Singapore

Commentary on Monthly New Home Sales for December 2025

January 15, 2026

Associated Contact

Head of Marketing & Communications, Singapore

In the absence of major new launches amid the December holiday lull, developer sales in December sank to the lowest level in 2025. Nonetheless, the year still closed at a multi-year high on earlier surges.

In December, 197 new private homes were sold, down 39.4% m-o-m from 325 units in Nov 2025 and 3% y-o-y from the 203 units moved in Dec 2024. This is the lowest monthly record of new sales for 2025 and since 153 units were sold in Feb 2024.

December’s sales take the tally of new homes sold in Q4 2025 to 2,946 units, down 10.4% q-o-q from the high base of 3,288 units in Q3 largely due to fewer launches – there were 5 major launches in Q4 2025 compared to 8 in Q3 – and the December holiday lull. Homebuying appetite remained strong in the quarter amid low interest rates and economic outperformance, with new launches generally recording robust take-up.

This brings 2025 new homes sold to 10,821 units, up 67.3% from the 6,469 units in 2024, the highest since 2021, amid lower interest rates, pent-up demand and bumper new launches.

Top 10 Selling Projects in December 2025 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

Freehold |

RCR |

31 |

$2,498 |

82.4% |

|

OTTO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

28 |

$1,751 |

98.3% |

|

POLLEN COLLECTION II (LANDED) |

POLLEN RISE / POLLEN LANE / POLLEN TERRACE / POLLEN CRESCENT |

99 yrs |

OCR |

17 |

$2,599 |

9.1% |

|

NAVA GROVE |

PINE GROVE |

99 yrs |

RCR |

15 |

$2,641 |

93.8% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

8 |

$2,593 |

92.3% |

|

AURELLE OF TAMPINES (EC) |

TAMPINES STREET 62 |

999 yrs |

OCR |

8 |

$1,932 |

100.0% |

|

CANBERRA CRESCENT RESIDENCES |

CANBERRA CRESCENT |

99 yrs |

OCR |

8 |

$2,008 |

79.0% |

|

UPPERHOUSE AT ORCHARD BOULEVARD |

ORCHARD BOULEVARD |

99 yrs |

CCR |

7 |

$3,410 |

73.4% |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

6 |

$3,066 |

59.4% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

6 |

$2,542 |

70.1% |

There was only 1 new launch in Dec 2025, 99-year leasehold landed project Pollen Collection II (186 units) located along Pollen Rise at Seletar Hills. The project sold 17 units (9% of its 186 total units) at a median price of $2,599 psf and was the 3rd best performer in the month.

Other top performing projects were all existing launches, including 2 EC projects. The top performing launch was freehold project The Continuum (816 units) – located along Thiam Siew Avenue – which sold 31 more units at a median price of $2,498 psf after dangling a “one price” promotion for its 1+study units starting at $1.338 mil, implying about 10-15% discount from its launch price of $2,800 psf. The price looks attractive for a freehold project in a RCR location, comparable to most of the 99-year leasehold projects in an equivalent location. 816-unit The Continuum was launched in May 2023 and sold 27% at a median price of $2,720psf in the first month.

The 2nd top performer was Otto Place EC (600 units) which was launched in Jul 2025. The project moved another 28 units at a median price of $1,751 psf and was 98% sold.

By market segment, December 2025’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR). 110 units or 56% of total December sales were recorded, compared to 215 units (66%) in Nov 2025.

- The Outside Central Region (OCR) moved 67 units or 34% of total December sales after 80 units (25%) in Nov 2025.

- The Core Central Region (CCR) moved 20 units (10% of total September sales), down from 30 units (9%) in November.

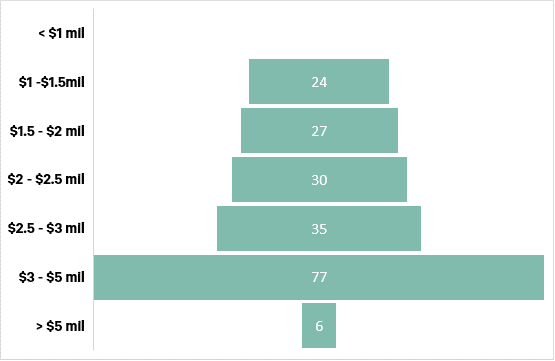

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Jan 2026.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) at 39% was actually in the S$3.00 – 5.00 mil range from transactions at new landed launch Pollen Collection II and larger 4-bedroom units at existing city fringe launches Nava Grove and Pinetree Hill. The $2.50 – 3.00 mil range was second at 18%.

Outlook and forecasts

December’s sales take the tally of new homes sold for the full year of 2025 to 10,821 units, 67.3% higher y-o-y from the 6,469 units sold in 2024 and a 4-year high since 13,027 units were sold in 2021.2025 was a rocky year amid heightened global economic uncertainty from the unpredictability of US trade policies which caused new sales to slump in Q2 2025 after a bumper Q1. Nevertheless, the significant fall in domestic interest rates (3-month SORA was down more than 180 bps at 1.19% on 31 Dec compared to 3.02% on 3 Jan 2025) and pent-up demand alongside the attractive pipeline of new launches bolstered the market which saw a strong rebound in H2 2025.

Looking ahead to 2026, 2 announced launches would kickstart the year in January, 99y suburban project Narra Residences (540 units) at Dairy Farm Walk and freehold CBD project Newport Residences (246 units) which is the residential component of the redevelopment of Fuji Xerox Towers. Overall, buying sentiment and appetite is expected to remain strong in 2026 but sales volumes may ease with fewer launches expected and as interest rate declines taper. Compared to the 11,482 units launched in 2025, an estimated 9,500 – 10,500 units could potentially be launched in 2026. Correspondingly, CBRE Research expects 7,500 – 8,500 new homes to be sold.

Private home prices, which rose 3.4% in 2025 (based on Q4 flash estimate) and have cumulatively risen 42.4% since Covid trough in Q1 2020, could grow at a slower or similar pace in 2026. We forecast private home prices to grow 2 – 4%, relatively in line with forecasted 2026 GDP growth – MTI projects FY2026 GDP growth of 1 – 3%, a moderation from 4.8% for 2025.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.