Singapore

Commentary on Monthly New Home Sales for August 2025

September 15, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Developer sales in Aug 2025 surged for the second consecutive month to the highest level in 2025-to-date on bumper new launches prior to the start of the Seventh Lunar month on 23 Aug 2025. Developers launched 2,496 new units in the month, 49% higher m-o-m from 1,675 units in Jul 2025.

Correspondingly, 2,142 new private homes were sold, up 127.9% m-o-m from 940 units in Jul 2025 and 9-fold the 211 units moved in Aug 2024. This is the highest monthly record of new sales for the year so far and since 2,560 units were sold in Nov 2024.

August’s sales take the tally of new homes sold in the year-to-August to 7,669 units, already 18.6% higher than 2024’s full-year volume of 6,469 units. This comes on the back of strong buying sentiment amid low interest rates and better-than-expected economic performance despite persistent trade uncertainty and geopolitical tensions, with MTI upgrading its 2025 GDP growth forecast to 1.5 – 2.5% from a prior 0 – 2%.

Top 10 Selling Projects in August 2025 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

SPRINGLEAF RESIDENCE |

UPPER THOMSON ROAD |

99 yrs |

OCR |

884 |

$2,166 |

93.9% |

|

RIVER GREEN |

RIVER VALLEY GREEN |

99 yrs |

CCR |

451 |

$3,111 |

86.1% |

|

PROMENADE PEAK |

ZION PROMENADE |

99 yrs |

RCR |

333 |

$2,919 |

55.9% |

|

CANBERRA CRESCENT RESIDENCES |

CANBERRA CRESCENT |

99 yrs |

OCR |

211 |

$1,991 |

56.1% |

|

OTTO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

191 |

$1,760 |

90.2% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

25 |

$2,565 |

57.8% |

|

UPPERHOUSE AT ORCHARD BOULEVARD |

ORCHARD BOULEVARD |

99 yrs |

CCR |

22 |

$3,353 |

66.1% |

|

ARTISAN 8 |

SIN MING ROAD |

Freehold |

RCR |

15 |

$2,386 |

44.1% |

|

THE ROBERTSON OPUS |

UNITY STREET |

999 yrs |

CCR |

15 |

$3,308 |

46.6% |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

13 |

$2,909 |

54.9% |

New launches in August 2025

|

Project Name |

Street Name |

Tenure |

Locality |

Total no. of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

|

ARTISAN 8 |

SIN MING ROAD |

Freehold |

RCR |

34 |

34 |

15 |

2386 |

44% |

|

CANBERRA CRESCENT RESIDENCES |

CANBERRA CRESCENT |

99 yrs |

OCR |

376 |

376 |

211 |

1991 |

56% |

|

PROMENADE PEAK |

ZION PROMENADE |

99 yrs |

RCR |

596 |

596 |

333 |

2919 |

56% |

|

RIVER GREEN |

RIVER VALLEY GREEN |

99 yrs |

CCR |

524 |

524 |

451 |

3111 |

86% |

|

SPRINGLEAF RESIDENCE |

UPPER THOMSON ROAD |

99 yrs |

OCR |

941 |

941 |

884 |

2166 |

94% |

There were 5 new launches in Aug 2025, 4 major launches and 1 boutique project spread across all market segments. The OCR saw the launch of Springleaf Residence (941 units) and Canberra Crescent Residences (376 units), the CCR observed the launch of River Green (524 units) and the RCR recorded the launch of Promenade Peak (596 units) and boutique freehold project Artisan 8 (34 units).

All of the new launches made it to the top 10 best-selling projects in the month, led by Springleaf Residence (941 units) which saw robust take-up given its attractive price point, moving 941 units (94% of total units) in the month at a median price of $2,166 psf, making it the best performing new launch in terms of % sold for 2025 so far.

- The next best-selling project was River Green (524 units) which sold 451 or 86% of its 524 total units at a median price of $3,111 psf, far surpassing the 59% of total units sold at Upperhouse at Orchard Boulevard (301 units) last month and making it the best-selling CCR project in the year so far and at least the past 10 years. By shrinking unit sizes, the developer, Wingtai Holdings was able to keep the quantum palatable for most units, making it affordable for a larger proportion of buyers.

- Competing launch, Promenade Peak (596 units) located nearby to River Green was the third best-selling project, moving 333 units or 56% of its 596 total units at a median price of $2,919 psf. The project featured larger-format units that appealed to buyers purchasing for own-stay.

- Canberra Crescent Residences (376 units) was the fourth top performing project, seeing 56% take-up, with 211 units sold at a median price of $1,991 psf.

- For its small size, Artisan 8 sold a respectable 44% or 15 units at a median price of $2,386 psf during launch.

By market segment, August 2025’s developer sales (excluding ECs) were again led by the Outside Central Region (OCR) which recorded the sale of 1,153 units (53.8%) from 70 units (7.4%) of total new sales in Jul 2025. This was largely attributed to robust take-up a top-selling project Springleaf Residence and healthy performance at Canberra Crescent Residences.

- Similar to last month, the Core Central Region (CCR) fared well, moving 513 units (23.9% of August sales) compared to 357 units in July (38%) mainly due to the success of River Green.

- The Rest of Central Region (RCR) was comparable to the CCR, only trailing slightly behind. 476 units or 22.2% of total August sales were recorded, matching the 513 units (54.6%) in Jul 2025.

*Based on Realis new sales (excl. EC) caveats extracted on 15 Sep 2025.

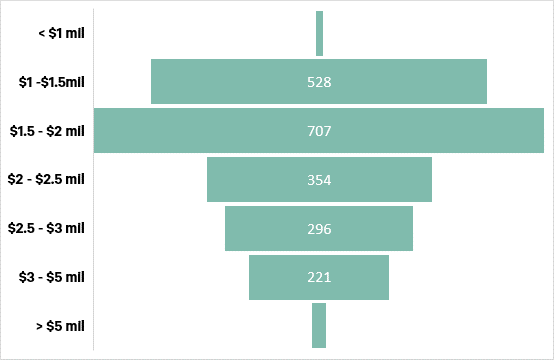

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) at 33% was actually in the S$1.50 – 2.00 mil range which is the sweet spot for 2-bedders from the new launches. The $1.00 – 1.50 mil range was second at 25%.

Outlook and forecasts

While the bulk of major projects have already been launched, there are still a few anticipated launches for the remainder of the year. Zyon Grand (706 units) located on the hybrid SA2 site adjacent to Promenade Peak could ride on the success of the latter. Penrith (462 units) situated on Margaret Drive GLS could also see strong pent-up demand from upgraders in the area which has not seen a new condo launch in 7 years since Margaret Ville was launched in May 2018. 666-unit Skye at Holland next to the popular Holland Village is also keenly watched.

With the current tally of new sales in the year-to-August at 7,669 units already exceeding FY2024’s 6,469 units, CBRE Research now expects the full year 2025 new home sales could reach 8,000 – 9,000 units, above our prior forecast of 7,000 – 8,000 units.

Correspondingly, private home prices which have risen 1.8% in H1 2025 could see similar growth momentum in H2 2025. We maintain a full-year 2025 private home price increase of 3 – 4% for now, on still-low unsold inventory and strong household balance sheets.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.