Press Release

Commentary on Monthly New Home Sales for February 2025

March 17, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Developer sales continued their advance in Feb 2025 on attractive new launches. Private new home sales rose 45.4% m-o-m to 1,575 units in the month from 1,083 units recorded in Jan 2025. Sales were also 10 times the 153 units in Feb 2024 and posted a 13-year high for the month of February since 2,417 units were moved in Feb 2012.

This follows the uptick in market activity in Q4 2024 which took the tally of new home sales for 2024 to 6,469 units, up 0.7% y-o-y from 2023’s 6,421 units which was a 15-year low for developer sales since 4,264 units were sold in 2008 during the Global Financial Crisis. Buying sentiment and appetite has improved amid lower mortgage rates and as developers push ahead with major launches.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

PARKTOWN RESIDENCE |

TAMPINES STREET 62 |

99 yrs |

OCR |

1041 |

$2,363 |

87% |

|

ELTA |

CLEMENTI AVENUE 1 |

99 yrs |

OCR |

326 |

$2,538 |

65% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

22 |

$2,613 |

77% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

18 |

$2,098 |

85% |

|

NAVA GROVE |

PINE GROVE |

99 yrs |

RCR |

18 |

$2,574 |

75% |

|

NOVO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

17 |

$1,676 |

89% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

13 |

$2,216 |

85% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

FH |

RCR |

10 |

$2,906 |

69% |

|

KASSIA |

FLORA DRIVE |

FH |

OCR |

9 |

$2,065 |

71% |

|

TERRA HILL |

YEW SIANG ROAD |

FH |

RCR |

8 |

$2,574 |

49% |

New launches in February 2025

|

Project Name |

Street Name |

Tenure |

Locality |

Total # of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

|

PARKTOWN RESIDENCE |

TAMPINES STREET 62 |

99 yrs |

OCR |

1193 |

1193 |

1041 |

2363 |

87% |

|

ELTA |

CLEMENTI AVENUE 1 |

99 yrs |

OCR |

501 |

501 |

326 |

2538 |

65% |

Feb 2025 saw 2 new suburban condo launches – integrated mega-project Parktown Residence (1,193 units) in Tampines and Elta (501 units) in Clementi. Located at suburban neighbourhoods which have not seen new supply in at least the past 5 years, both projects saw strong pent-up demand and robust take-up.

Parktown Residence (1,193 units) clinched the spot as the top performing project in the month, selling 1,041 units or 87% of total units at a median price of $2,363 psf in February. The key draw for the launch was its unique status as an integrated development with direct access to a host of amenities including a retail mall, the future Tampines North MRT station on the Thomson-East Coast Line, and a bus interchange.

The second best-selling project was new launch Elta (501 units) in Clementi, which sold 326 units, 65% of total units at a median price of $2,538 psf in February. The launch benefitted from pent-up demand due to its location in the mature Clementi estate which has not seen a new launch in 5 years since Clavon in 2020.

The third performing project was existing launch Pinetree Hill (520 units) which moved another 22 units at a median price of $2,613 psf

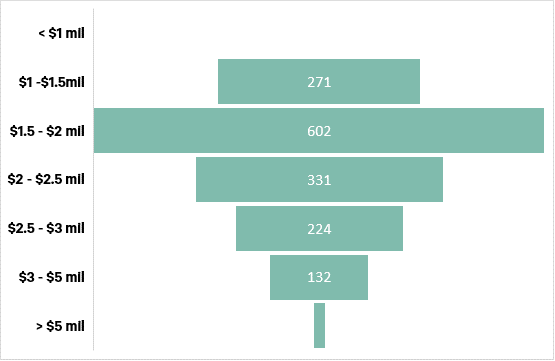

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 17 Feb 2025.

By market segment, Feb 2025’s developer sales (excluding ECs) were led by the Outside Central Region (OCR). 1,452 units or 92.2% of total February new home sales came from the OCR due to strong sales at Elta and Parktown Residence, up from 191 units (17.6%) in Jan 2025. 98 units or 6.2% of total February new home sales were from the Rest of Central Region (RCR), down from 771 units (71.2%) in Jan 2025. Lastly, the Core Central Region (CCR) moved 25 units (1.6% of February sales), compared to 121 units (11.2%) in Jan 2025.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 – 2.00 mil range at 38.2% which is the sweet spot for buyers of 2-bedder units at new launches. This was followed by the S$2.00 mil – S$2.50 mil bracket at 21.0%.

Outlook and forecasts

February’s sales take the tally of new homes sold in 2M2024 to 2,658 units, on track for Q1 2025 sales to match the 3,420 units sold in Q4 2024. Looking ahead, sales in March next month are expected to remain healthy, albeit slowing from Feb 2025’s high base. Media sources report that new launch Lentor Central Residences moved 445 units or 93% of its 477 units at an average price of $2,200 psf over its launch weekend.CBRE Research is cautiously optimistic on the private residential market in 2025. We forecast 7,000 – 8,000 new homes to be sold in 2025, an improvement from 2024’s 6,469 units on easing interest rates, better buying sentiment and an attractive pipeline of launches. However, while general take-up rates across new projects are expected to improve, buyers could remain selective in 2025 amid a myriad of new launch options. Attractive developer pricing remains key to healthy new launch performance.

Correspondingly, private residential prices rose 3.9% in 2024, a moderation from 2023’s 6.8% growth. Home prices are likely to continue rising in 2025 supported by strong household balance sheets, lower interest rates, and potential benchmark pricing at new launches. Barring an economic recession, interest rate hikes or additional cooling measures, CBRE Research forecasts a moderate price increase of 3 – 6% in 2025.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.