Singapore

Commentary on the GLS 1H 2026 – Sustained high housing supply, JLD, new Bayshore commercial-residential site

December 2, 2025

Associated Contact

Head of Marketing & Communications, Singapore

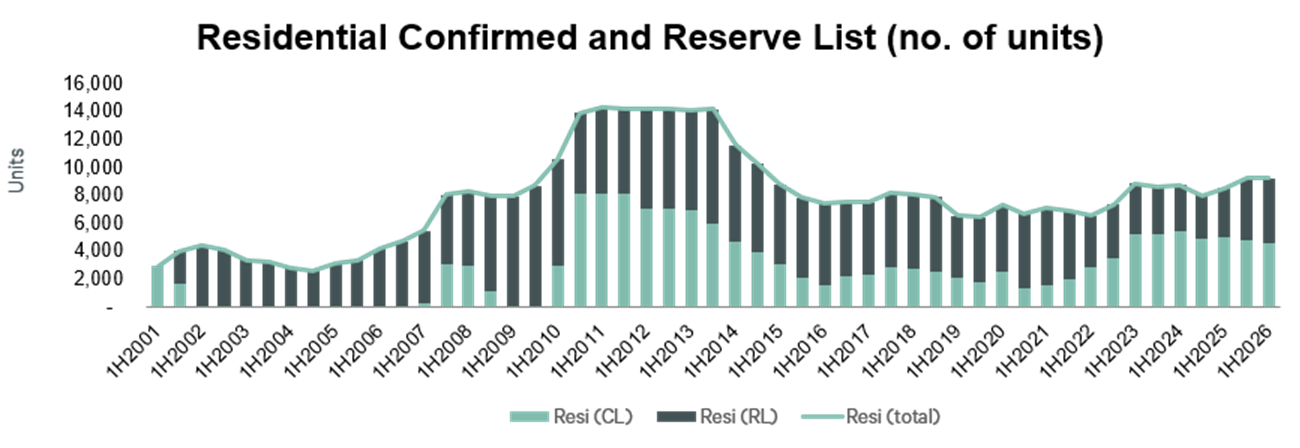

Sustained high housing supply

The 1H 2026 Government Land Sale (GLS) program saw the government maintain the overall residential supply at around 9,200 units, similar to 2H 2025 GLS. The supply consists of a good spread of sites across various geographical locations, supporting the development of both conventional private residential units and long-stay Serviced Apartments, to cater to both owner-occupation and rental housing demand.3,940 private housing units across 6 private residential and 1 commercial-residential site, and 635 Executive Condominium (EC) units across 2 EC projects, will be launched via the Confirmed List in 1H2026. An additional 4,610 units will be made available via the Reserve List. Included in the Reserve List are 1,200 residential units that could be developed in the Town Hall Link (JLD carve-out) white site (up from 600 units from JLD in 2H 2025 GLS). The hotel site at Telok Ayer brought over from 2H25’s Reserve List has a reduced SA2 requirement of 135 units from 200 units, while the Cross Street site and Media Circle sites maintained the quota of 315 and 520 SA2 units respectively. This brings to a total of 970 SA2 units that could be built, all via the Reserve List, and could be triggered if there is demand.

Excluding 635 EC units, 1H 2026 GLS Confirmed List of 3,940 private homes are higher than the 3,735 private homes in 2H 2025 Confirmed List, implying approximately 8,000 units on an annualised basis, which is higher than 2024’s 6,469 developer sales (excluding ECs), but lower with the 2014-2023 10-year average developer sales of 8,853 units. This should provide ample future land banking opportunities for developers, who can also trigger the Reserve List sites should they deem there is more demand.

Source: CBRE Research, MND. Resi: Residential. CL: Confirmed List. RL: Reserve List.

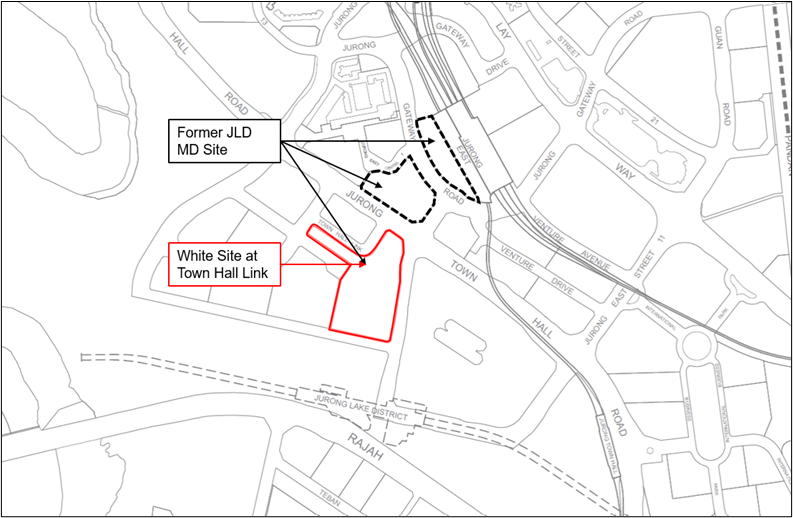

Carve-out of JLD white site

The former JLD master developer white site has been carved out into the Town Hall Link site, half the original size – with a total potential yield of 186,000 sqm, comprising a minimum of 40,000 sqm of office space, up to 1,200 private residential units and 44,000 sqm GFA of space for complementary uses (e.g. retail, hotel, community uses).Location Plan for the White Site at Town Hall Link

Source: MND

We believe this shows that the Government remains committed to developing JLD as the largest mixed-use business district outside the city centre and a model sustainable district that integrates business, residential and recreational spaces, despite 2024’s failed tender of the master developer site.

In 2024, after a concept-price tender process with only two bids from one bidder group received, the final offer price of $640 psf ppr from the consortium of five major developers (CapitaLand Development, City Developments Ltd, Frasers Property, Mitsubishi Estate and Mitsui Fudosan Asia) was deemed too low, and the tender was not awarded. The outcome reflected generally cautious market sentiment amid high financing costs and global economic uncertainties then. Developers were also concerned about the significant scale of the project, which entails multi-year development risks and substantial capital outlay. The winning party would additionally be responsible for district-wide infrastructure, including a district cooling system and pneumatic waste conveyancing—further increasing development costs.

We believe the carved-out smaller parcel should attract better interest. At roughly half the size of the previous Master Developer site, the reduced scale as well as a higher number of residential units that could be pre-sold, should ease upfront capital commitment and mitigate development risks. This signals greater flexibility and responsiveness to earlier market feedback gathered from extensive engagements of industry stakeholders. We understand the government will undertake some of the infrastructure requirements which should also provide some relief to the developer, though more details will be disclosed when the site is launched.

The recent sale of JEM’s office component to Keppel in August 2025 for $462 million underscores long-term confidence in the JLD location. It also shows that demand for suburban office assets persists, though valuation remains a critical factor. Future transport enhancements—including the Jurong Region Line (2028) and Cross-Island Line (2032)—will further enhance accessibility and improve the site’s appeal for both businesses and residents.

New Bayshore/ Bedok South commercial-residential site

We also note a large commercial-residential site at Bayshore Drive on top of the Bedok South MRT station under construction has been added to the GLS Confirmed List. With a total GFA of over 1.6 bn sq ft including 1,280 dwelling units and 22,500 sqm of commercial GFA, land cost will likely exceed $1 bn and this will be one of the largest mixed-use projects in the East Coast of Singapore. Key attractions could be the proximity to popular Temasek Primary School and MRT station, and some unblocked landed views. We expect developers to partner up to diversify risks and mitigate the large capital outlay.Which are the most attractive new sites on GLS 1H 2026?

The 1H2026 Confirmed List offers a good mix of attractive sites across all market segments, with more sites in the Newton, Bayshore and Greater Southern Waterfront precincts which have been earmarked for transformation.There are 9 residential sites on the Confirmed List, of which 7 are new, and 2 were carried over from 2H25’s Reserve List – Holland Plain and River Valley Green (Parcel C). Among the new sites, we find the most attractive sites to be Lorong Puntong, New Upper Changi Road and Peck Hay Road.

Most attractive sites:

1. Lorong Puntong (140 units)- Palatable size

- Walking distance from Bright Hill MRT

- Sin Ming estate bordering Bishan and Ang Mo Kio could see strong upgrader demand

- Located just opposite the popular Ai Tong School

- Last GLS plot in neighbourhood was awarded more than a decade ago on 13 Oct 2014

2. New Upper Changi Road (1,040 units)

- Walking distance from Bedok MRT, and host of amenities at Bedok Mall and Chai Chee Business Park

- Mature residential estate

- 4 years since the last new launch in the area, Sky Eden @ Bedok launched in Sep 2022. Likely to see strong upgrader demand from nearby Chai Chee and Bedok HDB estates or downgraders from nearby Opera Estate

3. Peck Hay Road (315 units)

- 2nd site, under the Draft Master Plan 2025 for the transformation of Newton area from its current business-oriented nature to a more balanced residential and lifestyle hub, with white sites or mixed-use developments planned around Newton MRT

- Bukit Timah Road site launched under the 2H2025 GLS programme had seen robust interest from developers in November.

- This Peck Hay Road site is further from Newton MRT compared to the Bukit Timah Road but still within walking distance

- Within 1km of SJIJ and ACS Junior

- Prime location 1 MRT stop away from the Orchard Road shopping belt

- Palatable size

Event and details

The Government has announced the GLS Programme for 1H2026. Comprising nine Confirmed List sites and 12 Reserve List sites, the Programme can yield 9,185 private residential units, 209,150 sqm gross floor area (GFA) of commercial space and 970 hotel rooms.

The Confirmed List, which comprises eight private residential sites and one Commercial & Residential site, can yield 4,575 private residential units (including 635 EC units) and 22,500 sqm GFA of commercial space.

The Reserve List includes six private residential sites, one commercial site, three White sites and two hotel sites, which can potentially yield an additional 4,610 private residential units, 186,650 sqm GFA of commercial space, and 970 hotel rooms.

The Government will continue to closely monitor economic and property market conditions, and adjust the GLS programme as necessary to meet Singapore’s housing, commercial and hospitality needs.

Read the MND press release here.

PROPOSED RESIDENTIAL, COMMERCIAL AND HOTEL SITES FOR 1H2026 GLS PROGRAMME

|

S/N |

Location |

Site Area (ha) |

Proposed GPR |

Estimated No. of Residential Units (1) |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (m2) |

Estimated Launch Date |

Sales Agent |

|

Confirmed List |

||||||||

|

Residential Sites |

||||||||

|

1 |

1.57 |

1.8 |

280 |

0 |

0 |

Feb-2026 |

URA |

|

|

2 |

1.15 |

3.5 |

470 |

0 |

0 |

Apr-2026 |

URA |

|

|

3 |

0.55 |

4.9 |

315 |

0 |

0 |

Apr-2026 |

URA |

|

|

4 |

2.54 |

1.4 |

415 |

0 |

0 |

May-2026 |

URA |

|

|

5 |

1.16 |

1.6 |

185 |

0 |

0 |

May-2026 |

HDB |

|

|

6 |

3.16 |

2.8 |

1,040 |

0 |

0 |

May-2026 |

URA |

|

|

7 |

0.43 |

2.8 |

140 |

0 |

0 |

Jun-2026 |

URA |

|

|

8 |

1.29 |

3.5 |

450 |

0 |

0 |

Jun-2026 |

HDB |

|

|

Commercial & Residential Sites |

||||||||

|

9 |

5.74 |

2.6 |

1,280 |

0 |

22,500 |

Mar-2026 |

URA |

|

|

|

Total (Confirmed List) |

4,575 |

0 |

22,500 |

|

|

||

|

S/N |

Location |

Site Area (ha) |

Proposed GPR |

Estimated No. of Residential Units (1) |

Estimated No. of Hotel Rooms |

Estimated Commercial Space (m2) |

Estimated Available Date (16) |

Sales Agent |

|

Reserve List |

||||||||

|

Residential Sites |

||||||||

|

1 |

0.60 |

5.6 |

390 |

0 |

150 |

Available |

URA |

|

|

2 |

0.57 |

4.2 |

520 |

0 |

400 |

Available |

URA |

|

|

3 |

1.00 |

4.3 |

500 |

0 |

400 |

Available |

URA |

|

|

4 |

0.23 |

6.3 |

315 |

0 |

500 |

Available |

URA |

|

|

5 |

0.66 |

2.8 |

200 |

0 |

750 |

Feb-2026 |

URA |

|

|

6 |

0.39 |

3.0 |

135 |

0 |

0 |

Jun-2026 |

URA |

|

|

Commercial Sites |

||||||||

|

7 |

1.00 |

1.4 |

0 |

0 |

13,350 |

Available |

URA |

|

|

White Sites |

||||||||

|

8 |

1.73 |

4.2 |

775 |

0 |

6,000 |

Available |

URA |

|

|

9 |

2.75 |

4.2 |

440 |

0 |

78,000 |

Available |

URA |

|

|

10 |

3.72 |

- |

1,200 |

0 |

84,000 |

Mar-2026 |

URA |

|

|

Hotel Sites |

||||||||

|

11 |

1.02 |

2.8 |

0 |

530 |

2,000 |

Available |

URA |

|

|

12 |

0.42 |

7.0 |

135 |

440 |

1,100 |

Dec-2025 |

URA |

|

|

|

Total (Reserve List) |

4,610 |

970 |

186,650 |

|

|

||

|

|

Total (Confirmed List and Reserve List) |

9,185 |

970 |

209,150 |

|

|

||

(1) The estimated number of dwelling units (DU) for Executive Condominium and private residential sites take into account the average unit sizes of recent comparable developments and prevailing Development Control guidelines.

(2) Site is imposed with DU cap of 282 residential units.

(3) New sites introduced in 1H2026.

(4) A mixed-use development with integrated bus interchange facilities (estimated 6,500 sqm GFA). Site is imposed with DU cap of 1,280 residential units and a retail cap of 22,500 sqm GFA.

(5) Site is imposed with a retail cap of 150 sqm GFA.

(6) Site is predominantly for long-stay Serviced Apartments use and imposed with a retail cap of 400 sqm GFA.

(7) Site is imposed with a retail cap of 400 sqm GFA.

(8) Site is predominantly for long-stay Serviced Apartments use and imposed with a minimum commercial quantum of 500 sqm GFA.

(9) Site is imposed with a minimum retail quantum of 750 sqm GFA and a minimum 500 sqm GFA for childcare centre.

(10) Site is imposed with a minimum office quantum of 8,400 sqm GFA and a minimum 650 sqm GFA for childcare centre.

(11) Site is imposed with a retail cap of 6,000 sqm GFA and a minimum 500 sqm GFA for childcare centre.

(12) Site is imposed with a retail cap of 33,000 sqm GFA and a minimum office quantum of 45,000 sqm GFA.

(13) Site is imposed with a minimum office quantum of 40,000 sqm GFA, a minimum 800 sqm GFA for childcare centre and a maximum residential quantum of 102,000 sqm GFA.

(14) Site is imposed with a retail cap of 2,000 sqm GFA.

(15) Site is imposed with a minimum long-stay Serviced Apartments quantum of 6,200 sqm GFA.

(16) Refers to estimated date the detailed conditions of sale will be available and applications can be submitted.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2024 revenue). The company has more than 140,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.