Singapore

CBRE Commentary on URA Q3 2023 Statistics

October 27, 2023

Associated Contact

Head of Marketing & Communications, Singapore

Office

• Office rents continued to grow on the back of limited supply and increasing back-to-office momentum. Based on URA statistics, office rents in the Central Region increased for the eighth consecutive quarter since Q3 2021.

• The URA office rental index increased by 4.9% q-o-q in Q3 2023, an acceleration from the increase of 2.3% q-o-q registered in the previous quarter. This increase was mainly propped up by the Central Area, where rents increased by 5.2% q-o-q.

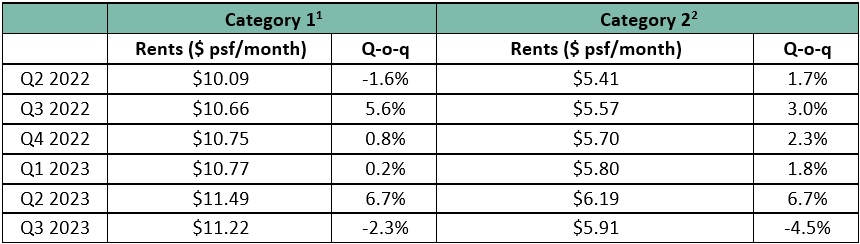

• Median rental (by contract date) in Category 1 (a proxy for prime CBD) office space declined slightly by 2.3% q-o-q. The slight decline in median rents could be due to the sharp rental acceleration of 6.7% q-o-q in Q2 2023. Though this could allude to a slowdown in the pace of rental growth, CBRE Research notes that vacancies for overall prime offices remains low, leading to the resilience in rental performance for the overall prime office market that we have seen thus far.

• On the contrary, median rental (by contract date) in Category 2 (a proxy for CBD Grade B) office space registered a larger decline of 4.5% q-o-q. This could be driven by flight to quality relocations, and it was the first decline after seven consecutive quarters of growth.

• According to URA data, leasing activity is positive islandwide, as seen in the positive net absorption of 0.25 mil sq. ft., following the +0.32 mil sq. ft. in Q2 2023. Tighter market conditions arising from project redevelopments and hence stock removals have also helped to prop up occupancies from 89.2% in Q2 2023 to 90.0% in Q3 2023. According to URA data, about 0.45 mil sq. ft. was removed from stock this quarter, which could have been attributed to redevelopment projects such as Faber House, Central Square and Central Mall.

• Similarly, CBRE Research observed that gross effective prime rents for Core CBD have picked up from modest levels of leasing activity. More diversified demand drivers have made up for the slack resulting from the slowdown in the tech sectors, with private wealth, asset management and consumer goods being the active sectors. Despite concerns surrounding WeWork, other flex space operators appear undeterred, and continued to expand their presence within the CBD. Shadow space was also seen tapering off this quarter, with the amount of shadow space in Q3 2023 halved to 0.33 mil sq. ft., from the record high of 0.70 mil sq. ft. in Q1 2023.

Table 1: Median rentals based on contract date

1 Refers to office space in buildings located in core business areas in Downtown Core and Orchard Planning Area which are relatively modern or recently refurbished, command relatively high rentals and have large floor plate size and gross floor area.

2 Refers to the remaining office space in Singapore which are not included in “Category 1”

Source: URA

Outlook

• According to data tracked by CBRE Research, year-to-date, Core CBD (Grade A) rents have increased by 1.3% in 2023, largely supported by tight vacancies.

• Near-term risks include a cautious economic outlook, high interest rates, and an increasing cost environment which have moderated rental growth to date. That said, the office rental market has outperformed expectations due to limited supply, increasing back-to-office momentum and steady absorption of shadow space. Furthermore, the delayed completion of IOI Central Boulevard Towers to Q1 2024 should keep market vacancy low for the rest of 2023.

• CBRE Research expects Core CBD (Grade A) rents to eventually grow by 1.5% - 2.0% for the full year, outpacing projected GDP growth, but slower than the 8.3% rental growth in 2022.

Retail

• Retail indicators such as the retail sales index continued to grow y-o-y in Q3 2023 despite global macroeconomic weakness. Retail sales remained supported by tourism spending, which was boosted by the F1 race, and consumers’ discretionary purchases. As a result, URA’s Q3 2023 data showed that rents of retail space in the Central Region rose by 0.5% q-o-q, extending the increase of 0.3% q-o-q the previous quarter. Similarly, CBRE Research notes that rents for prime retail spaces islandwide rose at a faster clip in Q3 2023, rising by 1.4% q-o-q, compared to 0.8% q-o-q in Q2 2023.

• However, the rise in rents, coupled with ongoing challenges such as manpower shortages and inflation could have resulted in retailers consolidating their spaces in Q3 2023. According to URA data, the islandwide private retail market saw negative net absorption of 8,000 sq. m. (about 86,000 sq. ft.), compared to the higher take-up of space in Q2 2023 which saw positive net absorption of 25,000 sq. m. (about 269,000 sq. ft.). Despite this, islandwide private retail vacancy rates fell from 8.3% in Q2 2023 to 8.0% in Q3 2023, due to a decline in stock of 22,000 sq. m. (about 237,000 sq. ft.). This is likely to be attributed to the impending redevelopment of projects such as JCube, Central Mall, Central Square and Faber House.

• The lower take-up of space in Q3 2023 was contributed mainly by the suburban market, which saw negative net absorption of 16,000 sq. m. (about 172,000 sq. ft.), leading to a rise in vacancy rates from 4.1% in Q2 2023 to 4.9% in Q3 2023. Demand for suburban retail appears to have stabilized with the return to office and as some retailers consolidate after a strong rental and manpower cost run-up.

• On the other hand, the Downtown Core submarket saw a positive net absorption of 11,000 sq. m. (about 118,000 sq. ft.) in Q3 2023. This could have been boosted by the completion of phase 1 of Guoco Midtown and The M. As a result, the submarket saw a significant drop in vacancy rates from 10.6% in Q2 2023 to 7.9% in Q3 2023, the lowest since Q4 2019’s 7.3%. Improving return-to-office trends, coupled with the availability of space, could have spurred more retailers to take up space in the downtown core locations.

• CBRE Research believes that rents have continued to recover alongside tourism recovery and the increase in office crowds in Q3 2023. Anecdotally, CBRE Research notes that demand was primarily driven by F&B operators and services such as Cedric Grolet, Luckin Coffee and Clinique La Prairie. Several pop-up stores also took up space in the quarter, including TAG Heuer Motorsports Experience which was centred around the F1 race.

Residential

Overall private housing prices rose marginally in Q3 2023, reversing the decline in Q2 2023. The increase was led by upgraders in the OCR and RCR non-landed segments, partially offset by declines in landed properties and CCR non-landed segments. Developer sales volume had fallen by about 8.5% on a q-o-q basis and by about 11% on a y-o-y basis in Q3 2023. We believe prices will continue to stabilise over the next few quarters on softer economic conditions, elevated mortgage rates and recent cooling measures.

Private home prices rose marginally by 0.8% q-o-q in Q3 2023, higher than the flash estimate of 0.5% announced on 2 Oct, and reversing the 0.2% q-o-q decline in Q2 2023. With this, private home prices have risen 3.9% in the first nine months of 2023, and up 28.9% since bottoming in Q1 2020.

Price momentum picked up in the city fringe and suburban market segments, but overall home price growth was offset by a moderate decline in the CCR and a relatively steep correction in landed property prices. Prices of landed properties saw a steep correction of 3.6%, after 8 straight quarters of increase, the largest quarterly decline since Q2 2009 when prices fell 4.7% q-o-q.

Prices of non-landed properties increased 2.1% q-o-q, mainly driven by properties OCR and RCR. OCR prices rose 5.5% q-o-q, accelerating from the 1.2% in Q2 2023. RCR prices rose 2.1% q-o-q, reversing the 2.5% decline in Q2.

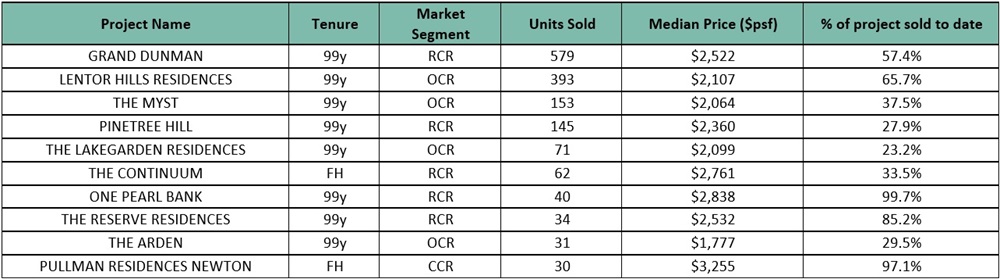

• New launches in OCR included Lentor Hills Residences, The Lakegarden Residences, The Myst, The Arden and The Altura EC. Response has also been mixed, with the EC outperforming private ones.

• Take-up rates are generally lower than last year’s, as buyer fatigue and resistance to high price points set in.

• The CCR saw a price decline of 2.7% q-o-q, as developers continued to dangle discounts to clear unsold inventory especially for those that near the ABSD timeline. Sentiment remained tentative after the 60% foreigners’ ABSD measure in April 2023. We note that CCR projects under construction such as The Atelier and The Avenir sold their last unit respectively in August and are now fully sold.

Source: URA, CBRE Research

*Sales status based on caveats from Realis as of 27 Oct 2023.

• New home sales slowed q-o-q despite a larger number of new projects and more units launched. 1,946 new private homes (excluding ECs) were sold in Q3 2023, 8.5% lower than the 2,127 units moved in Q2 2023. This could be attributed to weaker economic conditions and an indication of increased buyer selectiveness amid the myriad of available new launch options. Pent-up demand has also been mostly absorbed and genuine buyers are now spoilt for choice. In addition, prices have already moved up significantly and investors could feel that there is limited room for upside. Some of the projects which are targeted at investors or typically have a higher proportion of foreigner buyers will continue to face some resistance given the recent cooling measures doubling foreigners’ ABSD to 60% as well as a further increase in ABSD rate for investors. These investors will reassess their options and take a longer time to shop around.

• Stable activity was observed in the resale market. 2,900 resale units were transacted in Q3 2023, down marginally by 2.6% from Q2 2023’s 2,976 units. Resale transactions made up 55.8% of total transactions in Q3 2023, a relatively equal proportion to 55.2% in Q2 2023.

• Unsold inventory of uncompleted private residential units (excluding ECs) declined in Q3 2023 to 16,747 units from 17,484 units in Q2 2023. Including completed units, unsold inventory has likewise fallen 4.3% from 17,924 units in Q2 2023 to 17,161 units in Q3 2023.

o While unsold inventory is still significantly lower than the last peak of 37,799 units recorded in Q1 2019, the Government has ramped up GLS confirmed list supply under the H2 2023 GLS Program further to bring 2023’s full year supply to 9,250 units, the highest in a decade. Supply is now more in line with the 10-year average developer sales (2013 – 2022) of 9,706 units. Upcoming tenders of GLS sites would continue to see interest as developers have largely shifted their focus to acquiring development land via the GLS Programme over collective sales given the greater certainty of deal completion and pricing discretion. They are however likely to remain highly cautious and selective until there is more clarity on an economic recovery and interest rate stabilisation.

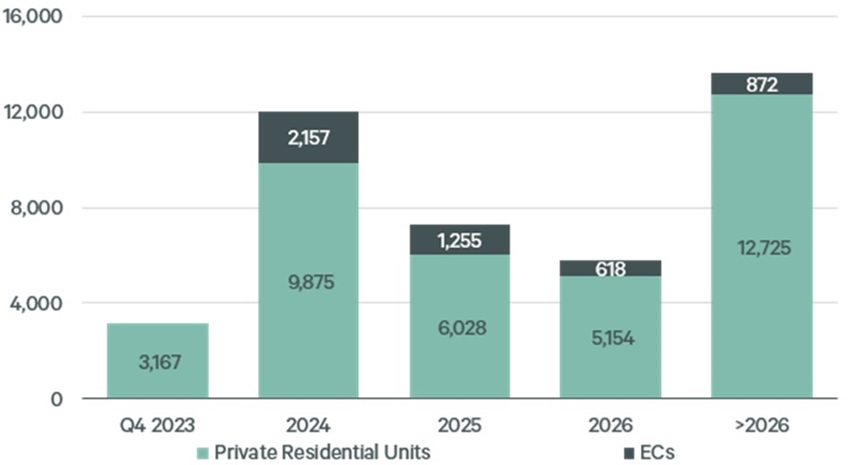

• 15,883 private homes (excluding ECs) have been completed in the first nine months of 2023. With 3,167 units due to complete in Q4, 2023 will see a total completion of 19,050 units, the largest number of completions since 20,648 units in 2017.

• With completions continuing to outstrip demand, vacancy rates rose significantly to 8.4% in Q3 2023 from 6.3% in Q2 2023, matching levels last seen in 2017. Rents are anticipated to ease further moving forward alongside abundant new supply in the coming quarters. Expatriate demand could moderate as companies restructure and cut back on hiring amid challenging economic conditions.

*For private residential units and ECs with planning approvals

Outlook

• Year-to-September new developer sales currently stand at 5,329 units, a 16.9% y-o-y fall from 6,409 units sold over the corresponding period in 2022. Souring macro backdrop, elevated interest rate hikes and cooling measures have resulted in increased buyer selectiveness and slower demand through 2023.

• Looking ahead, major launches that could be coming in Q4 2023 are concentrated in the OCR, with projects such as Lentoria (265 units), J’den (368 units), Hillock Green (474 units), Hillhaven (341 units) and Sora at Yuan Chin Road (440 units). The RCR could also see some launches – The Hill@one north (142 units) and Sky Botania (172 units) and the CCR could see the launch of Newport Residences (246 units). Amid weaker sentiment, still-high interest rates and the upcoming December holiday season, developers might choose to push launches into 2024 when interest rates stabilise and sentiment improves. As such, developer sales are expected to remain subdued in Q4 2023. Overall, CBRE Research expects 6,500 – 7,000 new private homes to be sold in 2023, potentially below the 7,099 units in 2022, which was already a 14-year low since 2008’s 4,264 units.

• In the rental market, overall private residential rents have risen 11.1% in the year-to-September 2023 so far and are up 58.5% since bottoming in Q3 2020. Moving forward, the 3,167 private residential units (excl. ECs) expected to be completed in Q4 2023 and 9,875 units in 2024 would inject a significant amount of stock into the market and alleviate the tight supply situation. In addition, we note expatriate demand has slowed with the economic slowdown and temporarily-displaced owners move into their newly completed homes as the backlog clears. Thus, we expect rents to start easing over the next few quarters.

• However, rents are unlikely to fall back to pre-2022 levels, due to increased property taxes, higher prices (requiring higher returns), higher mortgage payments from higher interest rates, and higher rental demand from the newly imposed 15-month wait-out period for downgraders (buying resale HDB) under Sep 2022’s round of cooling measures. CBRE Research expects islandwide private property rents to record a full year increase of 5%.

• Correspondingly, CBRE Research believes home prices which have risen 3.9% cumulatively have peaked and are likely to be muted in Q4 2023. Barring widespread retrenchments and a sustained recession, a significant price correction is not expected given low unsold inventory and generally healthy household balance sheets. As such, CBRE Research maintains its full year 2023 forecast for private home price growth of 3%, slower than the 8.6% seen in 2022 due mainly to a weaker economic outlook -- MTI forecasts 0.5 – 1.5% GDP growth for 2023, vs 3.6% for 2022.

Click here for more details on the URA press release.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.