Singapore

Commentary on Monthly New Home Sales for March 2024

April 15, 2024

Associated Contact

Head of Marketing & Communications, Singapore

New private developer sales saw a strong month-on-month rebound in March on the back of an increase in launches following the Chinese New Year seasonal lull. Despite no new launches in the CCR, some ongoing CCR projects have seen renewed interest in March. Nonetheless, overall sentiment remains relatively muted on economic uncertainties and negative newsflows.

New home sales more than quadrupled m-o-m to 718 units in Mar 2024 from 153 units in Feb 2024. On a y-o-y basis, developer sales were also up 46% y-o-y from 492 units in Mar 2023. This is largely attributed to a pickup in new launches following the Chinese New Year seasonal lull.

March sales take Q1 2024 new home sales to 1,175 units, a 7.6% q-o-q increase from 1,092 units in Q4 2023 but 6.4% lower y-o-y from 1,256 units sold over the correspondingly period in 2023. Take-up has largely moderated and buying sentiment has turned cautious amid high interest rates and an uncertain economy. Buyers are now more selective amid more choices and high price points. Selected projects with superior attributes at realistic price points outperformed while overall sales remained tepid.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

LENTOR MANSION |

LENTOR GARDENS |

99 yrs |

OCR |

409 |

$2,269 |

76.7% |

|

LUMINA GRAND |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

86 |

$1,528 |

72.3% |

|

LENTORIA |

LENTOR HILLS ROAD |

99 yrs |

OCR |

60 |

$2,129 |

22.5% |

|

THE BOTANY AT DAIRY FARM |

DAIRY FARM WALK |

99 yrs |

OCR |

33 |

$2,030 |

73.8% |

|

LENTOR HILLS RESIDENCES |

LENTOR HILLS ROAD |

99 yrs |

OCR |

29 |

$2,114 |

81.6% |

|

NORTH GAIA |

YISHUN CLOSE |

99 yrs |

OCR |

23 |

$1,341 |

70.5% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

16 |

$2,074 |

23.2% |

|

THE MYST |

UPPER BUKIT TIMAH ROAD |

99 yrs |

OCR |

13 |

$1,996 |

54.7% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

12 |

$2,168 |

38.4% |

|

WATTEN HOUSE |

SHELFORD ROAD |

FH |

CCR |

12 |

$3,255 |

74.4% |

Mar 2024 saw four new non-landed launches: two boutique projects in the city-fringe: Ardor Residence (35 units) and Koon Seng House (17 units); and two more major suburban launches: Lentor Mansion (533 units) and Lentoria (267 units).

The top 2 best performing private projects were from the two Lentor new launches, led by Lentor Mansion (533 units) which was met with robust demand, moving 409 of its total units (77%) at a median price of $2,269 psf, making it the best-performing new launch in 2024 so far. Lentor Mansion is jointly developed by GuocoLand and Hong Leong Holdings and is the first development sold using new guidelines from the URA on the harmonisation of strata and gross floor area which would skew per square foot prices upwards by 5 – 10%. The project was, however, still well-received likely due to its keeping its layouts efficient and price quantum comparable with or even slightly lower than earlier projects, its location within a 1km radius from CHIJ St Nicholas Girls’ School, and ample facilities.

In second place was new launch Lentoria (267 units) jointly developed by Hong Leong Group and Mitsui Fudosan which sold 60 units or 17% of total units at a median price of $2,129 psf.

Following behind in third place was existing launch The Botany at Dairy Farm (386 units) which transacted another 33 units at a median price of $2,030 psf.

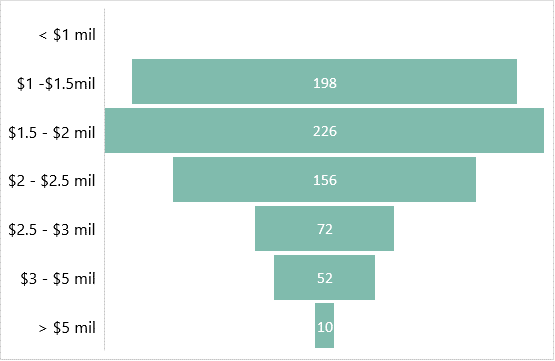

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Apr 2024.

By market segment, Mar 2024’s developer sales (excluding ECs) were led by the Outside Central Region (OCR) due to the success of Lentor projects, selling 605 units or 84.3% of total March new home sales, up from 58 units (37.9%) in February. The Rest of Central Region (RCR) saw 66 sales (9.2%), up from 61 units (39.9%) in February 2024. Despite no new launches in March, Core Central Region (CCR) also saw better sales, selling 47 units (6.5% of March sales), compared to 34 units (22.2%) in February. The better performance of CCR launches came on the back of Cuscaden Reserve cutting prices by about 20% which may have triggered more buyer interest and bargain hunting in the CCR. 19 Nassim sold 11 units in March, its highest monthly sales, at a median price of S$3,304 psf. 19 Nassim has since sold 31 out of total 101 units. Klimt at Cairnhill sold 8 units, highest since Oct 2023, at a median price of S$3,497 psf. We note that Leedon Green and Pullman Residences sold their last units in March, at S$3,135 and S$3,435 psf respectively.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 mil - S$2.00 mil range at 31.7%. This was followed by the S$1.00 mil – S$1.50 mil bracket at 27.7%.

Outlook and forecasts

2023 new home sales hit a 15-year low at 6,421 units, 9.6% below the 7,099 units in 2022 amid repeated rounds of cooling measures, a softening economic backdrop and elevated interest rates. Buyers have turned more selective amid a myriad of new launch options, buyer fatigue and increasing resistance to high price points.

Homebuyers’ tentative stance appears to have persisted in Q1 2024, with the tally of new home sales at 1,175 units, 6.4% lower y-o-y from 1,256 units sold in Q1 2023 despite more new launches (Q1 2024 saw 6 new launches vs 4 in Q1 2023). Negative newsflows from a slew of company layoffs, albeit globally could have further dented buying sentiment to start the year.

Looking ahead, 2 new city-fringe project launches are expected in Apr 2024. The former of which is freehold project The Hillshore (59 units) situated along Pasir Panjang Road which would be the maiden condo undertaken by local developer FRX Capital. The latter, The Hill @ One-North (142 units) sits on the Slim Barracks Rise (Parcel B) GLS site awarded in Oct 2021 to Kingsford Development could see healthy demand, following the success observed at the adjacent site launched at the end of Apr 2023 as Blossoms by the Park (275 units) which achieved 73% take up at an average price of $2,423 psf on the first day of sales.

Overall, CBRE Research is cautiously optimistic on the private residential market in 2024. We expect forecast 7,000 – 8,000 new homes could be sold in 2024, an improvement from the 6,421 units in 2023 but still below the 5-year average new developer sales across 2019 – 2023 of 9,288 units. In the near term, downbeat macroeconomic conditions, cooling measures and elevated interest rates are likely to continue weighing on the private residential market but sentiment could improve in H2 2024 if interest rates ease and the economy recovers.

Correspondingly, private residential prices which are now up 1.5% based on Q1 2024’s flash estimate could rise at a slower pace in Q2 2024 before picking up again in H2 2024 if interest rates fall and the economy recovers. CBRE Research maintains our price forecast at 3 – 4% in 2024. A significant correction is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.