Singapore

Commentary on Monthly New Home Sales for September 2024

October 15, 2024

Associated Contact

Head of Marketing & Communications, Singapore

Following the dearth of launches in August amid the lunar seventh month, private new home sales rebounded in September, rising 90% m-o-m and 84.8% y-o-y to 401 units. This came on the back of an attractive new launch – 8@BT.

September’s sales take the tally of new homes sold in Q3 2024 to 1,188 units, a 63.9% q-o-q pickup from the low base of 725 units in Q2 2024 but down 39% y-o-y from 1,946 units in Q3 2023. The cumulative tally of new homes sold from 9M 2024 is now 3,077 units, 42.3% lower y-o-y from 5,329 units over the corresponding period in 2023.

This follows H1 2024 sales of 1,889 units which is a record low for half-year developer sales, below the previous floor of 1,977 units in H2 2008 during the Global Financial Crisis (GFC). 2024 is shaping up to be the weakest since 2008’s 4,264 new private home sales in terms of annual new sales, with market sentiment cautious since late 2023. Nevertheless, home sales are poised to improve in Q4 2024, amid pent-up demand, more attractive launches waiting in the wings, lower interest rates and a more optimistic economic outlook – Q3 2024’s GDP flash estimate announced yesterday (14 Oct) recorded 4.1% y-o-y growth, its highest pace since 2022.

Top 10 Selling Projects in September 2024 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

8@BT |

BUKIT TIMAH LINK |

99 yrs |

RCR |

83 |

$2,727 |

52.5% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

72 |

$2,501 |

61.0% |

|

HILLHAVEN |

HILLVIEW RISE |

99 yrs |

OCR |

46 |

$2,120 |

68.3% |

|

TEMBUSU GRAND |

JALAN TEMBUSU |

99 yrs |

RCR |

32 |

$2,431 |

78.7% |

|

HILLOCK GREEN |

LENTOR CENTRAL |

99 yrs |

OCR |

22 |

$2,224 |

60.1% |

|

LENTORIA |

LENTOR HILLS ROAD |

99 yrs |

OCR |

19 |

$2,163 |

52.4% |

|

THE MYST |

UPPER BUKIT TIMAH ROAD |

99 yrs |

OCR |

16 |

$2,082 |

67.6% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

FH |

RCR |

11 |

$2,843 |

48.3% |

|

LUMINA GRAND (EC) |

BUKIT BATOK WEST AVENUE 5 |

99 yrs |

OCR |

11 |

$1,486 |

81.3% |

|

POLLEN COLLECTION (LANDED) |

POLLEN VIEW/POLLEN CRESCENT/POLLEN WALK/POLLEN PLACE |

99 yrs |

OCR |

10 |

$2,272 |

68.2% |

|

SCENECA RESIDENCE |

TANAH MERAH KECHIL LINK |

99 yrs |

OCR |

10 |

$2,074 |

81.7% |

New launches in September 2024

|

Project Name |

Street Name |

Tenure |

Locality |

Total # of units |

Units Launched in the Month |

Units Sold in the Month |

Median Price ($psf) in the Month |

Units sold as % of launched |

|

8@BT |

BUKIT TIMAH LINK |

99y |

RCR |

158 |

158 |

83 |

$2,727 |

53% |

September 2024 saw the sole launch of 99y 8@BT (158 units) located at Bukit Timah Link, just beside the Beauty World MRT station, developed by Bukit Sembawang Estates. Benefitting from its attractive location close to the MRT and an upcoming integrated transport hub at Jalan Anak Bukit, the project observed a stable take-up rate of 53%, moving 83 of its 158 total units at a benchmark median price of around $2,727 psf. The performance of said launch appears to have had spillover effects on other comparatively cheaper projects in the RCR, with 3 of the top 5 projects in the month coming from the segment.

The second top project in the month was Pinetree Hill (520 units) at Pine Grove which sold 72 more units at a median price of $2,501 psf. This is followed by suburban project Hillhaven (341 units) located at Hillview Rise, which moved another 46 units at a median price of $2,120 psf.

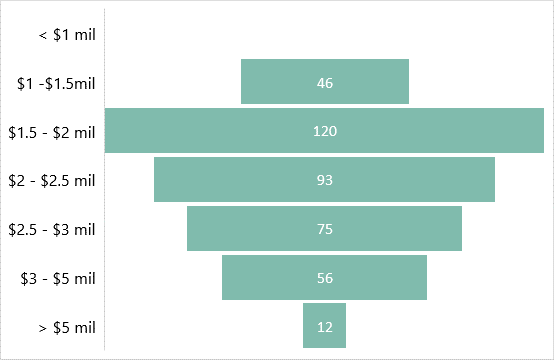

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 Oct 2024.

By market segment, September 2024’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR), due to the sole new launch in RCR. 221 units, or 55.1% of September’s total new home sales, were sold in the RCR, up from 66 units (31.3%) in August. The Outside Central Region (OCR) sold 165 units (41.1% of September sales), up from 125 units (59.2%) in August 2024. Lastly, the Core Central Region (CCR) observed muted sales, moving 15 units (3.7% of September sales), compared to 20 units (9.5%) in August.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) were in the S$1.50 – 2.00 mil range at 29.9%. This was followed by the S$2.00 mil – S$2.50 mil bracket at 23.1%.

Outlook and forecasts

2024 is shaping up to potentially register the worst annual new sales since 2008. Secondary sales volumes, however, continue to hold up, an indication that there is still liquidity in the market, but price-conscious buyers have turned to secondary stock amid the wide price gap between primary and secondary stock.

We believe some pent-up demand for new homes is building up, and with more attractive launches announced in the months ahead and a more optimistic economic outlook, sales are poised to rebound in Q4 2023. There are indications of a recovery in sentiment following September’s rate cut, with recently launched freehold project in popular East Coast, Meyer Blue (226 units) observing a healthy performance, moving 114 of its total 226 units (50%) over its 5 October launch weekend at an average price of $3,260 psf. Another launch, Norwood Grand at Champions Way, marked to be the first private home launch in Woodlands in 12 years, could also see good sales over the 19 Oct weekend.

Other major potential launches in Q4 2024 include Emerald of Katong (846 units), Nava Grove at Pine Grove (552 units) in the RCR; The Chuan Park (916 units) at Lorong Chuan and Novo Place (EC) in Tengah in the OCR. Attractive developer pricing remains key to healthy new launch performance.

CBRE Research now expects 5,000 – 5,500 new homes to be sold in 2024, compared to 6,421 units in 2023. A more significant recovery of new developer sales is likely in 2025.

Private residential prices, which unexpectedly registered a 1.1% decline in Q3 2024’s flash estimate, should remain resilient in Q4 2024. CBRE Research keeps our full year forecast at +3% in 2024. A correction is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.