Singapore

Commentary on Monthly New Home Sales for February 2026

March 16, 2026

Associated Contact

Head of Marketing & Communications, Singapore

In the absence of new launches amid the Chinese New Year lull, developer sales slowed in February. 246 new private homes were sold, down 47.2% m-o-m from 466 units in Jan 2026 and 84.6% y-o-y from the 1,597 units moved in Feb 2025.

This brings the first two months of the year’s new home sales to 712 units, down 73.4% compared to the same period last year which had been bolstered by robust takeup of The Orie, Parktown Residence, and Elta. Homebuying sentiment and appetite is by no means weaker as the attractive launch line-up starting from March should see sales pick up strongly hereon.

Top 10 Selling Projects in February 2026 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

NEWPORT RESIDENCES |

ANSON ROAD |

999 yrs |

CCR |

32 |

$3,059 |

66.3% |

|

PINETREE HILL |

PINE GROVE |

99 yrs |

RCR |

19 |

$2,576 |

97.7% |

|

CHUAN PARK |

LORONG CHUAN |

99 yrs |

OCR |

14 |

$2,674 |

91.4% |

|

ONE MARINA GARDENS |

MARINA GARDENS LANE |

99 yrs |

RCR |

13 |

$2,989 |

62.2% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

Freehold |

RCR |

12 |

$2,915 |

85.4% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

12 |

$2,550 |

75.1% |

|

NARRA RESIDENCES |

DAIRY FARM WALK |

99 yrs |

OCR |

12 |

$2,146 |

23.9% |

|

THE LAKEGARDEN RESIDENCES |

YUAN CHING ROAD |

99 yrs |

OCR |

10 |

$2,321 |

94.1% |

|

ELTA |

CLEMENTI AVENUE 1 |

99 yrs |

OCR |

10 |

$2,669 |

74.5% |

|

OTTO PLACE (EC) |

PLANTATION CLOSE |

99 yrs |

OCR |

10 |

$1,760 |

98.5% |

There were no new launches in Feb 2026 amid the Chinese New Year lull. As such, all top performing projects were existing launches, including 1 EC project.

The top performing launch was 999-year CBD project Newport Residences (246 units) which moved over 50% sold during its launch in January, due to its attractive pricing for a near-freehold project in the CCR. The project sold 32 more units in February at a median price of $3,059 psf.

The second top performer was city-fringe launch Pinetree Hill (520 units) which was launched in Jul 2023. The project moved another 19 units in Feb 2026 at a median price of $2,576 psf and is now 98% sold. This was followed by suburban project Chuan Park (916 units). Launched in Nov 2024, 14 more units changed hands at a median price of $2,674 psf in Feb 2026.

By market segment, Feb 2026’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR). 103 units or 42% of total February sales were recorded, compared to 121 units (26%) in Jan 2026.

- The Outside Central Region (OCR) moved 80 units or 33% of total February sales after 183 units (39%) in Jan 2026.

- The Core Central Region (CCR) moved 63 units (26% of total February sales), down from 162 units (35%) in January which saw the launch of Newport Residences.

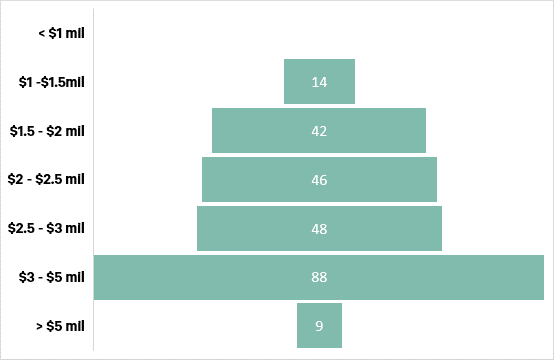

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 16 Mar 2026.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) at 36% was actually in the S$3.00 – 5.00 mil range from larger units sold at existing launches Chuan Park, The Continuum, and Pinetree Hill. The $2.50 – 3.00 mil range was second at 19%.

Outlook and Forecasts

February’s sales take the tally of new homes sold in 2M2026 to 712 units. Looking ahead, sales momentum is set to pick up in March alongside high-profile launches such as River Modern (455 units) in the River Valley district. It was reported that the project saw robust take-up, moving 410 units or 90% of its total 455 units at an average price of $3,266 psf over its launch weekend on 7-8 March.

At Tampines in the OCR, residential-commercial project Pinery Residences (588 units) at Tampines Street 94 and nearby Rivelle Tampines EC (572 units) have started previews, with prices starting from around $2,400 psf and around $1,800 psf respectively. Despite the benchmark pricings, they could still see good demand from upgraders and first timers when they open for booking on 28 and 21 March respectively.

Homebuying sentiment and appetite has been healthy on the back of fast-declining interest rates and steady household income growth. However, volatility arising from a protracted US–Iran conflict is likely to increase caution among homebuyers, who may become more discerning in their purchase decisions. Competitive and realistic developer pricing will be critical.

CBRE Research projects that 7,500 – 8,500 new homes will be sold in 2026, coming off a strong pent-up demand and the 10,815 units in 2025, and slightly below the 5-year average (2021 – 2025) of 8,766 units.

Correspondingly, private home prices, which increased 3.3% in 2025, are likely to grow at a stable pace in 2026. CBRE Research forecasts a price growth of 2 – 4%.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.