Singapore

CBRE Commentary on URA Q4 2023 and FY 2023 Statistics

January 26, 2024

Associated Contact

Head of Marketing & Communications, Singapore

Office

• The office market surpassed expectations due to limited supply, increasing back-to-office rates, and gradual decline of shadow space. The URA office rental index (Central Region) inched up by 0.3% q-o-q in Q4 2023, following the increase of 4.9% q-o-q registered in the previous quarter. For the full year, office rents increased by 13.1% y-o-y, a faster increase from the 11.7% in 2022.

• This increase was primarily evident in the rentals of Category 1 office buildings (a proxy for prime CBD). Median rental (by contract date) in Category 1 office space increased by 2.7% q-o-q in Q4 2023, a reversal from a temporary decline of 2.3% in the previous quarter. CBRE Research explains that availability of space remains extremely tight due to limited supply. With the delayed completion of IOI Central Boulevard Towers from Q4 2023 to Q1 2024 and the resilient leasing demand observed across the year, vacancy rates for Category 1 buildings dropped to 7.5% in Q4 2023 from the high of 12.4% in Q3 2021. This was also the lowest vacancy since Q1 2020.

Table 1: Median rentals based on contract date

| Category 11 | Category 22 | |||||

|---|---|---|---|---|---|---|

| Rents ($psf/mth) | Q-o-q | Vacancy | Rents ($psf/mth) | Q-o-q | Vacancy | |

| Q4 2022 | $10.75 | 0.8% | 9.5% | $5.70 | 2.3% | 12.1% |

| Q1 2023 | $10.77 | 0.2% | 10.9% | $5.80 | 1.8% | 11.4% |

| Q2 2023 | $11.49 | 6.7% | 9.2% | $6.19 | 6.7% | 11.5% |

| Q3 2023 | $11.22 | -2.3% | 8.0% | $5.91 | -4.5% | 10.9% |

| Q4 2023 | $11.52 | 2.7% | 7.5% | $6.04 | 2.2% | 11.0% |

2 Refers to the remaining office space in Singapore which are not included in “Category 1”

Source: URA

• CBRE Research observed that some occupiers were renewing existing leases at higher reversionary rents rather than relocate, given high capex and interest rates. Selected premium office space with quality specs in the Core CBD were also highly contested among competing tenants, leading to rental escalation. Meanwhile, shadow spaces in prime areas like Marina Bay and Raffles Place attracted occupiers seeking high-quality, fitted office spaces. Some shadow spaces were also taken off the market as tech occupiers decided to retain their office premises. Thus, towards the end of 2023, CBRE observed shadow space declining from the peak of 0.7 million sq. ft. in Q1 2023 to 0.17 million sq. ft. by Q4 2023.

• According to URA data, despite the lack of supply, the market still experienced positive net absorption of 0.10 mil sq. ft., following the +0.25 mil sq. ft. in Q3 2023. This led islandwide vacancies to inch down from 10.0% in Q3 2023 to 9.9% in Q4 2023. CBRE Research observed that office demand remained resilient and was seen from sectors including private wealth asset management firms, legal sector, flexible workspace operators and government agencies.

Outlook

• According to CBRE Research’s data, Core CBD (Grade A) rents grew by 1.7% y-o-y, moderating from the 8.3% rental growth in 2022. Moving forward, the market may face a slower first half with an above historical average completion pipeline in 2024 and potential secondary spaces, which could lend to a temporary increase in the availability of spaces.

• That said, sentiment could pick up in H2 2024 as interest rates and inflationary pressures ease. As the economy picks up, companies could regain confidence to increase budgets and embark on relocations, expansionary or workplace strategies. With flight-to-quality and flight-to-green trends to continue, CBRE Research expects Core CBD (Grade A) rents to grow at a moderate pace of 2% - 3% in 2024.

Retail

• Retail indicators such as the retail sales index started to flatten out y-o-y in Q4 2023. Retail sales could have been affected by the higher number of outbound residents, and the erosion of consumers’ purchasing power as a result of ongoing inflation. Therefore, URA’s Q4 2023 data showed that rents of retail space in the Central Region fell marginally by 0.1% q-o-q, reversing the increase of 0.5% q-o-q the previous quarter. Rents for full year 2023 increased slightly by 0.4% y-o-y, marking the first year that rents have risen since the pandemic. CBRE Research observes that the retail market continues to be two-tiered, with strong leasing demand for prime spaces in Q4 2023 supporting islandwide prime rents. Prime rents increased by 1.2% q-o-q, extending the rise of 1.4% q-o-q the previous quarter and bringing full year growth to 4.2% y-o-y.

• Rate hikes and the weak global macroeconomic backdrop have resulted in softer investor sentiments in H1 2023, with prices of retail assets in the Central Region falling slightly by between end-2022 to June 2023. However, investor sentiment started to improve in H2 2023 alongside a firm tourism recovery, resulting in a full year price increase of 1.2% y-o-y, compared to an overall decline of 7.8% y-o-y in 2022.

• Buoyed by the year-end festive season, Q4 2023 saw a plethora of retail expansions and new market entrants. According to URA data, the islandwide private retail market experienced positive net absorption of 69,000 sq. m. (about 743,000 sq. ft.), in line with strong leasing demand seen in Q4 in previous years. As a result, islandwide private retail vacancy rates fell from 8.0% in Q3 2023 to 6.7% in Q4 2023, the lowest vacancy rate since Q4 2014’s 6.5%.

• All submarkets saw positive net absorption in Q4 2023, with the fringe and Orchard areas outperforming the rest of the submarkets. The fringe area saw positive net absorption of 26,000 sq. m. (about 280,000 sq. ft.), leading to a fall in vacancy rates from 8.2% in the previous quarter to 6.7% in Q4 2023, a record low for the past decade. This was likely due to the completion of One Holland Village, a pet-friendly mall which is part of a mixed-use development. Almost half of the tenants are F&B operators, while 14% offer services such as health, beauty and wellness.

• The Orchard submarket also saw strong positive net absorption of 19,000 sq. m. (about 205,000 sq. ft.), bringing vacancy rates down from 11.8% in Q3 2023 to 8.7% in Q4 2023. The increase in tourist arrivals could have spurred retailers to take up space in the submarket, especially overseas retailers who are looking to showcase their brands to an international audience. Notably, United Colors of Benetton re-entered Singapore after exiting in 2015, while L’Artisan Parfumeur and Press Butter Sand set up physical stores in Takashimaya Shopping Centre in the quarter.

• CBRE Research believes that rents have continued to recover alongside tourism recovery and the year-end festive season in Q4 2023. Anecdotally, CBRE Research notes that demand was primarily driven by F&B operators and fashion brands such as Ju Xing Home, Fore Coffee, Tim Hortons, Marimekko and Cloud9 Studio. Pop-up stores continued to proliferate in the quarter, including Dyson Holiday Beauty Lab and Nintendo pop-up.

Outlook

• Retailers are cautiously optimistic about tourism recovery and consumer spending as labour market conditions remain resilient. However, In the near term, retailers may continue to face challenges such as manpower shortage, competition from e-commerce and higher operating costs. Nonetheless, tourism arrivals will be boosted by the strong pipeline of MICE events and sell-out concerts, which should support demand for prime retail spaces. Coupled with below-historical-average new retail supply in the next few years, CBRE Research expects overall retail rents to maintain its growth trajectory in 2024.

Residential

Rentals of private residential properties fell for the first time in three years in Q4 2023, breaking a streak of 12 consecutive quarterly increases and ending the 58.5% run-up since Q2 2020. With this, rents rose 8.7% in 2023, a significant moderation from 29.7% growth in 2022 on the back of abundant completions in 2023. Rents are on average up 55.1% above last pandemic-low in Q3 2020.

Private housing prices continued to rise in Q4 2023, capping the year with a 6.8% full year increase, albeit slowing slightly from the 8.6% increase in 2022. This means private home prices have grown for 7 straight years, after bottoming in mid-2017. 2023’s increase was led by suburban non-landed market which rose 13.7% y-o-y, while the prime and city fringe markets grew by a much more sustainable pace of 1.9% and 3.1% respectively.

Overall prices have run up 32.5% since the onset of COVID-19, mainly driven by locals’ pent-up demand and the slower supply over 2020-2022. There have been indications of an increasing resistance to high price points in 2023 amid higher interest rates and the punitive 60% ABSD for foreigners (since late April), with sale transaction volume falling by about 44% on a q-o-q basis in Q4 2023 and by 9.6% on a y-o-y basis for the whole of 2023. Full year 2023 developer sales came in at 6,421 units, a 15-year low. We expect developer sales could remain soft in H1 2024, before normalising to a full year take-up of 7,000 – 8,000 units.

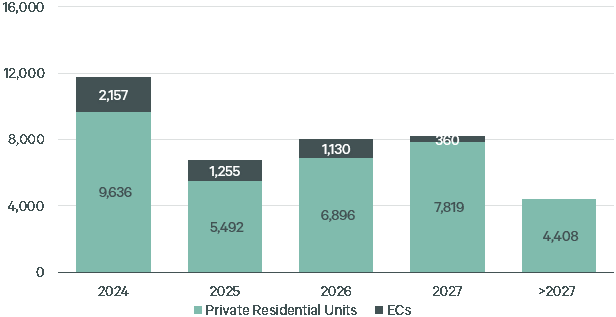

We expect a soft landing for the residential market as the price and rental growth should moderate in 2024 but not crash. Prices are unlikely to correct significantly due to resilient household balance sheets and low unsold inventory, while rents could soften in the H1 2024 as the market digests the peak completions in 2023 of close to 20,000 private homes which will taper off significantly to less than 10,000 units and 6,000 units in 2024 and 2025 respectively.

Private home prices rose moderately by 2.8% q-o-q in Q4 2023, accelerating from the 0.8% q-o-q increase in Q3 2023. With this, private home prices for 2023 as a whole rose 6.8%, slowing down from the 8.6% in 2022, and are up 32.5% since the onset of COVID-19.

o In Q4 2023, Prices of landed properties rebounded strongly by 4.6% q-o-q after a 3.6% decline in Q3 2023 while prices in the non-landed segment grew 2.3% q-o-q, at a similar pace to the last quarter. The increase in prices of non-landed properties was driven by properties in the Outside of Central Region (OCR) and CCR where prices rose by 4.5% q-o-q and 3.9% q-o-q respectively in Q4 2023, supported by benchmark prices set at new launches. Overall growth in non-landed properties, however, was weighed down by a 0.8% q-o-q decline in RCR prices.

o During the quarter, the launch of J’den in the OCR and the private launch of Watten House in the CCR saw warm responses and set new benchmark prices in their respective areas, supporting price growth in their segments.

o The decline in the RCR price index could be attributed to existing projects such as Liv @ MB, Myra and One Pearl Bank clearing their last few units at discounts. The mentioned three projects sold their last few units in Q4 2023 and are now fully sold.

o Prices of non-landed properties increased by 6.6% in 2023, moderating from the 8.1% increase in 2022. Prices of non-landed properties in the CCR and RCR increased by 1.9% and 3.1% respectively in 2023, moderating from their respective increases of 4.8% and 9.7% in 2022 while OCR prices saw stronger price growth of 13.7% in 2023 compared to 9.3% in 2022.

| Project name | Tenure | Market segment | Units sold | Median price ($psf) | % of project sold to date* |

|---|---|---|---|---|---|

| THE RESERVE RESIDENCES | 99y | RCR | 663 | $2,473 | 90.6% |

| J'DEN | 99y | OCR | 326 | $2,478 | 88.6% |

| BLOSSOMS BY THE PARK | 99y | RCR | 227 | $2,441 | 82.5% |

| LENTOR HILLS RESIDENCES | 99y | OCR | 438 | $2,105 | 73.2% |

| SCENECA RESIDENCE | 99y | OCR | 175 | $2,086 | 65.3% |

| GRAND DUNMAN | 99y | RCR | 616 | $2,523 | 61.1% |

| TEMBUSU GRAND | 99y | RCR | 377 | $2,461 | 59.1% |

| THE BOTANY AT DAIRY FARM | 99y | OCR | 227 | $2,065 | 58.8% |

| THE MYST | 99y | OCR | 182 | $2,075 | 44.6% |

| THE CONTINUUM | FH | RCR | 304 | $2,733 | 37.3% |

*Sales status based on caveats from Realis as of 26 Jan 2024.

• New home sales slowed in Q4 2023 amid a limited number of new launches and the December holiday lull. The quarter saw three new launches and 1,060 newly launched units, less than half of the 2,805 units launched in Q3 2023. Correspondingly, 1,092 new private homes (excluding ECs) were sold in Q4 2023, 43.9% lower than the 1,946 units moved in Q3 2023. This could be attributed to weaker economic conditions, buyer fatigue and increasing resistance to high price points. Foreigner buying remains subdued since the doubling of ABSD to 60% in Apr 2023.

• In contrast, stable activity was observed in the resale market. 2,831 resale units were transacted in Q4 2023, down marginally by 2.4% from Q3 2023’s 2,900 units. Resale transactions made up 65.3% of total transactions in Q4 2023, a higher proportion than 55.8% in Q3 2023 on lower new sales. 11,329 resale homes were sold in 2023, a 19.2% fall from 14,026 units in 2022.

• Unsold inventory of uncompleted private residential units (excluding ECs) rose in Q4 2023 to 16,929 units from 16,747 units in Q3 2023. Including completed units, unsold inventory likewise increased 0.6% from 17,161 units in Q3 2023 to 17,262 units in Q4 2023.

• Rentals of private residential properties fell for the first time in three years in Q4 2023, breaking a streak of 12 consecutive quarterly increases and ending the 58.5% run-up since Q2 2020. Based on the URA Rental Index for all private residential properties, rents declined 2.1% q-o-q in Q4 2023, a reversal from the 0.8% rise in Q3 2023. With this, rents rose 8.7% in 2023, a significant moderation from 29.7% growth in 2022 on the back of abundant completions in 2023.

Source: URA, CBRE Research

*For private residential units and ECs with planning approvals

Outlook

• 6,421 new homes were sold in 2023, 10.2% lower than the 7,099 units recorded in 2022 and a 15-year low since 2008’s 4,264 units. Overall sell-through rate in 2023 was lower than 2022, largely due to weaker economic conditions, increased buyer selectiveness amid a myriad of new launch options and increasing resistance to high price points. In addition, prices have already moved up significantly and investors could feel that there is limited room for upside.

• Looking ahead, CBRE Research is cautiously optimistic on the private residential market in 2024. The current tentative buying sentiment is expected to stretch into H1 2024 amid still-high interest rates and uncertain economic conditions but sentiment could improve in H2 2024 if interest rates ease and the economy recovers. Overall, CBRE Research expects 7,000 – 8,000 new private homes to be sold in 2023, an improvement from the 6,421 units in 2023 but still below the 5-year average new developer sales across 2019 – 2023 of 9,288 units.

• In the rental market, overall private residential rents rose 8.7% in 2023. Moving forward, the 9,636 private residential units (excl. ECs) (Chart 1) expected to be completed in 2024 would inject a healthy amount of stock into the market and continue to exert downward pressure on rents. In addition, expatriate demand has slowed from a pullback in hiring activity as companies restructure amid weaker economic conditions and temporarily-displaced owners move into their newly completed homes. As such, we expect rents to continue easing over the next few quarters. However, rents are unlikely to fall back to pre-2022 levels, due to increased property taxes, higher prices (requiring higher returns), higher mortgage payments from higher interest rates, and higher rental demand from the newly imposed 15-month wait-out period for downgraders (buying resale HDB) under Sep 2022’s round of cooling measures. CBRE Researches forecasts islandwide rents to rise 1 – 3% in 2024, slowing from the 8.7% increase in 2023. Barring a significant pullback in demand, a correction is not expected due to the elevated inflationary environment which should support asking rents.

• Home prices which rose 6.8% in 2023, moderating from 8.6% in 2022 are expected to see momentum ease further in 2024. CBRE Research forecasts that private residential prices could grow 3 – 4% in 2024. A significant decline is not expected given still-low unemployment rate, resilient household balance sheets, and low unsold inventory.

Read the URA press release here .

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.