Singapore

Commentary on Monthly New Home Sales for June 2024

July 15, 2024

Associated Contact

Head of Marketing & Communications, Singapore

New private developer sales remained in the doldrums in June, sinking to a record low for the month of June, and just slightly higher than May 2024’s lacklustre showing of 223 units. This brings Q2 2024 new home sales to 752 units, the lowest since Q4 2022’s 690 units. Including the 1,164 units in Q1 2024, 1H24 of 1,916 units is the lowest half yearly new home sales on record, even lower than H2 2008’s 1,977 units, during the throes of Global Financial Crisis.

New home sales rose marginally by 2.2% m-o-m to 228 units in Jun 2024 from 223 units in May 2024. On a y-o-y basis, sales were down 18.0% from 278 units in June 2023 which was the previous floor for the month. This is largely attributed to the absence of major new launches amid the June school holiday lull. Developers could also have held back on launches amid near-term interest rate uncertainty and the current tentative buying sentiment. 118 units were launched in the month, half of May’s 228 units and April’s 278 units.

June sales take the current H1 2024 tally of new homes sold to 1,916 units, 43.4% lower y-o-y from 3,383 units over the corresponding period in 2023. Buyers are now more selective amid more choices and high price points, with near-term sentiment further dented by a delay in the timeline of US interest rate cuts.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

NORTH GAIA |

YISHUN CLOSE |

99 yrs |

OCR |

29 |

$1,311 |

82.3% |

|

THE LAKEGARDEN RESIDENCES |

YUAN CHING ROAD |

99 yrs |

OCR |

23 |

$2,119 |

45.8% |

|

THE BOTANY AT DAIRY FARM |

DAIRY FARM WALK |

99 yrs |

OCR |

21 |

$1,979 |

94.6% |

|

TEMBUSU GRAND |

JALAN TEMBUSU |

99 yrs |

RCR |

20 |

$2,542 |

65.4% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

18 |

$2,124 |

42.8% |

|

LUMINA GRAND |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

16 |

$1,508 |

75.6% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

15 |

$2,548 |

44.0% |

|

LENTOR HILLS RESIDENCES |

LENTOR HILLS ROAD |

99 yrs |

OCR |

14 |

$2,104 |

90.5% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

13 |

$2,132 |

47.5% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

FH |

RCR |

11 |

$2,859 |

44.0% |

|

LENTORIA |

LENTOR HILLS ROAD |

99 yrs |

OCR |

11 |

$2,096 |

32.6% |

There were no new launches in June amid the school holiday lull.

Amid the dearth of new launches, all of the top 10 best performing projects in the month came from existing projects mainly from the OCR and RCR, including 2 EC launches. This is indicative that buyers have turned very price sensitive amid economic weakness and high mortgage rates.

The top performing private project in the month was existing launch, The Lakegarden Residences (306 units) which moved another 23 units at a median price of $2,119 psf. This was followed by The Botany at Dairy Farm (386 units) which sold 21 units at a median price of $1,979 psf. Said project is now 95% sold.

The third best performing project was RCR project, Tembusu Grand (638 units) where 20 more units were transacted at a median price of $2,542 psf.

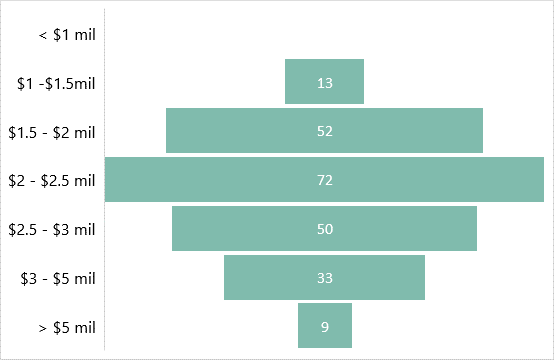

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Jul 2024.

By market segment, Jun 2024’s developer sales (excluding ECs) continued to be led by the Outside Central Region (OCR), selling 132 units or 57.9% of total June new home sales, down from 143 units (64.1%) in May. The Rest of Central Region (RCR) sold 71 units (31.1%), up from 53 units (23.8%) in May 2024. Lastly, the Core Central Region (CCR) observed weaker sales, moving 25 units (11% of June sales), compared to 27 units (12.1%) in May.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$2.00 – 2.50 mil range at 31.4%. This was followed by the S$1.50 mil – S$2.00 mil bracket at 22.7%.

Outlook and forecasts

2023 new home sales hit a 15-year low at 6,421 units, 9.6% below the 7,099 units in 2022 amid repeated rounds of cooling measures, a softening economic backdrop and elevated interest rates.

The weak sentiment has persisted through the first half of 2024, with developer sales sinking to a record low half-yearly new sale, 43.4% lower y-o-y from 3,383 units sold over the correspondingly period in 2023. Buyers have turned more selective amid a myriad of new launch options, buyer fatigue and increasing resistance to high price points, with generally lower take-up rates observed across 2024 project launches. Homebuyers’ current tentative stance is likely to persist until interest rate cuts and an economic rebound catalyse a recovery in sentiment.

Looking ahead, developer sales could pick up in July 2024 on the back of two new suburban launches, Kassia (276 units) situated along Flora Drive and Sora (440 units), the redevelopment of former Parkview Mansions, along Yuan Ching Road in Jurong Lake District. It was reported that Sora moved 102 units, 23.2% of its total units over its launch weekend at an average selling price of $2,160 psf.

Other major launches anticipated in the H2 2024 pipeline include suburban project The Chuan Park (916 units) at Lorong Chuan developed by Kingsford Development & MCC Land, city-fringe launch Emerald of Katong (847 units) (Jalan Tembusu site) and mixed-use project The Collective at One Sophia (367 units) which, if priced attractively, could ride on the positive interest for mixed-use developments which offer residents convenience and access to a host of amenities. Projects at Toa Payoh Lor 1, Clementi Ave 1, and Tampines Avenue 11 sites are also highly anticipated future launches.

Nonetheless, with the expectation of a delay in interest rate cuts amid protracted economic uncertainty, the timeline for a more significant recovery in new developer sales is likely to be pushed to 2025. CBRE Research expects 5,500 – 6,500 new homes to be sold in 2024. H2 2024 sales could see a pickup in sales with more major launches anticipated in the pipeline and bring overall sales for the year close to 2023’s 6,421 units. Attractive developer pricing remains key to healthy new launch performance.

Correspondingly, private residential prices which are up 2.5% in H1 2024 based on Q2 2024’s flash estimate is expected to stabilise and rise at a slower pace in H2 2024 with the pushback in the timeline for interest rate cuts and anticipated economic recovery. CBRE Research forecasts prices to rise 3 – 4% in 2024. A significant correction is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory. HDB resale price index rose 2.1% q-o-q in Q2 2024, accelerating from the 1.8% in Q1 2024. Barring a major economic shock, the public housing market could continue to support the OCR and RCR segments of the private market going forward.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.