Singapore

Commentary on Monthly New Home Sales for June 2025

July 15, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Developer sales in Jun 2025 sank for the fourth straight month to the lowest level in 2025-to-date on the absence of major new launches amid the June school holidays lull. 272 new private homes were sold in the month, down 12.8% m-o-m from 312 units in May 2025. On a y-o-y basis, however, sales were up 19.3% from the 228 units sold in Jun 2024.

June’s sales take the tally of new homes sold in Q2 2025 to 1,259 units, down 63% q-o-q, but up 74% y-o-y.

This four-month sequential decline reflects cautious buyer sentiment, weighed down by persistent trade frictions and geopolitical tensions that have clouded Singapore’s economic outlook. However, with a bumper new launch pipeline and some pent-up demand, sales would likely pick up in July and August.

Top 10 Selling Projects in June 2025 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

49 |

$2,962 |

51.2% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

30 |

$2,516 |

44.4% |

|

THE HILL @ONE-NORTH |

SLIM BARRACKS RISE |

99 yrs |

RCR |

17 |

$2,490 |

77.5% |

|

AMBER HOUSE |

AMBER GARDENS |

Freehold |

RCR |

17 |

$2,977 |

16.2% |

|

AURELLE OF TAMPINES (EC) |

TAMPINES STREET 62 |

99 yrs |

OCR |

15 |

$1,813 |

98.8% |

|

GRAND DUNMAN |

DUNMAN ROAD |

99 yrs |

RCR |

12 |

$2,534 |

78.9% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

12 |

$2,311 |

92.6% |

|

NAVA GROVE |

PINE GROVE |

99 yrs |

RCR |

12 |

$2,569 |

81.3% |

|

ARINA EAST RESIDENCES |

TANJONG RHU ROAD |

Freehold |

RCR |

9 |

$2,982 |

8.4% |

|

NOVO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

9 |

$1,592 |

99.6% |

There were two relatively small new launches in Jun 2025, both in the East Coast in RCR and of freehold tenure – Arina East Residences (107 units), redevelopment of the former La Ville located in Tanjong Rhu and Amber House (105 units), the redevelopment of the former Amber Glades which was acquired by Far East Organisation through a collective sale back in Mar 2011.

Both projects were met with a relatively muted response – Arina East Residences (107 units) sold 9 units (8% of total units) at a median price of $2,982 psf and Amber House (105 units) moved 17 units (16% of total units) at a median price of $2,977 psf.

The top performing projects in June were existing launches. The top performing launch for a third consecutive month was One Marina Gardens (937 units) developed by Kingsford Group located in the Marina South precinct at the fringe of the CBD. Recently launched in Apr 2025, the project moved another 49 units at a median price of $2,962 psf, after 62 units at median price of $2,975 psf in May, and is now 51% sold.

The second best-selling private project was new launch Bloomsbury Residences (358 units) at Media Circle in the one-north precinct which was also launched in Apr 2025. The project sold another 30 units in Jun 2025 at a median price of $2,516 psf. This was followed by another one-north project The Hill @One-North (142 units) which was launched in Apr 2024. The project sold another 17 units at a median price of $2,490 psf.

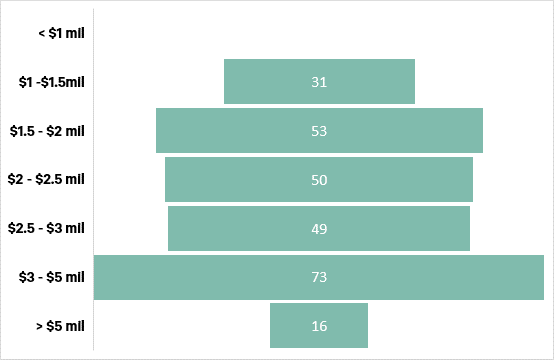

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Jul 2025.

By market segment, Jun 2025’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR) which recorded the sale of 189 units (69.5%) from 191 units (61.2%) of total new sales in May 2025. This was largely attributed to One Marina Gardens and Bloomsbury Residences.

Lastly, the Core Central Region (CCR) continued to underperform, moving 14 units (5.1% of June sales), down marginally from 15 units (4.8%) in May 2025.

Based on quantum size, the new sales transactions appear to be quite evenly distributed across different budgets in June. The largest proportion of new private homes sold (excl. ECs) was actually in the S$3.00 – 5.00 mil range at 26.8% from larger units at existing city fringe and suburban launches, followed by the S$1.50 mil – S$2.00 mil bracket at 19.5% which is the sweet spot for 2-bedders at Bloomsbury Residences and One Marina Gardens. The $2.00 – 2.50 mil and $2.50 – 3.00 mil range trailed closely behind at 18.4% and 18% respectively.

Notably, 16 units above $5 mil were recorded in the month, of which 7 were from mixed-use RCR project Canninghill Piers (696 units) at a median price of $2,711 psf. The project is the residential component of the redevelopment of Liang Court and was launched in Nov 2021, and sold 576 units of 83% of 696 total units in Nov 2021 at a median price of $2,887psf.

Outlook and Forecasts

The lack of launches and weak sales in May and June reflect the cautious sentiment among developers and homebuyers on the back of ongoing global trade frictions which have dampened Singapore’s economic outlook.

On 3 Jul 2025, the government announced a new round of cooling measures. Seller’s Stamp Duty was raised by 4 ppts and the holding period to 4 years with effect from 4 Jul 2025. This is expected to have a limited impact on transaction volumes and pricing as it should not impact the majority of buyers who are genuine owner occupiers or long-term investors.

A slew of projects is expected to launch in July and August prior to the start of the Hungry Ghost Festival in the last week of August. As such, sales are expected to see an uptick in the months ahead.

It was reported that LyndenWoods (343 units), the first project launch following the new cooling measures from 4 July observed robust take-up, moving 324 units (94% of total units) at an average price of $2,450 psf. On the other hand, luxury W Residences Marina View (683 units), in prime CBD Marina View, and launched over the same July 12 weekend with listing prices of $3,800-6,000 psf, was reported to have sold just one unit at $4,085psf. This could be an indication that buyers are price-sensitive, but there is still ample interest for well-priced projects with attractive attributes given lower interest rates and resilient economic growth.

The performance of upcoming launches is expected to be mixed with over half of the launches in pretty prime locations in the CCR and RCR. CBRE Research maintains our full year new home sales to be 7,000 – 8,000 units, signaling a slowdown in new home sales compared to the 1H25, but we note sales performance could surprise on the upside if developers priced and designed them sensitively.

Correspondingly, private home prices which have risen 1.3% in H1 2025 based on Q2 2025’s flash estimate could see similar growth momentum in H2 2025. We maintain a full-year 2025 private home price increase of 3 – 4% for now, on still-low unsold inventory and strong household balance sheets.

Advance estimates released by the MTI yesterday (14 Jul) showed that Singapore’s economy grew by 4.3% y-o-y in Q2 2025, accelerating from the 4.1% growth in Q1 2025. The better-than-expected GDP performance in Q2 is largely due to the front-loading of exports and manufacturing before the 90-day pause in US tariffs ends. Looking forward, there remain significant uncertainty and downside risks in the global economy in the second half of 2025, given the lack of clarity over the tariff policies of the US.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.