Singapore

Commentary on Monthly New Home Sales for June 2026

July 15, 2026

Associated Contact

Head of Marketing & Communications, Singapore

In the absence of new launches amid the school holidays lull, June’s developer sales slowed to the lowest monthly level in over two years. 156 new private homes were sold, down 65.1% m-o-m from 447 units in May 2026, and down 42.6% y-o-y from 272 units in June 2026. This is also the lowest monthly sales since 153 units were sold in February 2024.

June sales take the tally of new sales in H1 2026 to 4,164 units, 9.2% below the 4,587 units recorded in H1 2025. New sales momentum is, however, expected to pick up in the months ahead as some attractive launches test the market. Homebuying appetite appears to stay resilient despite heightened volatility and economic uncertainty from the ongoing Middle East conflict amid low mortgage rates.

Top 10 Best-selling Projects in Jun 2026 (including ECs and landed)

|

Project Name |

Street Name |

Tenure |

Locality |

Units Sold in the Month |

Median Price ($psf) in the Month |

% of project sold to date |

|

COASTAL CABANA (EC) |

JALAN LOYANG BESAR |

99 yrs |

OCR |

21 |

$1,836 |

82.5% |

|

HUDSON PLACE RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

12 |

$2,577 |

67.6% |

|

THE CONTINUUM |

THIAM SIEW AVENUE |

Freehold |

RCR |

11 |

$2,789 |

95.7% |

|

UNION SQUARE RESIDENCES |

HAVELOCK ROAD |

99yrs |

RCR |

11 |

$2,762 |

48.6% |

|

CHUAN PARK |

LORONG CHUAN |

99 yrs |

OCR |

11 |

$2,631 |

96.4% |

|

TERRA HILL |

YEW SIANG ROAD |

99 yrs |

RCR |

9 |

$2,654 |

75.6% |

|

ELTA |

CLEMENTI AVENUE 1 |

99 yrs |

OCR |

6 |

$2,825 |

82.2% |

|

BLOOMSBURY RESIDENCES |

MEDIA CIRCLE |

99 yrs |

RCR |

6 |

$2,551 |

86.9% |

|

THE SEN |

JALAN JURONG KECHIL |

99 yrs |

RCR |

6 |

$2,341 |

38.3% |

|

NARRA RESIDENCES |

DAIRY FARM WALK |

99 yrs |

OCR |

6 |

$2,219 |

34.3% |

|

RIVELLE TAMPINES (EC) |

TAMPINES STREET 95 |

99 yrs |

OCR |

6 |

$1,947 |

97.9% |

In June, as there were no new launches in June, the top 10 best-selling projects in the month were all existing launches from the RCR and OCR, including 2 EC developments.

EC project, Coastal Cabana (748 units) at Jalan Loyang Besar, which launched in January 2026 was the best-selling project, moving another 21 units at a median price of $1,836 psf. This EC project, which was launched in January 2026, has seen renewed interest after major EC policy changes were to take effect on new EC sites sold after 8 May 2026. Key changes include doubling the Minimum Occupation Period (MOP) to 10 years, removing the Deferred Payment Scheme (DPS), and raising the first-timer quota to 90%.

The second-best performer in June was RCR project Hudson Place Residences (327 total units) which moved 209 units at a median price of $2,465 psf last month after its mid-May launch. 12 more units were sold in June at a median price of $2,577 psf.

Tied in third place with 11 units transacted are RCR projects The Continuum (816 units), Union Square Residences (366 units) and OCR launch Chuan Park (916 units) which saw units trade at median prices of $2,789 psf, $2,762 psf and $2,631 psf respectively.

By market segment, June 2026’s developer sales (excluding ECs) were led by the Rest of Central Region (RCR), accounting for 84 units or 54% of total June sales, compared to 334 units (75%) in May 2026.

- The Outside Central Region (OCR) moved 57 units or 37% of total June sales after 91 units (20%) in May 2026.

- The Core Central Region (CCR) moved 15 units (10% of total June sales), down from 22 units (5%) in May.

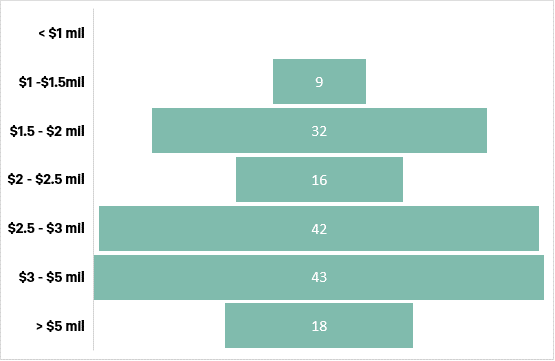

New Home Sales (excl. ECs) by quantum

Source: CBRE Research, URA

*Based on Realis new sales (excl. EC) caveats extracted on 15 July 2026.

Based on quantum size, the largest proportion of new private homes sold (excl. ECs) at 27% was in the S$3.00 – 5.00 mil range as buyers scooped up larger 3 and 4-bedders from existing projects such as The Continuum and Chuan Park.

The $2.50 – 3.00 mil range was second at 26%, followed by the $1.50 – 2.00 mil bracket at 20%.

Outlook and forecasts

Homebuying appetite has remained resilient in the year so far despite heightened volatility and economic uncertainty from the ongoing Middle East conflict, which has re-escalated after the peace deal between the US and Iran fell through.

Looking ahead, sales momentum is expected to gain steam in July following the lull in June alongside announced high-profile launches such as suburban project Lentor Gardens Residences (499 units), the seventh project in the popular Lentor estate, and CCR project Dunearn House (380 units), the maiden launch in the Bukit Timah Turf City rejuvenation.

Based on Q2 2026 GDP advance estimates, the quarter recorded 5.7% y-o-y GDP growth, easing from the restated 6.3% y-o-y in Q1 2026, but nonetheless still very robust for a mature economy. Barring major economic shocks, CBRE Research projects that 7,500 – 8,500 new homes will be sold in 2026 given a decent pipeline of attractive new launches, healthy household balance sheets, low unemployment rate, and low mortgage rates. This represents a moderation after above-trend sales of 10,815 units in 2025, and is slightly below the 5-year average (2021 – 2025) of 8,766 units.

Private home prices have risen 1.4% in H1 2026, based on Q2 2026’s flash estimate, and could grow at a similar pace in H2 2026. We maintain our private home prices to grow 2 – 4% in 2026 for now, relatively in line with MTI’s most recent 2026 GDP growth forecast of 2 – 4%, which is a moderation from the 5% GDP growth for 2025.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.