Singapore

Commentary on Monthly New Home Sales for March 2025

April 15, 2025

Associated Contact

Head of Marketing & Communications, Singapore

Developer sales in March 2025 eased from February’s robust performance on fewer launches. 555 new units were launched in the month, less than one-third of the 1,694 units in February. Correspondingly, private new home sales fell 54.4% m-o-m to 729 units in the month from 1,597 units recorded in Feb 2025 but were up 1.5% y-o-y from the 718 units sold in Feb 2024.

March’s sales take the tally of new homes sold in Q1 2025 to 3,409 units, holding firm from the high base of 3,420 units sold in Q4 2024. Buying sentiment and appetite has improved amid lower mortgage rates and as developers push ahead with major launches.

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

AURELLE OF TAMPINES (EC) |

TAMPINES STREET 62 |

99 yrs |

OCR |

705 |

$1,769 |

92.8% |

|

LENTOR CENTRAL RESIDENCES |

LENTOR CENTRAL |

99 yrs |

OCR |

460 |

$2,213 |

96.4% |

|

NOVO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

30 |

$1,661 |

93.7% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

27 |

$2,581 |

81.7% |

|

LUMINA GRAND (EC) |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

24 |

$1,513 |

93.6% |

|

AUREA |

BEACH ROAD/NICOLL HIGHWAY |

99 yrs |

CCR |

24 |

$2,924 |

12.8% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

21 |

$2,181 |

87.8% |

|

NORTH GAIA (EC) |

YISHUN CLOSE |

99 yrs |

OCR |

20 |

$1,407 |

99.8% |

|

PARKTOWN RESIDENCE |

TAMPINES STREET 62 |

99 yrs |

OCR |

20 |

$2,444 |

88.7% |

|

SORA |

YUAN CHING ROAD |

99 yrs |

OCR |

19 |

$2,320 |

42.0% |

|

Project Name |

Street Name |

Tenure |

Locality |

Total no. of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

Units sold as % of total |

|

AUREA |

BEACH ROAD/NICOLL HIGHWAY |

99 yrs |

CCR |

188 |

78 |

24 |

2924 |

31% |

13% |

|

LENTOR CENTRAL RESIDENCES |

LENTOR CENTRAL |

99 yrs |

OCR |

477 |

477 |

460 |

2213 |

96% |

96% |

March 2025 saw 2 new private launches – the residential component of Golden Mile Complex redevelopment, Aurea (188 units) in Beach Road and mass-market project Lentor Central Residences (477 units) which is the sixth Lentor project to be launched over the past 3 years.

Despite concerns of oversupply in the Lentor area which now has 6 newly launched projects since 2022 and another upcoming site at Lentor Gardens GLS, Lentor Central Residences (477 units) clinched the spot as the top performing private project in the month, moving 460 units or 96% of its 477 total units at a median price of $2,213 psf. The key draw for the launch was its attractive price point comparable with Lentor projects launched 2 years ago.

The second best-selling private project was existing launch Pinetree Hill (520 units) which sold another 27 units at a median price of $2,581 psf in March, followed by new launch Aura (188 units) which saw more subdued take-up, selling 24 units or 13% of its 188 total units, likely due to its higher price point with a median price of $2,924 psf.

We do note however that the top selling launch (incl. ECs) was EC project Aurelle of Tampines (760 units) which saw robust take-up, moving 705 units or 93% of its total units at a median price of $1,769 psf, a new benchmark price for ECs. The project may have benefitted from its attractive location near transport hubs (the future Tampines North MRT station on the Thomson-East Coast Line and a bus interchange) and a host of amenities at the upcoming retail mall located next to integrated development Parktown Residence (1,193 units) located just across from Aurelle. The strong performance at Aurelle of Tampines also led to spillover demand at existing EC launches, with EC projects forming 4 of the top 10 launches.

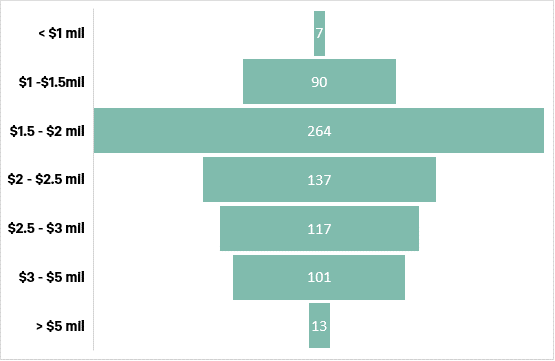

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Apr 2025.

By market segment, March 2025’s developer sales (excluding ECs) were led by the Outside Central Region (OCR). 596 units or 81.8% of total March new home sales came from the OCR due to strong sales at Lentor Central Residences, albeit down from 1,469 units (92.0%) in Feb 2025 which saw more launches. 87 units or 11.9% of total March new home sales were from the Rest of Central Region (RCR), down from 100 units (6.3%) in Feb 2025. Lastly, the Core Central Region (CCR) moved 46 units (6.3% of March sales), up from 28 units (1.8%) in Feb 2025 on the new launch of Aurea.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 – 2.00 mil range at 36.2% which is the sweet spot for buyers of 2-bedder units at new launches. This was followed by the S$2.00 mil – S$2.50 mil bracket at 18.8%.

Outlook and forecasts

March’s sales take the tally of new homes sold in Q1 2025 to 3,409 units, holding firm (down marginally by 0.3% q-o-q) from the high base of 3,420 units sold in Q4 2024 and up 192.8% y-o-y from the 1,164 units sold in Q1 2024.Looking ahead, sales in April could be flat from March's levels on 2 major launches in the CCR and RCR. Media articles reported that new launch One Marina Gardens in the CBD moved 353 units or 38% of its 937 units at an average price of $2,953 psf over its launch weekend. Meanwhile, city fringe launch, Bloomsbury Residences at Media Circle near the one-north precinct sold 90 units or 25% of its 358 total units at an average price of $2,474 psf.

CBRE Research is cautiously optimistic on the private residential market in 2025. While Q1 2025’s new sales have held up mainly on attractive OCR and RCR projects, most new launches for the rest of 2025 will be from the CCR, which have higher price points and may not generate the same kind of volumes. With most pent-up demand in the suburbs and city fringe realised, pricing and design will be crucial for the upcoming new launches to continue this momentum. We thus maintain our full year new home sales to be 7,000 – 8,000 units, signalling a slowdown in new home sales in the next few quarters, but nonetheless still an improvement from 2024’s 6,469 units on easing interest rates and good pipeline of launches.

Correspondingly, private residential prices rose 3.9% in 2024, a moderation from 2023’s 6.8% growth. Flash estimates show that private home prices rose 0.6% q-o-q in Q1 2025, moderating from the 2.3% q-o-q increase in Q4 2024. Growth momentum could plateau in the next few quarters on a weaker economic outlook – MTI has cut Singapore’s 2025 GDP growth forecast to 0 – 2% (from an initial 1 – 3%) as of 14 April. We maintain a full-year 2025 private home price increase of 3 – 4% for now but recognise there could be risk to the downside.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.