Singapore

Commentary on Monthly New Home Sales for January 2025

February 17, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Following the December holiday seasonal lull, developer sales saw a strong start to 2025 with a robust rebound in Jan 2025. Private new home sales surged five-fold to 1,083 units in the month from the 203 units recorded in Dec 2024. Sales were also up 256.3% y-o-y from 304 units in Jan 2024 and posted a 4-year high for the month of January since 1,633 units were moved in Jan 2021.

This follows the uptick in market activity in Q4 2024 which took the tally of new home sales for 2024 to 6,469 units, up 0.7% y-o-y from 2023’s 6,421 units which was a 15-year low for developer sales since 4,264 units were sold in 2008 during the Global Financial Crisis. Buying sentiment and appetite has improved amid lower mortgage rates and as developers push ahead with major launches.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

THE ORIE |

LORONG 1 TOA PAYOH |

99 yrs |

RCR |

680 |

$2,731 |

88% |

|

ONE BERNAM |

BERNAM STREET |

99 yrs |

CCR |

99 |

$2,521 |

99% |

|

BAGNALL HAUS |

UPPER EAST COAST ROAD |

FH |

OCR |

75 |

$2,494 |

66% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

21 |

$2,253 |

81% |

|

CHUAN PARK |

LORONG CHUAN |

99 yrs |

OCR |

20 |

$2,654 |

81% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

19 |

$2,559 |

73% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

FH |

RCR |

13 |

$3,001 |

68% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

11 |

$2,145 |

81% |

|

UNION SQUARE RESIDENCES |

HAVELOCK ROAD |

99 yrs |

RCR |

11 |

$3,333 |

30% |

|

NAVA GROVE |

PINE GROVE |

99 yrs |

RCR |

11 |

$2,555 |

72% |

New launches in January 2025

|

Project Name |

Street Name |

Tenure |

Locality |

Total no. of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

|

THE ORIE |

LORONG 1 TOA PAYOH |

99 yrs |

RCR |

777 |

777 |

680 |

2731 |

88% |

|

BAGNALL HAUS |

UPPER EAST COAST ROAD |

FH |

OCR |

113 |

113 |

75 |

2494 |

66% |

|

THE GATZ |

LOR 32 GEYLANG |

FH |

RCR |

6 |

6 |

0 |

- |

- |

Jan 2025 saw 3 new private launches - The Orie (777 units) in Toa Payoh, Bagnall Haus (113 units) at Upper East Coast and boutique project The Gatz (6 units) located in Geylang.

New launch The Orie (777 units) clinched the spot as the top performing project in the month, benefitting from its attractive location near Braddell MRT and in the mature Toa Payoh estate. The project saw robust take-up, selling 680 units or 88% of total units at a median price of $2,731 psf on the back of pent-up demand as the first new Toa Payoh launch in 9 years since Gem Residences in 2016.

Second best-selling project was 351-unit One Bernam in Tanjong Pagar, which sold 99 units at a median price of $2,521 psf in January, after cutting prices by up to 27%. One Bernam first launched in May 2021 and sold 83 units at a median price of $2,471 psf then, mainly for low-floor units.

The third performing project was new launch 113-unit Bagnall Haus, selling 75 units or 66% of total units at a median price of $2,494 psf. The key draws for this project include its attractive pricing for a freehold tenure and its location next to the upcoming Sungei Bedok MRT Station - an interchange for the Downtown and Thomson-East Coast lines.

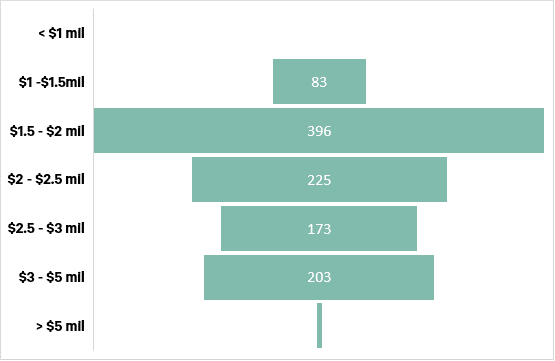

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 17 Jan 2025.

By market segment, Jan 2025’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR). 771 units or 71.2% of total January new sales came from the RCR, up from 73 units (36%) in Dec 2024. 191 units or 17.6% of total January new home sales were from the Outside Central Region (OCR), up from 111 units (54.7%) in Dec 2024. Lastly, the Core Central Region (CCR) moved 121 units (11.2% of January sales), compared to 19 units (9.4%) in Dec 2024, due to One Bernam’s fire sale. While the rest of the high-end market remained largely quiet, 54-unit ultra luxurious Park Nova stood out, with two units sold in January 2025 at high price points. The largest penthouse of Park Nova, measuring 5,899 sq ft, was sold by the developer for $38.888 million, or about $6,593 psf. This marks the highest recorded for a unit at Park Nova by both absolute price and psf-price. Also in the same month, a four-bedroom apartment spanning 2,906 sq ft on the 19th floor had fetched $16.59 million ($5,708 psf).

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 – 2.00 mil range at 36.5% which is the sweet spot for buyers of 2-bedder units at new launches. This was followed by the S$2.00 mil – S$2.50 mil bracket at 20.7%.

Outlook and Forecasts

Next month’s sales are shaping up to surpass Jan 2025 already strong showing with attractive projects Elta (501 units) at Clementi Avenue 1 and ParkTown Residence (1,193 units) at Tampines Avenue 11 slated to launch over the 22 February weekend. Said 2 projects are poised to see robust pent-up demand from the lack of supply in their respective neighbourhoods.

CBRE Research is cautiously optimistic on the private residential market in 2025. We forecast 7,000 – 8,000 new homes to be sold in 2025, an improvement from 2024’s 6,469 units on easing interest rates, better buying sentiment and an attractive pipeline of launches. However, while general take-up rates across new projects are expected to improve, buyers could remain selective in 2025 amid a myriad of new launch options. Attractive developer pricing remains key to healthy new launch performance.

Correspondingly, private residential prices rose 3.9% in 2024, a moderation from 2023’s 6.8% growth. Home prices are likely to continue rising in 2025 supported by strong household balance sheets, lower interest rates, and potential benchmark pricing at new launches. Barring an economic recession, interest rate hikes or additional cooling measures, CBRE Research forecasts a moderate price increase of 3 – 6% in 2025.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.