. We note that since the cooling measures in April 2023, developers displayed low risk appetites, preferring sites with fewer than 500 buildable units and hence, lower risk of not being able to sell everything within the five-year ABSD timeframe; as well as sites in the suburbs where demand is less affected by cooling measures, and those with differentiating factors such as proximity to transport nodes, good schools and limited competing supply.

Forecasts

Launches that could be coming in the next few quarters include J’den, The Hill@one north and Newport Residences.

Overall, CBRE Research expects 6,500 – 7,000 new private homes to be sold in 2023, potentially below the 7,099 units in 2022, which was already a 14-year low since 2008’s 4,264 units.

Correspondingly, CBRE Research believes home prices which have risen 3.1% in H1 2023 have peaked and are likely to flatten out in the next few quarters. Barring widespread retrenchments and a sustained recession, a significant price correction is not expected given low unsold inventory and generally healthy household balance sheets. As such, CBRE Research maintains its full year 2023 forecast for private home price growth of 3%, slower than the 8.6% seen in 2022 due mainly to a weaker economic outlook -- MTI forecasts 0.5 – 1.5% GDP growth for 2023, vs 3.6% for 2022.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.