Singapore

CBRE Commentary on Monthly New Home Sales for September 2023

October 16, 2023

Associated Contact

Head of Marketing & Communications, Singapore

New private home sales dwindled for a second straight month, falling 44.9% m-o-m from 394 units in Aug 2023 to 217 units in Sep 2023, on the absence of major new launches, as well as softening demand and the lunar seventh month seasonal lull which extended into mid-September. This is the lowest monthly private home sales this year, and lowest since Dec 2022’s 170 units.

On a y-o-y basis, new home sales were also down 78.0% y-o-y from 987 units in Sep 2022. Sentiment this year has clearly deteriorated with higher interest rates, softer economic prospects and two more rounds of cooling measures since.

With no major new launch in Sep, most sales were from previously-launched projects. This brings cumulative nine-month new home sales in 2023 to 5,407 units, -15.6% y-o-y from the 6,409 units sold over the first nine months in 2022.

New launches in Sep 2023

Source: CBRE Research, URA

Sep 2023 saw 1 small new apartment launch in the OCR, The Shorefront (23 units) which sold 3 units or 13% of total units at a median price of $1,902 psf.

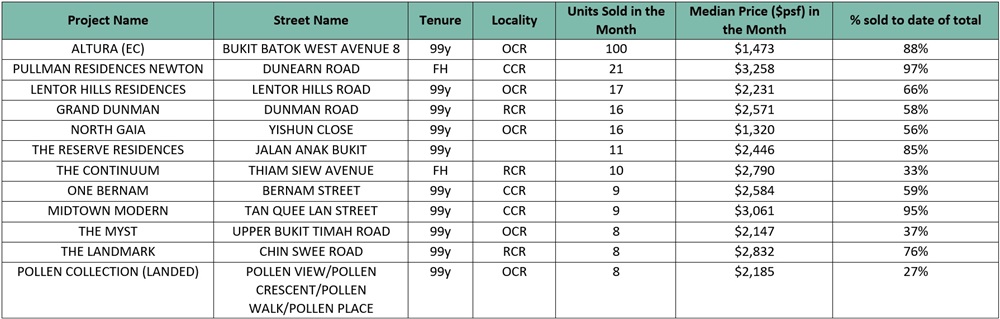

Top 10 Selling Projects in Sep 2023 (including ECs and landed)

(Top 12 due to 3 projects selling the same number during the month)

Source: CBRE Research, URA

The top performing project in the month was Altura EC launched in August which sold another 100 units at a median price of S$1,473 psf. A distant second was Pullman Residences Newton which sold 21 units at a median price of S$3,258 psf. The third best-selling project was Lentor Hills Residences, launched in July, which sold another 17 units in September to bring cumulative sales to 66%.

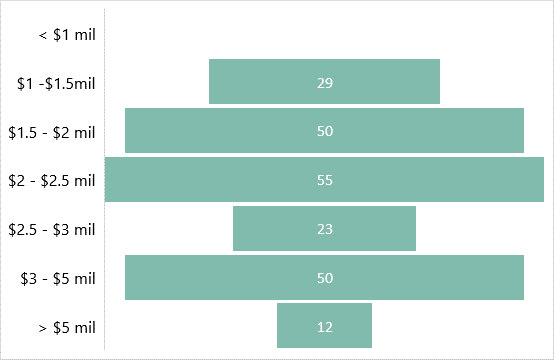

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 16 Oct 2023.

By market segment, Sep 2023’s developer sales (excluding ECs) were evenly split, led marginally by the Core Central Region (CCR) where 76 units (35.0%) were sold, followed by the Rest of Central Region (RCR) where 71 units (32.7%) were sold and the Outside Central Region (OCR) which saw the sale of 70 units (32.3%). This compares to 24.4% in the CCR, 26.9% in the RCR and 48.7% in the OCR in Aug 2023.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$2.00 mil - S$2.50 mil range at 25.1%. This was followed by the S$1.50 mil – S$2.00 mil bracket at 22.8%.

Outlook

Year-to-Sep 2023 new home sales currently stand at 5,407 units, a 15.6% y-o-y fall from 6,409 units sold over the correspondingly period in 2022. CBRE Research is of the view that the souring macro backdrop, elevated interest rate hikes and cooling measures have resulted in increased buyer selectiveness and slower demand. This is evidenced by the slower take-up rate in the abundant new launches that have come through over July to August 2023.

Slowdown in new launch take-up

In 2022, developers launched 15 new private residential projects with 4,528 units (excluding ECs) for sale. While this year to date, CBRE Research estimates that developers have already launched 19 private non-landed residential projects with a total of 6,815 units. We believe the pent-up demand has been mostly absorbed and genuine buyers are now spoilt for choice. Some of the projects which are targeted at investors or typically have higher foreigner buyers will face some resistance given the recent cooling measures doubling foreigners’ ABSD to 60% as well as a further increase in ABSD rate for investors. These investors will reassess their options and take a longer time to shop around.

Forecasts

Major launches that could be coming in Q4 2023 are concentrated in the OCR, with projects such as Lentoria (265 units), J’den (368 units), Hillock Green (474 units), Hillhaven (341 units) and Sora at Yuan Chin Road (440 units). The RCR could also see some launches – The Hill@one north (142 units) and Sky Botania (172 units) and the CCR could see the launch of Newport Residences (246 units). Amid weaker sentiment, still-high interest rates and the upcoming December holiday season, developers might choose to push launches into 2024 when interest rates stabilise and sentiment improves. As such, developer sales are expected to remain subdued in Q4 2023.

Overall, CBRE Research expects 6,500 – 7,000 new private homes to be sold in 2023, potentially below the 7,099 units in 2022, which was already a 14-year low since 2008’s 4,264 units.

Correspondingly, CBRE Research believes home prices which have risen 3.6% cumulatively accounting for Q3 2023’s flash estimate have peaked and are likely to be muted in Q4 2023. Barring widespread retrenchments and a sustained recession, a significant price correction is not expected given low unsold inventory and generally healthy household balance sheets. As such, CBRE Research maintains its full year 2023 forecast for private home price growth of 3%, slower than the 8.6% seen in 2022 due mainly to a weaker economic outlook -- MTI forecasts 0.5 – 1.5% GDP growth for 2023, vs 3.6% for 2022.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.