Singapore

CBRE Commentary on Monthly New Home Sales for February 2024

March 15, 2024

Associated Contact

Head of Marketing & Communications, Singapore

Feb 2024 private home sales sank to a historic low for the month of February after a rebound in January on the absence of new launches amid the Chinese New Year lull.

New home sales almost halved m-o-m to 149 units in Feb 2024 from 281 units in Jan 2024. This was a historic low for the month of February, below the previous low of 174 units recorded in Feb 2008.

On a y-o-y basis, developer sales were down 66% y-o-y from 433 units in Feb 2023. This is largely attributed to the absence of new launches in the month, with developers choosing to hold back launches amid the Chinese New Year seasonal lull. Developer sales have also been tepid since 2023, hitting a 15-year low of 6,421 units for the full year on weak economic conditions, buyer fatigue and increasing resistance to high price points.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

LUMINA GRAND (EC) |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

16 |

$1,497 |

55.9% |

|

THE BOTANY AT DAIRY FARM |

DAIRY FARM WALK |

99 yrs |

OCR |

15 |

$2,018 |

65.3% |

|

NORTH GAIA (EC) |

YISHUN CLOSE |

99 yrs |

OCR |

14 |

$1,327 |

66.9% |

|

BLOSSOMS BY THE PARK |

SLIM BARRACKS RISE |

99 yrs |

RCR |

10 |

$2,585 |

86.5% |

|

GRAND DUNMAN |

DUNMAN ROAD |

99 yrs |

RCR |

10 |

$2,532 |

62.5% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

10 |

$2,468 |

36.9% |

|

LENTOR HILLS RESIDENCES |

LENTOR HILLS ROAD |

99 yrs |

OCR |

8 |

$2,099 |

76.8% |

|

THE MYST |

UPPER BUKIT TIMAH ROAD |

99 yrs |

OCR |

8 |

$2,238 |

51.5% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

8 |

$2,242 |

36.1% |

|

THE LANDMARK |

CHIN SWEE ROAD |

99 yrs |

RCR |

6 |

$2,858 |

87.4% |

With no new launch in Feb 2024, most sales were from previously launched projects. 2 of the top 3 best performing projects were EC developments and all of the top 10 were located in either the OCR or RCR.

The top performing project in the month was EC development, Lumina Grand just launched in Jan 2024 which sold another 16 units at a median price of $1,497 psf. Following close behind was The Botany at Dairy Farm which sold 15 units at a median price of $2,018 psf. The third best-selling project was another EC project, North Gaia which was launched in Apr 2022 and sold another 14 units in Feb 2024 to bring cumulative sales to 67%.

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Mar 2024.

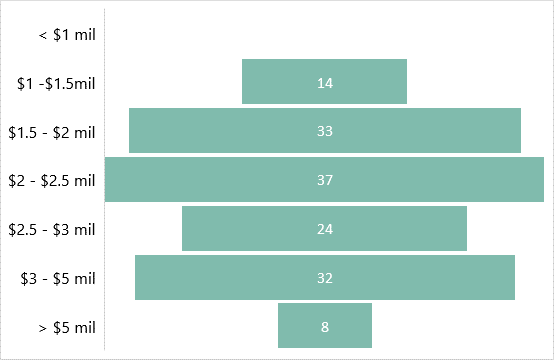

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$2.00 mil - S$2.50 mil range at 25%. This was followed by the S$1.50 mil – S$2.00 mil bracket at 22.3%.

Outlook and forecasts

2023 new home sales hit a 15-year low at 6,421 units, 9.6% below the 7,099 units in 2022 amid repeated rounds of cooling measures, a softening economic backdrop and elevated interest rates. Buyers have turned more selective amid a myriad of new launch options, buyer fatigue and increasing resistance to high price points.

Homebuyers’ tentative stance appears to be persisting in Q1 2024, coupled with negative newsflows from a slew of company layoffs, albeit globally which could have further dented buying sentiment to start the year.

Looking ahead, sales in Mar 2024 are set to pick up on more launches, with 2 new project launches in the Lentor area, Lentoria (267 units) and Lentor Mansion (533 units). It was reported that the former moved 50 of its 267 total units (18.7%) at an average price of $2,120 psf over its Mar 2 – 3 launch weekend while the latter is expected to launch tomorrow during the 16 Mar weekend. While said launches could offer a temporary boost to monthly sales figures, a more significant recovery in developer sales is only anticipated in H2 2024 if interest rates ease and the economy recovers.

Nevertheless, there is a healthy pipeline of potential new launches in 2024 which could support 2024 sales when buying sentiment improves. Notable projects include OCR projects Sora (440 units), city fringe launch The Hill@One-North (142 units) and CBD project Marina View Residences (683 units).

Overall, CBRE Research is cautiously optimistic on the private residential market in 2024. We expect forecast 7,000 – 8,000 new homes could be sold in 2024, an improvement from the 6,421 units in 2023 but still below the 5-year average new developer sales across 2019 – 2023 of 9,288 units. In the near term, downbeat macroeconomic conditions, cooling measures and elevated interest rates are likely to continue weighing on the private residential market but sentiment could improve in H2 2024 if interest rates ease and the economy recovers.

Correspondingly, private residential prices could rise 3 – 4% in 2024, slowing from 2023’s 6.8%. A significant correction is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.