Singapore

Commentary on Monthly New Home Sales for July 2024

August 15, 2024

Associated Contact

Head of Marketing & Communications, Singapore

Following the school holidays lull in June, private developer sales picked up in the month of July on the back of two new launches. 571 units were sold, more than doubling Jun 2024’s lacklustre showing of 228 units. This is, however, still a decade low for the month of July since Jul 2014’s 511 units and less than half the month’s 5-year historical average of 1,223 units as homebuyers’ tentative stance persisted amid weak economic conditions, high interest rates and resistance to high price points.

New home sales were up 150.4% m-o-m to 571 units in Jul 2024 from 228 units in Jun 2024. On a y-o-y basis, sales dived 59.6% from 1,413 units in Jul 2023. This was largely attributed to the return of new launches following the June school holidays lull. 616 units were launched in the month, more than five-fold June’s 118 units.

July sales take the year-to-date 2024 tally of new homes sold to 2,460 units, 48.7% lower y-o-y from 4,796 units over the corresponding period in 2023. This follows H1 2024 sales of 1,889 units which is a record low for half-year developer sales, below the previous floor of 1,977 units in H2 2008 during the Global Financial Crisis (GFC). Market sentiment remains cautious, with buyers currently very selective and price sensitive amid a gloomy and uncertain economic outlook, coupled with delays in any interest rate cut.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

KASSIA |

FLORA DRIVE |

FH |

OCR |

154 |

$2,049 |

55.8% |

|

SORA |

YUAN CHING ROAD |

99 yrs |

OCR |

103 |

$2,152 |

23.4% |

|

THE LAKEGARDEN RESIDENCES |

YUAN CHING ROAD |

99 yrs |

OCR |

41 |

$2,212 |

57.2% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

29 |

$2,088 |

51.3% |

|

NORTH GAIA EC |

YISHUN CLOSE |

99 yrs |

OCR |

26 |

$1,319 |

86.4% |

|

GRAND DUNMAN |

DUNMAN ROAD |

99 yrs |

RCR |

24 |

$2,583 |

69.1% |

|

TEMBUSU GRAND |

JALAN TEMBUSU |

99 yrs |

RCR |

23 |

$2,445 |

69.0% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

21 |

$2,183 |

51.7% |

|

LENTOR MANSION |

LENTOR GARDENS |

99 yrs |

OCR |

20 |

$2,237 |

85.6% |

|

LENTORIA |

LENTOR HILLS ROAD |

99 yrs |

OCR |

20 |

$2,171 |

40.1% |

|

Project Name |

Street Name |

Tenure |

Locality |

Total # of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

|

SORA |

YUAN CHING ROAD |

99y |

OCR |

440 |

320 |

103 |

2152 |

32% |

|

KASSIA |

FLORA DRIVE |

FH |

OCR |

276 |

276 |

154 |

2049 |

56% |

July 2024 saw two new launches – 99y Sora (440 units) located in Jurong Lake district and freehold Kassia (276 units), the final project in the Flora Drive enclave at Upper Changi Road North. The former sold 103 units (23%) of total units at a median price of $2,152 psf while the latter moved 154 units (56%) at a median price of $2,049 psf.

The top performing private project in the month was new launch Kassia (276 units). Benefiting from its attractive price point and price quantum for a freehold project, it was met with healthy demand, moving 154 units (56%) at a median price of $2,049 psf. Meanwhile, demand at the second top project in the month, new launch Sora (440 units) was more subdued. 103 units (23%) were sold at a median price of $2,152 psf, consistent with the sell-through rate of 20 – 30% for most projects in 2024 thus far amid a soft primary market.

The third best performing project was another Jurong Lake district project, The Lakegarden Residences (306 units) which sold 41 units at a median price of $2,212 psf in July, bringing its cumulative take-up to 175 units or 57%. Located just adjacent to Sora, The Lakegarden Residences which was launched in August 2023 sold 73 units or 35% of its 306 units at a median price of $2,101 psf then, and has seen renewed interest in June and July 2024 on the back of Sora’s launch buzz.

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Aug 2024.

By market segment, Jul 2024’s developer sales (excluding ECs) continued to be led by the Outside Central Region (OCR). Boosted by new launches, 444 units or 77.8% of total July new home sales were sold in the OCR, up from 132 units (57.9%) in June. The Rest of Central Region (RCR) trailed at 106 units (18.6%), up from 71 units (31.1%) in June 2024. Lastly, the Core Central Region (CCR) observed muted sales, moving 21 units (3.7% of July sales), compared to 25 units (11.0%) in June.

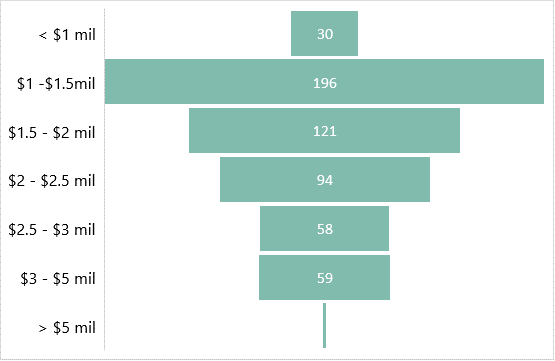

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.00 – 1.50 mil range at 35%, a shift away from the S$1.50 mil – 2.00 mil range majority for most months which could be indicative of increased buyer price sensitivity. This was followed by the S$1.50 mil – S$2.00 mil bracket at 21.6%.

Outlook and forecasts

2023 new home sales hit a 15-year low at 6,421 units, 9.6% below the 7,099 units in 2022 amid repeated rounds of cooling measures, a softening economic backdrop and elevated interest rates. This soft sentiment and market have persisted in 2024, with H1 2024 sales falling to a record low for half-year developer sales, below the previous floor of 1,977 units in H2 2008 during the Global Financial Crisis (GFC) and 44.2% lower y-o-y from H1 2023.

Despite a rebound in sales in July on a return of launches, the gap between 2024’s tally of new home sales of 2,460 units and 2023’s 4,796 units has widened to 48.7% y-o-y. Buyers have turned very cautious and price sensitive, displaying resistance to high price points especially at recent new launches. In turn, the lower take-up rates observed across 2024 project launches appear to be encouraging developers to delay their launches in wait of better and more stable market conditions.

Looking ahead, developer sales are expected to be muted in Aug 2024 amid the Hungry Ghost Festival where developers tend to hold back on launches. Sales in September, however, look set to pick up on anticipated major city-fringe launches including freehold launch Meyer Blue (226 units), Emerald of Katong (847 units) -- the second Jalan Tembusu project, and 8@BT (158 units) located on the Bukit Timah Link GLS site near Beauty World. In the suburbs The Chuan Park (916 units) at Lorong Chuan developed by Kingsford Development & MCC Land could also launch. On the back of a healthy pipeline of launches, Q3 2024 developer sales could overtake the tepid sales recorded in Q2 2024.

Nonetheless, with the expectation of a delay in interest rate cuts amid protracted economic uncertainty, the timeline for a more significant recovery in new developer sales is likely to be pushed to 2025. CBRE Research expects 5,500 – 6,500 new homes to be sold in 2024. Attractive developer pricing remains key to healthy new launch performance.

Correspondingly, private residential prices which are up 2.3% in H1 2024 are expected to stabilise and rise at a slower pace in H2 2024 with the pushback in the timeline for interest rate cuts and anticipated economic recovery. CBRE Research maintains our price growth forecast at 3 – 4% in 2024. A significant correction is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory. HDB resale price index rose 2.3% q-o-q in Q2 2024, accelerating from the 1.8% in Q1 2024. Barring a major economic shock, the healthy public housing market could continue to support the OCR and RCR segments of the private market going forward.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.