Singapore

CBRE Commentary on Monthly New Home Sales for July 2023

August 15, 2023

Associated Contact

Head of Marketing & Communications, Singapore

New home sales surged to a yearly high in Jul 2023 on the back of a host of attractive new launches. Developers launched 2,156 units in Jul 2023, a high since 2,600 units launched in Jan 2021.

New developer sales (excluding ECs) in Jul 2023 surged more than five-fold m-o-m to 1,412 units from Jun 2023’s 278 units, and up 68.9% y-o-y from Jul 2022’s 836 units. This was the highest monthly sales in 2023-to-date, and also the highest monthly sales since 1,547 units in Nov 2021, reflecting liquidity and strong demand for new projects with attractive locational attributes despite high interest rates, tightened financing conditions and downbeat economic conditions.

Year-to-July 2023 new home sales currently stand at 4,795 units, a marginal 5.2% y-o-y fall from 5,058 units sold over the correspondingly period in 2022.

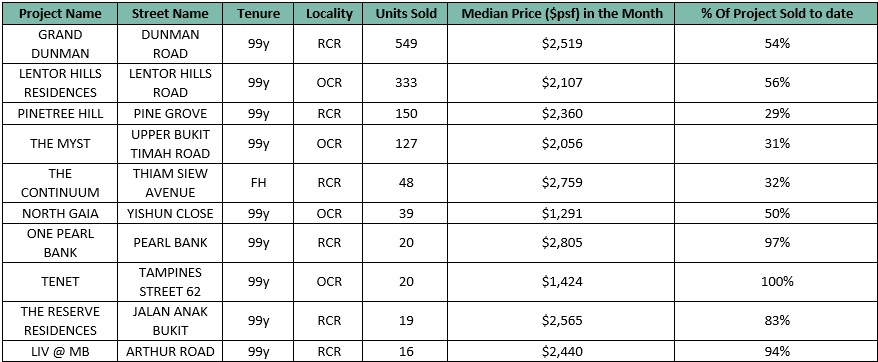

Top 10 Selling Projects in Jul 2023 (including ECs and landed)

Source: CBRE Research, URA

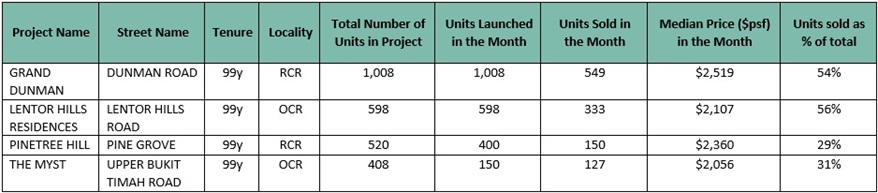

Jul 2023 saw 4 major new launches, 2 from the RCR – Grand Dunman (1,008 units) and Pinetree Hill (520 units) – and 2 from the OCR – Lentor Hills Residences (598 units) and The Myst (408 units). Said new launches were also the top performing projects in the month.

The top performing project in the month was RCR mega project, Grand Dunman (1,008 units) which moved 549 units or 54% of its total units at a median price of $2,519 psf. Jointly developed by SingHaiyi Group and CSC Land Group, the project benefitted from its proximity to several good schools (Kong Hwa School, Chung Cheng High School and Tanjong Katong Girls’ School), Dakota MRT Station, the Paya Lebar commercial precinct and the CBD.

The next best performing project in the month was OCR new launch, Lentor Hills Residences (598 units) developed by UOL and Singapore Land Group. The development sold 333 units (56%) at a median price of $2,107 psf, appealing to families with young children given its proximity to popular schools such as Henry Park and Pei Tong Primary School.

This was followed by new launches Pinetree Hill (520 units) and The Myst (408 units) which sold 150 (29%) and 127 units (31%) at median prices of $2,360 psf and $2,056 psf respectively.

New launches in Jul 2023

Source: CBRE Research, URA

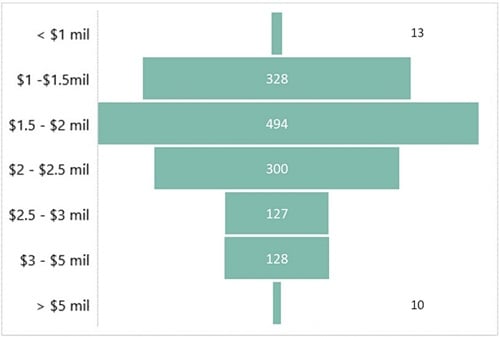

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Aug 2023.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 mil - S$2.00 mil range at 35.3%. This was followed by the S$1.00 mil – S$1.50 mil bracket at 23.4%.

By market segment, Jul 2023’s developer sales (excluding ECs) were skewed towards the Rest of Central Region (RCR) where 836 units (59.2%) were sold, followed by the Outside Central Region (OCR) where 488 units (34.6%) were sold and the Core Central Region (CCR) which saw the sale of 88 units (6.2%). This compares to 40.3% in the CCR, 52.9% in the RCR and 6.8% in the OCR in Jun 2023.

Outlook

Year-to-July 2023 new home sales currently stand at 4,795 units, a marginal 5.2% y-o-y fall from 5,058 units sold over the correspondingly period in 2022. While July sales had been stellar, sentiment has softened significantly going by how the new launches have done in August -- five new launches in August so far have yielded weaker sales. Altura EC and The Lakegarden Residences launched in the first weekend of August sold 220 (61%) and 71 (23%) units respectively, while the three new project launches in the second weekend of August only managed to sell 53 units in their first weekend. The worst-performing projects were in the CCR -- Orchard Sophia sold 19 or 24% of its 78 units and TMW Maxwell sold 7 or 2% of its 324 units. The Arden in the OCR sold 27 or 26% of 105 units.

Slowdown in new launch take-up

In 2022, developers launched 15 new private residential projects with 4,528 units (excluding ECs) for sale. While this year to date (up to weekend of 12 Aug), CBRE Research estimates that developers have already launched 17 private non-landed residential projects with a total of 6,773 units. We believe the pent-up demand has been mostly absorbed and genuine buyers are now spoilt for choice. In addition, prices have already moved up significantly and investors could feel that there is limited room for upside. Some of the projects which are targeted at investors or typically have higher foreigner buyers will face some resistance given the recent cooling measures doubling foreigners’ ABSD to 60% as well as a further increase in ABSD rate for investors. These investors will reassess their options and take a longer time to shop around.

We are of the view that the souring macro backdrop, elevated interest rate hikes and cooling measures have slowed demand, though this has become more prominent with the abundant new launches that have come through over the past two months.

Launches that could be coming in the next few quarters include J’den, The Hill@one north and Newport Residences.

Overall, CBRE Research expects 6,500 – 7,500 new private homes to be sold in 2023, on par with the 7,099 units in 2022, which was a 14-year low since 2008’s 4,264 units.

Correspondingly, in view of the cooling measures effective 27 Apr 2023, CBRE Research believes home prices which have risen 3.1% in H1 2023 have peaked and are likely to flatten out in the next few quarters. Barring widespread retrenchments and a sustained recession, a significant price correction is not expected given low unsold inventory and generally healthy household balance sheets. As such, CBRE Research maintains its full year 2023 forecast for private home price growth of 3%, slower than the 8.6% seen in 2022 due mainly to a weaker economic outlook -- MTI forecasts 0.5 – 1.5% GDP growth for 2023, vs 3.6% for 2022.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.