Singapore

Commentary on Monthly New Home Sales for December 2024

January 15, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Following robust sales in November from a host of attractive new launches, December’s private new home sales sunk to the second lowest level in 2024 on the absence of new launches and December holiday lull. Sales fell 92.1% m-o-m but were up 50.3% y-o-y at 203 units, the second lowest reading in 2024, just above the 153 units recorded in Feb 2024.

December’s sales take the tally of new homes sold for the whole of 2024 to 6,560 units, up 2.2% y-o-y from 2023’s 6,421 units which was a 15-year low for developer sales since 4,264 units were sold in 2008 during the Global Financial Crisis.

Developer sales leading up to 9M 2024 had been much weaker as sentiment was dented by elevated interest rates, high price points and the lack of attractive launches. However sentiment and sales saw a strong rebound in Q4 2024, catalysed by lower mortgage rates and strong pent-up demand for attractively-priced major new launches in the quarter.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

NOVO PLACE EC |

PLANTATION CLOSE |

99 yrs |

OCR |

158 |

$1,647 |

88% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

19 |

$2,278 |

77% |

|

THE MYST |

UPPER BUKIT TIMAH ROAD |

99 yrs |

OCR |

17 |

$2,080 |

77% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

FH |

RCR |

15 |

$2,864 |

67% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

11 |

$2,543 |

69% |

|

CHUAN PARK |

LORONG CHUAN |

99 yrs |

OCR |

11 |

$2,657 |

79% |

|

SORA |

YUAN CHING ROAD |

99 yrs |

OCR |

10 |

$2,198 |

33% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

9 |

$2,175 |

78% |

|

THE COLLECTIVE AT ONE SOPHIA |

SOPHIA ROAD |

99 yrs |

CCR |

9 |

$2,758 |

18% |

|

LENTORIA |

LENTOR HILLS ROAD |

99 yrs |

OCR |

7 |

$2,291 |

68% |

|

NAVA GROVE |

PINE GROVE |

99 yrs |

RCR |

7 |

$2,612 |

70% |

December 2024 saw no new private launches as developers held back in view of the December holiday season lull. As such, the top three best performing projects were existing launches, including 1 EC project, Novo Place (504 units) which was also the top performer in the month. Launched just a month ago in Nov 2024, said project sold another 158 units at a median price of $1,647 psf and was 88% sold.

The next 2 best performing projects were Hillock Green (474 units) at Lentor Central which sold another 19 units at a median price of $2,278 psf, followed by The Myst (408 units) which moved 17 units at a median price of $2,080 psf. These 2 projects have each sold 77% of their total units as of December.

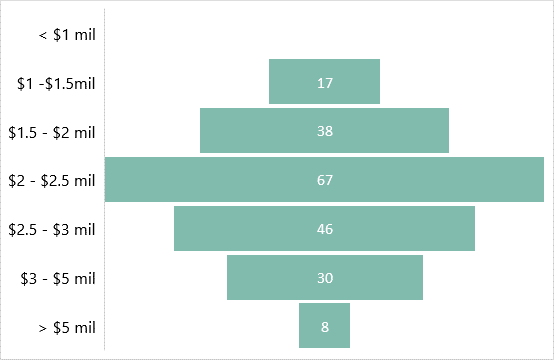

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Jan 2025.

By market segment, Decembers 2024’s developer sales (excluding ECs) were led by the Outside Central Region (OCR). 111 units or 54.7% of total December new home sales were sold in the OCR, down from 893 units (34.9%) in November. The Rest of Central Region (RCR) sold 73 units (36% of December sales), down from 1,569 units (61.3%) in November 2024. Lastly, the Core Central Region (CCR) moved 19 units (9.4% of December sales), compared to 98 units (3.8%) in November.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$2.00 – 2.50 mil range at 32.5% as buyers scooped up larger units at existing launches. This was followed by the S$2.50 mil – S$3.00 mil bracket at 22.3%.

Outlook and Forecasts

CBRE Research is cautiously optimistic on the private residential market in 2025. We forecast 7,000 – 8,000 new homes to be sold in 2025, an improvement from 2024’s 6,560 units on easing interest rates and better buying sentiment. However, while general take-up rates across new projects are expected to improve, buyers could remain selective in 2025 amid a myriad of new launch options. Attractive developer pricing remains key to healthy new launch performance.

Correspondingly, private residential prices rose 3.9% in 2024, a moderation from 2023’s 6.8% growth. With interest rate cuts of 100bps since Sep 2024 and likely to continue its downward trajectory (albeit may not be by much), private home prices should continue rising in 2025. Barring an economic recession or reversal of interest rate cuts and additional cooling measures, CBRE forecasts average private home prices to rise at a moderate pace of 3 – 6% in 2025 on lower interest rates, strong household balance sheets, still-low unsold inventory and an attractive pipeline of new launches which could set benchmark prices.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.